/W_R_%20Berkley%20Corp_%20phone%20and%20site-by%20T_Schnedier%20via%20Shutterstock.jpg)

W. R. Berkley Corporation (WRB), headquartered in Greenwich, Connecticut, is an insurance holding company that operates as a commercial line writer. Valued at $25.6 billion by market cap, the company offers property casualty insurance and reinsurance products.

Shares of this leading property casualty insurance holding company have underperformed the broader market over the past year. WRB has declined 7.2% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 23.3%. In 2026, WRB stock is down 2.3%, compared to the SPX’s 7.4% rise on a YTD basis.

Narrowing the focus, WRB’s underperformance is also apparent compared to the Invesco KBW Property & Casualty Insurance ETF (KBWP). The exchange-traded fund has declined about 3.1% over the past year. Moreover, the ETF’s 4.7% losses on a YTD basis outshines the stock’s dip over the same time frame.

WRB’s Q1 reflected a more competitive insurance market, with CEO W. Robert Berkley, Jr. noting increased pressure from national carriers in property and casualty lines. Despite pricing challenges, disciplined underwriting, lower catastrophe losses, and record investment income supported results. Management is now rethinking its balance of rate vs. growth, signaling a potential shift toward selective exposure growth in segments where margins are attractive, while staying cautious on tougher lines like commercial auto and workers’ comp. The focus remains on cycle management, underwriting discipline, and prudent capital deployment as competition reshapes the landscape.

On Apr. 21, WRB shares closed down more than 1% after reporting its Q1 results. Its adjusted EPS of $1.30 surpassed Wall Street expectations of $1.13. The company’s revenue stood at $3.7 billion, up 4% year over year.

For the current fiscal year, ending in December, analysts expect WRB’s EPS to grow 7.6% to $4.66 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in three of the last four quarters while missing the forecast on another occasion.

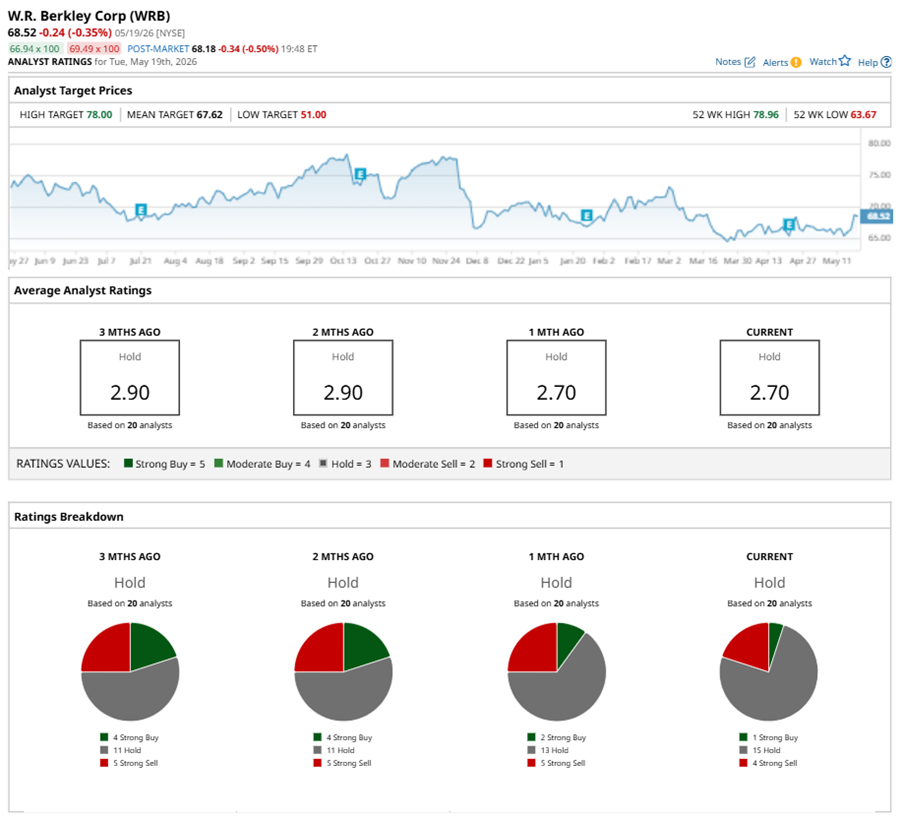

Among the 20 analysts covering WRB stock, the consensus is a “Hold.” That’s based on one “Strong Buy” rating, 15 “Holds,” and four “Strong Sells.”

This configuration is less bullish than a month ago, with two analysts suggesting a “Strong Buy,” and four advising a “Strong Sell.”

On Apr. 27, UBS kept a “Neutral” rating on WRB and lowered the price target to $68.

While WRB currently trades above its mean price target of $67.62, the Street-high price target of $78 suggests a 13.8% upside potential.