With a market cap of $17.8 billion, Dollar Tree, Inc. (DLTR) is a leading discount retail company that operates the Dollar Tree and Dollar Tree Canada brands across the United States and Canada, offering a wide range of affordable everyday products. It provides consumables, variety merchandise, and seasonal items to meet customers’ daily household and shopping needs.

Shares of the Chesapeake, Virginia-based company have lagged behind the broader market over the past 52 weeks. DLTR stock has risen 2.3% over this time frame, while the broader S&P 500 Index ($SPX) has gained 23.6%. Moreover, shares of the company are down nearly 28% on a YTD basis, compared to SPX’s 7.7% rise.

Narrowing the focus, shares of Dollar Tree have underperformed the Consumer Staples Select Sector SPDR Fund’s (XLP) 3.9% return over the past 52 weeks.

Shares of DLTR rose 6.4% on Mar. 16 after the company reported stronger-than-expected Q4 2025 results, including Q4 net sales growth of 9.0% to $5.45 billion, same-store sales growth of 5.0%, and adjusted EPS jumping 21% to $2.56. Investors were also encouraged by the company’s full-year fiscal 2026 guidance, which projected comparable store sales growth of 3% to 4%, net sales of $20.5 billion to $20.7 billion, and adjusted EPS of $6.50 to $6.90. Additional optimism stemmed from Dollar Tree’s aggressive shareholder returns and expansion strategy, which included $1.55 billion in share repurchases during fiscal 2025, 402 new store openings, and the expansion of its multi-price format to approximately 5,300 stores.

For the fiscal year, ending in January 2027, analysts expect DLTR’s adjusted EPS to increase 17.4% year-over-year to $6.75. The company’s earnings surprise history is promising. It beat the consensus estimates in the last four quarters.

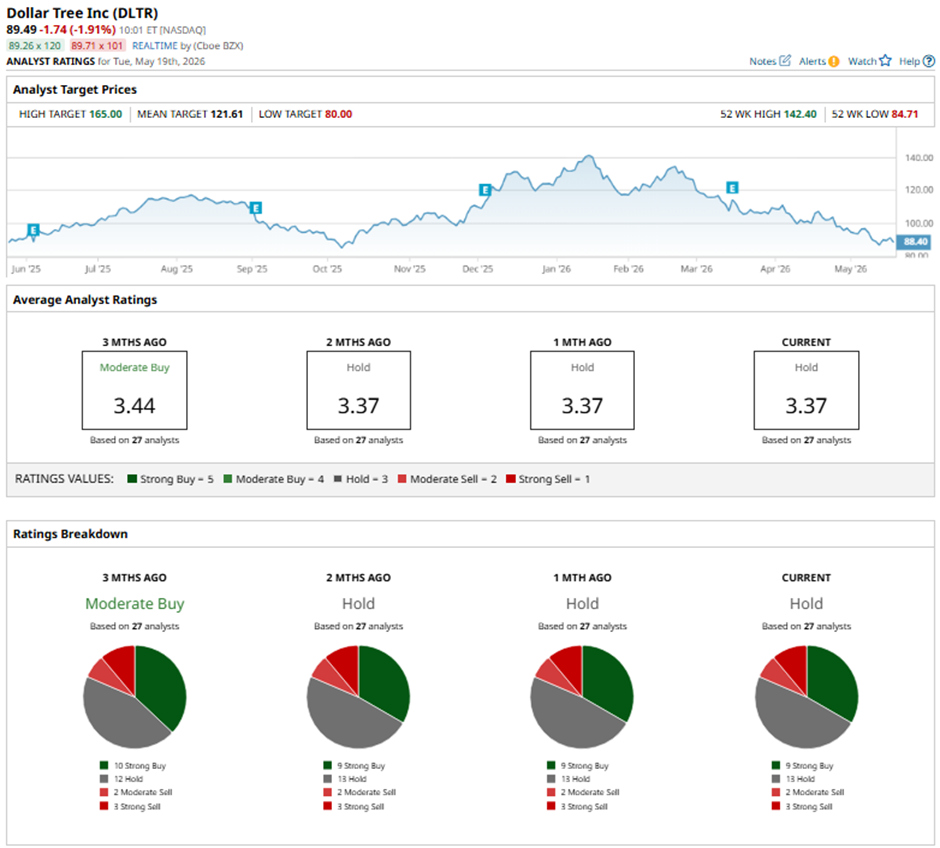

Among the 27 analysts covering the stock, the consensus rating is a “Hold.” That’s based on nine “Strong Buy” ratings, 13 “Holds,” two “Moderate Sells,” and three “Strong Sells.”

On May 18, Evercore ISI reduced its price target on DLTR to $140 while maintaining an “In Line” rating on the shares.

The mean price target of $121.61 represents a 35.9% premium to DLTR’s current price levels. The Street-high price target of $165 suggests a 84.4% potential upside.

.png?w=600)