Valued at a market cap of $23.1 billion, Church & Dwight Co., Inc. (CHD) is an Ewing, New Jersey-based company that develops, manufactures, and markets household, personal care, and specialty products.

Companies worth $10 billion or more are typically classified as “large-cap stocks,” and CHD fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the household & personal products industry. The company distinguishes itself by its unique "Evergreen" business model that balances value-tier products with premium innovation. Its core strength lies in its strong portfolio of brands, including Arm & Hammer, OxiClean, Trojan, and Batiste, which dominate their respective categories through high consumer trust and low private-label exposure.

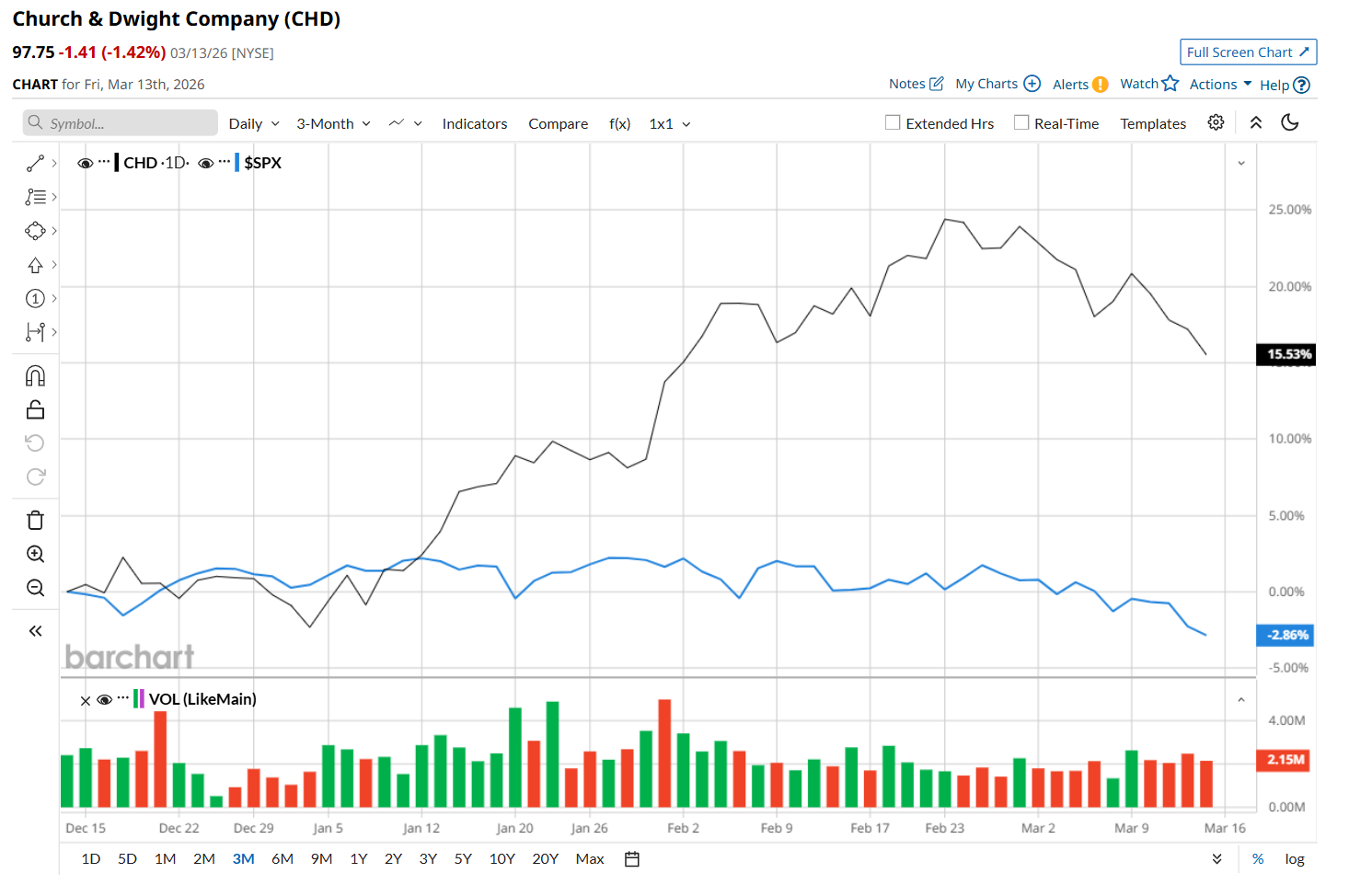

This consumer staples company is currently trading 14.2% below its 52-week high of $113.91, reached on Apr. 4, 2025. Shares of CHD have gained 15.5% over the past three months, considerably outperforming the S&P 500 Index’s ($SPX) 2.9% drop during the same time frame.

Moreover, on a YTD basis, shares of CHD are up 16.6%, compared to SPX’s 3.1% fall. However, in the longer term, CHD has fallen 10.9% over the past 52 weeks, notably lagging behind SPX’s 20.1% uptick over the same time frame.

To confirm its recent bullish trend, CHD has been trading above its 200-day moving average since mid-January, and has remained above its 50-day moving average since early January.

Shares of Church & Dwight climbed 4.7% on Jan. 30 following its Q4 earnings release. The company reported better-than-expected adjusted EPS of $0.86, supported by steady demand for both value-oriented and premium household and personal care products. Investor sentiment was further lifted by adjusted gross margin expanding by 90 basis points to 45.5%, along with management’s projection of around 100 basis points of additional margin expansion in 2026. The company also guided for organic sales growth of 3% to 4%, driven by volume, and adjusted EPS growth of 5% to 8% for 2026.

CHD has slightly underperformed its rival, The Procter & Gamble Company (PG), which fell 10.1% over the past 52 weeks. However, it has outpaced PG’s 5.4% YTD rise.

Looking at CHD’s recent outperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 20 analysts covering it, and the mean price target of $105.39 suggests a 7.1% premium to its current price levels.