The market’s biggest story in 2026 hasn’t just been AI — it has also been the sudden return of energy risk. Oil now trades above $102 per barrel as the Iran war disrupts shipping through the Strait of Hormuz, the narrow waterway that normally handles roughly 20% of global crude flows. That surge in price has forced investors to rethink a sector that many had treated as yesterday’s trade.

Accordingly, when Berkshire Hathaway (BRK.A) recently revealed it had sold billions of dollars worth of energy giant Chevron (CVX) in the first quarter, investors immediately asked the obvious question: Is CEO Greg Abel losing faith in Big Oil? Or is he simply reshaping Berkshire’s portfolio for the post-Buffett era?

CEO Greg Abel Put His Stamp on Berkshire in Q1

According to Berkshire’s latest 13F filing, Greg Abel — the successor to investing legend and longtime CEO Warren Buffett — moved aggressively during Q1. In fact, the executive completely exited 16 positions, including UnitedHealth Group (UNH), Visa (V), Mastercard (MA), Domino's Pizza (DPZ), and Amazon (AMZN).

The Amazon exit was notable because Berkshire had already reduced its position by 77% in Q4 before eliminating the remaining shares in Q1. Many of the Q1 sales were tied to former Berkshire investing lieutenant Todd Combs, who left for JP Morgan Chase (JPM) in December 2025. Reports suggest Abel may have unwound roughly $14 billion in positions previously associated with Combs.

But Abel wasn’t simply liquidating stocks. The CEO also went shopping. Berkshire more than tripled its stake in Alphabet's (GOOGL) Class A shares and added a new position in Class C (GOOG) stock, while also adding new positions in Macy's (M) and Delta Air Lines (DAL).

This may be the most dramatic overhaul ever made in Berkshire's portfolio.

Chevron Was the Biggest Sale

The largest move wasn’t a complete exit, however. Berkshire cut its Chevron stake by 35% to 84.3 million shares, selling 45.7 million shares during Q1 worth more than $8 billion.

Berkshire still owns about $17 billion worth of CVX stock. That matters because, unlike some of the smaller liquidated holdings, Chevron has long been viewed as a Buffett-approved core position rather than a Todd Combs pick.

Chevron stock has rewarded shareholders nonetheless, with shares up almost 29% year-to-date (YTD) and 38% over the past 12 months as oil prices have surged amid conflict in the Middle East. Yet shares have slipped more than 5% since the end of Q1, showing just how volatile energy markets remain.

Why Chevron Still Looks Positioned to Win

Chevron’s advantage is that it works in both high-price and low-price oil environments. When crude prices climb above $100 per barrel, Chevron’s upstream drilling operations mint cash. When prices weaken, its downstream refining and chemicals businesses often expand margins because feedstock costs fall. Chevron has multiple ways to profit regardless of where oil goes.

The company returned $6 billion to shareholders in Q1 through dividends and buybacks while maintaining production growth following the Hess acquisition. Just as important, Chevron’s break-even oil price remains far below current crude prices, near the mid-$50 range. With Brent crude recently hovering above $100, profit margins remain wide.

The bigger wildcard is geopolitics. Saudi Aramco CEO Amin Nasser warned this month that disruptions in the Strait of Hormuz could impact global oil markets well into 2027 if shipping constraints persist. Oil tanker traffic through the strait has plunged from around 70 vessels daily to as few as five.

In any case, prolonged supply disruptions would likely support elevated oil prices — and Chevron’s earnings power.

