Louisville, Kentucky-based Brown-Forman Corporation (BF.B) manufactures, distills, bottles, imports, exports, markets, and sells various alcoholic beverages. Its offerings include wines, whiskey spirits, ready-to-drink cocktails, vodkas, gin, rum, brandy, bourbons, and more. With a market cap of $13.1 billion, Brown-Forman's operations span the Americas, Europe, Asia, and internationally.

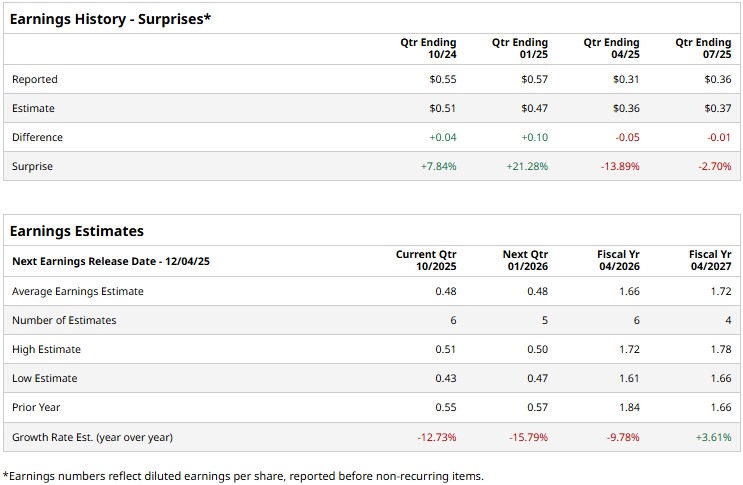

The company is expected to announce its second-quarter results by early December. Ahead of the event, analysts expect BF.B to report a profit of $0.48 per share, down 12.7% from $0.55 per share reported in the year-ago quarter. The company has a mixed earnings surprise history. It has surpassed the Street’s bottom-line estimates twice over the past four quarters while missing on two other occasions.

For the full fiscal 2026, analysts expect Brown-Forman to deliver an EPS of $1.66, down 9.8% from $1.84 reported in 2025. While in fiscal 2027, its earnings are expected to grow 3.6% year-over-year to $1.72 per share.

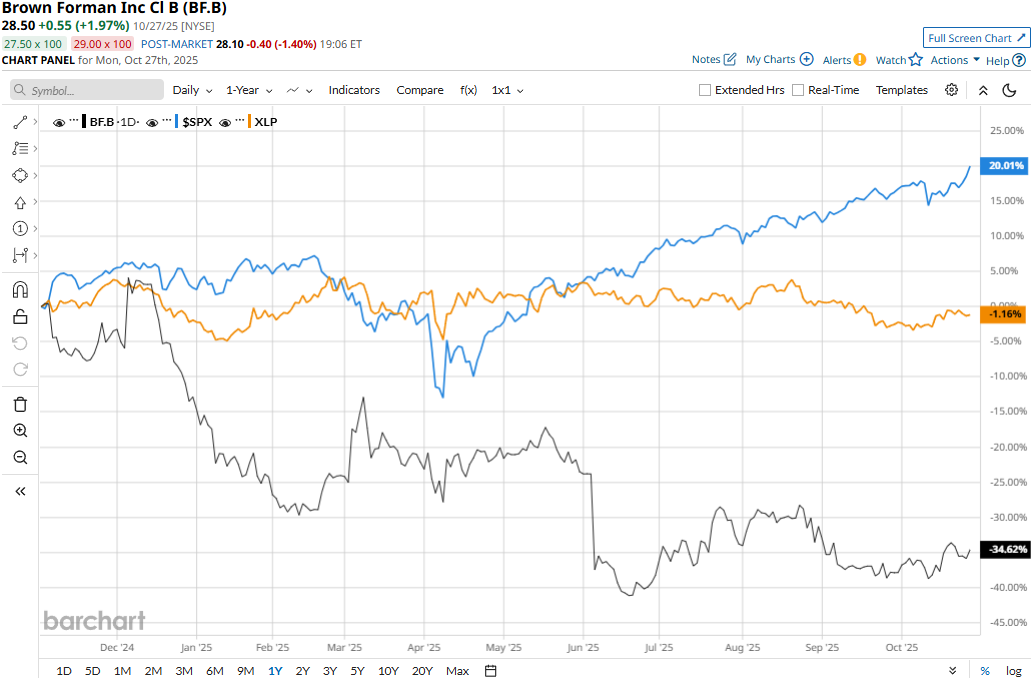

BF.B stock prices have tanked 41.1% over the past 52 weeks, notably underperforming the S&P 500 Index’s ($SPX) 18.4% gains and the Consumer Staples Select Sector SPDR Fund’s (XLP) 2.3% decline during the same time frame.

Brown-Forman’s stock prices dropped 4.9% in the trading session following the release of its mixed Q2 results on Aug. 28. Due to the conclusion of Brown-Forman’s business relationship with Korbel Champagne Cellars and the absence of a transition services agreement related to Sonoma-Cutrer and Finlandia, the company’s revenues observed a notable decline, which was partly offset by revenue gains in other areas. Its topline came in at $924 million, down 2.8% year-over-year, but 1.4% ahead of the Street’s expectations. Meanwhile, its EPS dropped 12.2% year-over-year to $0.36 and missed the consensus estimates by 2.7%, making investors jittery.

Analysts remain cautious about the stock’s prospects. Brown-Forman maintains a consensus “Hold” rating overall. Of the 18 analysts covering the stock, opinions include three “Strong Buys,” 12 “Holds,” one “Moderate Sell,” and two “Strong Sells.” Its mean price target of $31.93 suggests a 12% upside potential from current price levels.

On the date of publication, Aditya Sarawgi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.