/Unitedhealth%20Group%20Inc%20%20phone%20and%20site-by%20T_Schneider%20via%20Shutterstock.jpg)

UnitedHealth (UNH) has not had a healthy time for the better part of the last 12 months. The company has been rocked by the assassination of its CEO Brian Thompson in December 2024, as well as by the questioning of its policy practices, shareholder lawsuits, and Justice Department investigations. UNH shares are now down 44% on a year to date basis.

To compound matters further, analysts have been slashing their price target ahead of its second quarter earnings. Morgan Stanley’s Erin Wright cut the price target from to $342 from $374 earlier, citing ongoing challenges at UnitedHealth’s health services unit, Optum, and Wolfe Research trimmed its price target sharply to $330 from $363, warning about near-term earnings volatility and delayed sentiment recovery around the stock. Meanwhile, Barclays lowered its price target to $337 from $350, highlighting earnings pressure. All retained their “Buy” or “Outperform” ratings on the stock, though.

About UnitedHealth Stock

Over the past 20 years, the UNH stock has been a bona fide wealth creator for its shareholders, amassing share price growth of a whopping 450%. The company now operates through two segments, UnitedHealthcare and Optum.

While UnitedHealthcare offers health insurance plans, including Medicare Advantage and commercial products, Optum is a fast-growing services arm providing pharmacy benefits, care delivery, analytics, and IT services.

Additionally, it is the largest health insurer in the United States and ranked number one globally by revenue in the healthcare industry.

So, can UNH finally find its mojo back? I think it can and here’s why.

UNH Is Too Big to Ignore

As highlighted above, UnitedHealth commands a dominant position as the largest health insurer in the United States. That scale gives it real leverage in the market. But perhaps more important is how the company brings together two traditionally separate lines of business. UnitedHealth commands a level of coordination that pure-play insurers can’t match, allowing for operational synergies that offer both efficiency and flexibility.

In the first quarter of 2025, customer growth in UnitedHealthcare was particularly notable, rising by 780,000 individuals from the previous quarter. The total number now stands at 3.2 million. This uptick appears to be linked to strong uptake in some of the company’s more tailored healthcare offerings. The benefits of that growth are evident in the top-line momentum across all key business segments, including Optum Insight and Optum Rx.

Delving further into Optum, what makes the business even more interesting is its steady, contract-based revenue. Unlike insurance, which tends to be vulnerable to short-term medical cost volatility, Optum offers stability. At this point, nearly 43% of UnitedHealth’s operating income is being generated by its healthcare services division. And management has signaled clear intent to keep expanding this business. In 2025, they are aiming to add another 650,000 patients under value-based care agreements.

Broadly, demographic forces remain in UnitedHealth’s favor. As the U.S. population ages, the demand for integrated health solutions continues to rise. The company’s holistic model is well suited to meet that growing demand.

Still, there are concerns. UnitedHealth has been criticized for what some see as an unusually high claims denial rate, and that narrative could hurt its brand image with the possibility of consumers taking their business elsewhere. At the same time, financial ratios show pressure. The company’s combined ratio sits at 97.2%, which leaves little room for error. Also, in the first quarter, its medical care ratio came in at 84.8%, a slight increase from 84.3% a year earlier. That movement, though small, is negative for profitability since it indicates that the cost of providing care is rising faster than premiums.

Solid Fundamentals

UnitedHealth missed both revenue and earnings estimates in the most recent quarter.

Still, the company reported revenues of $109.6 billion in Q1, 2025, up $9.8 billion year over year. In terms of segments, Optum’s revenues were at $63.9 billion in the quarter, up from $61.1 billion, with an improvement in operating margins to 6.1% from 5.8%, in the year-ago period.

Earnings at $7.20 per share grew by 4.2% from the prior year but slightly missed the consensus estimate.

Coming to cash flows, in Q1 2025, UNH’s cash flow from operations surged to $5.5 billion compared to just $1.1 billion in the prior year as the company closed the quarter with a cash balance of $34.3 billion. This was much higher than its short-term debt of $9.9 billion.

However, a reduction in projected 2025 net earnings per share to be between $24.65 to $25.15 per share earlier is a concern. Yet, revenue estimates remained unchanged at $450 billion to $455 billion, the midpoint of which would denote yearly growth of 6.8%.

Also, UNH stock is trading at comfortable valuations. Its forward price-earnings ratio of 14.1x is nearly 40% below the sector median.

The company will report its Q2 2025 earnings on July 29.

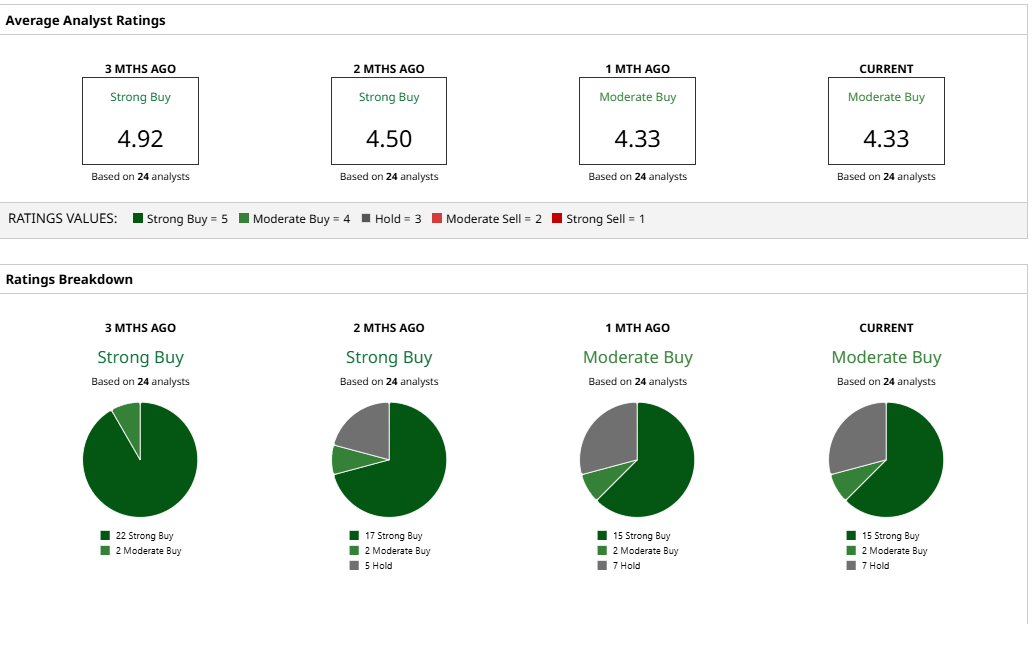

Analyst Opinions on UNH Stock

Overall, analysts have attributed a rating of “Moderate Buy” for UnitedHealth stock, with a mean target price of $358.70. This denotes uspide potential of about 27% from current levels. Out of 24 analysts covering the stock, 15 have a “Strong Buy” rating, two have a “Moderate Buy” rating, and seven have a “Hold” rating.