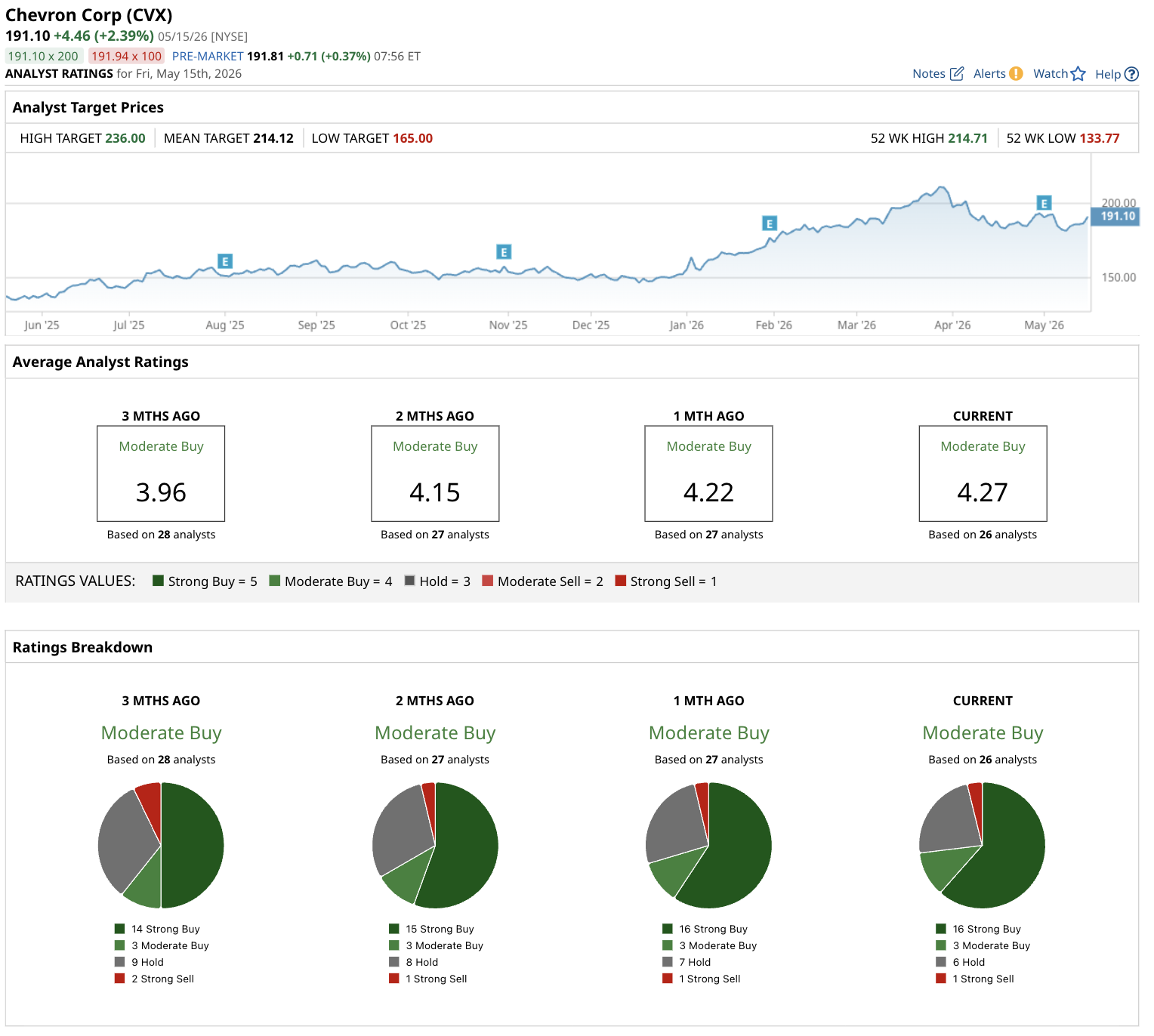

What Do Analysts Think About Chevron Stock?

Wall Street remains bullish on CVX stock despite the recent run-up, with a consensus "Moderate Buy" rating based on 26 analysts. The mean price target of $214.12 implies 9% potential upside from current levels. Meawnwhile, the high target of $236 implies 20% potential upside if oil prices remain elevated into 2027, while the low target of $165 suggests 16% downside risk thanks to Chevron’s integrated business model and dividend support.

Chevron currently yields 3.81%, which remains higher than the broader S&P 500’s ($SPX) average forward yield closer to 1%.

Granted, energy stocks always carry commodity risk. If oil prices collapse, Chevron shares would likely retreat with them. That said, the firm's diversified operations and low break-even costs give it more resilience than many pure-play producers.

The Bottom Line

In short, Greg Abel’s first major quarter running Berkshire’s portfolio showed investors exactly how willing he is to make bold moves. Selling 16 stocks outright grabbed headlines, but trimming billions worth of Chevron while still holding a massive $17 billion stake may tell investors even more.

Berkshire doesn’t appear to be abandoning Chevron. It appears to be managing position size after a powerful rally while keeping exposure to an energy market that could remain tight for years.

And if oil disruptions continue into 2027, Chevron may still prove to be one of Berkshire’s most important holdings.