-

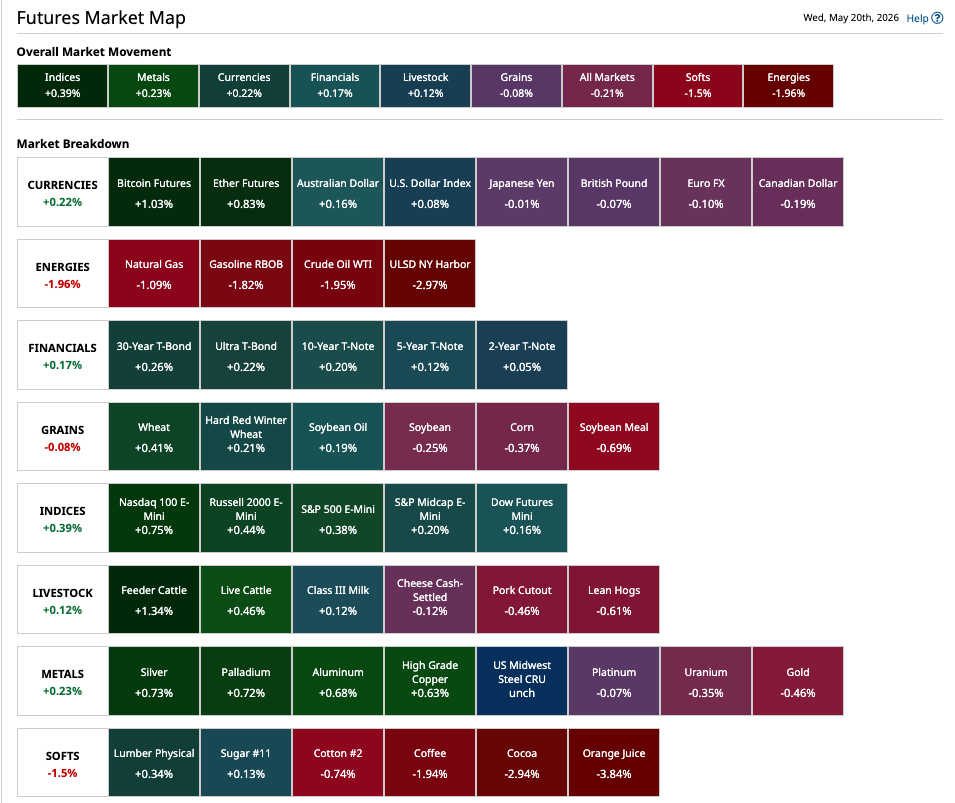

Given Indices were higher and Energies lower, my idea of what to expect with headlines didn't actually fit with what I saw.

-

Additionally, Treasury yields were lower to start the day while concerns over inflation risk continue to rise.

-

As for Grains, markets were generally under pressure despite a less favorable 6-to-10-day weather forecast.

Morning Summary: It’s early Wednesday morning, with dawn’s first light still an hour or more away as I fired up the computer and started to fill in this blank piece of electronic typing paper[i]. As usual, I ran the traps of the various sectors of the commodity complex, and given what I saw, I had a pre-conceived notion as to what I would find when I moved on to step two, checking the latest headlines. In a nutshell, Indices (US stock index futures) (ESM26) (YMM26) ((NQM26) were higher while Energies were lower across the board. My Blink reaction was financial news would be screaming about things like, “The US president says his War on Iran will be over in 10 days”, or something along that line. Instead I found, “Iran threatens to extend conflict ‘beyond the region’ if U.S. and Israel resume attacks”. I have a hunch threats coming from Tehran are taken a bit more seriously by global leaders than those emanating from the US White House. In other news, “Treasury yields inch lower as bond markets price ‘significant’ inflation risk”, though admittedly this makes no sense to me. As for Metals, gold (GCM26) was down $27 (0.6%) to start the day with silver (SIN26) up 61.5 cents (0.8%).

Corn: The corn market was in the red pre-dawn Wednesday. The July issue (ZCN26) posted a 6.0-cent trading range, relatively large for King Corn overnight, from up 1.75 cents to down 4.25 cents on trade volume of 26,000 contracts and was sitting 3.0 cents lower at this writing. Recall July closed 1.75 cents lower Tuesday followed by the National Corn Index coming in near $4.3575, down about 1.5 cents from Monday’s calculation and putting national average basis at 39.5 cents under July futures as compared to the previous 10-year low weekly close for this week of 39.0 cents under July. In other words, the basis market, the key read on real fundamentals, remains weak meaning there continues to be ample supplies in relation to demand as we approach the end of the 2025-2026 marketing year Q3. Over in new-crop we see both the September (ZCU26) and December (ZCZ26) issues also down 3.0 cents to start the day on lower overnight trade volume than what we’ve seen so far this week. What’s interesting about this is the extended 6-to-10-day weather forecast calls for above normal temperatures and below normal precipitation for much of the US Midwest (slide 2). But given the new dynamics of trade, maybe this isn’t that surprising after all.

Soybeans: The oilseed sub-sector was split evenly between red and green early Wednesday morning. Let’s set the stage by noting the spot-month diesel fuel contract (HOM26) is down 11.5 cents (2.8%) for seemingly no reason whatsoever. With that in mind, July canola is up $0.80 (0.1%) while July soybean oil is showing a gain of 0.19 cent (0.3%) at this writing. That all makes perfect sense, right? Meanwhile, July soybean meal is down $2.80 (0.8%) to start the day with the nearby July soybean issue (ZSN26) off 4.25 cents after sliding as much as 8.25 cents overnight. Regarding the latter, trade volume was light at about 16,000 contracts. A look back at Tuesday’s close and we see July finished 3.5 cents in the red followed by the National Soybean Index coming in near $11.4450, also down 3.5 cents from Monday. This left national average basis at 65.0 cents under July futures as compared to the previous 5-year low weekly close for this week of 61.25 cents under July. Again, the basis market remains weak heading toward the end of Q3. New-crop November (ZSX26) was down 4.25 cents after slipping as much as 8.0 cents overnight. Fundamentally, the Nov-January futures spread covered a neutral-to-bullish 38% calculated full commercial carry at Tuesday’s close.

Wheat: The wheat sub-sector was in the red across the board pre-dawn Wednesday. Why? Why not? It’s a day ending in “y”, and we are talking about wheat, so there doesn’t necessarily have to be a reason. In fact, it would not be surprising to see the markets back in the green by the time we reach intermission in a couple hours. As of this writing, the July HRW issue (KEN26) s down 3.5 cents after losing as much as 8.25 cents on trade volume of 2,200 contracts. That’s right, only 2,200 contracts. Let’s see how the rest of the day, this first day of the new positioning week, plays out. Fundametnally, HRW remains neutral to bearish. The latest national average basis calculations came in at 68.25 cents under July futures and 78.5 cents under September. For comparison, the previous 5-year low weekly close for this week is 66.5 cents under July and the first week of July at 57.75 cents under September. Keep this in mind with all the chatter about reduced HRW production this year. July SRW (ZWN26) was down 1.5 cents at this writing after sliding as much as 6.75 cents on trade volume of 13,300 contracts. That’s actually decent overnight activity, again indicating noncommercial interest in the market.

[i] And if you are familiar with the phrase “typing paper”, you were probably up as early as I was.