/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

Micron Technology (MU) has witnessed considerable growth, with its stock climbing nearly 40% year-to-date, well ahead of the broader S&P 500 Index’s ($SPX) 9.5% gain. The notable surge in MU stock reflects solid demand for its memory chips and storage solutions, a trend supported by the rapid buildout of data centers and a recovery in consumer markets like PCs and smartphones.

Despite this significant growth, MU stock still appears attractively priced. Furthermore, Micron’s management recently lifted its outlook for the fourth quarter, projecting higher revenue, stronger margins, and improved earnings per share.

This upbeat guidance suggests that the pricing and demand momentum for its products remains intact and could extend into the coming quarters, supporting its growth.

Micron Benefitting From AI-Driven Demand Expansion

Micron is benefiting from data center expansion, primarily driven by significant growth in artificial intelligence (AI) servers. In Q3, the data center revenue more than doubled year-over-year, reflecting the growing demand for its products in the AI infrastructure space.

A key driver has been Micron’s high-bandwidth memory (HBM) products, which are essential for training and running large AI models. The company has scaled production of its HBM3E line, now shipping in high volumes to major chipmakers. Looking ahead, its next-generation HBM4 is already sampling with customers and promises higher speeds and lower power consumption. With mass production scheduled for 2026, HBM4 could help maintain Micron’s leadership in this fast-growing market.

Micron’s growth story extends well beyond data centers. In PCs, demand is strengthening as AI-enabled laptops hit the market and the Windows 11 upgrade cycle gathers pace. Micron is gaining share in client solid-state drives (SSDs), a trend that should continue to lift results.

The mobile segment is another bright spot. With AI pushing up memory needs in smartphones, Micron’s advanced DRAM and NAND solutions are increasingly in demand for flagship devices. Its latest LP5X memory is already shipping and seeing strong uptake.

Automotive and industrial markets are also contributing to growth. As cars incorporate more advanced driver-assistance systems and factories adopt AI-driven automation, demand for high-performance memory is climbing. Micron’s innovations, such as dual-LP5 DRAM, position it well to capture this opportunity.

MU’s Healthy Supply-Demand Balance

Market dynamics are working in Micron’s favor. Notably, inventory levels across its customer base remain balanced, reducing the risk of a supply glut. At the same time, the ramp-up in HBM production is creating tightness in other types of memory, particularly DDR5. That supply squeeze is giving Micron greater pricing power.

DRAM demand is expected to climb at a high-teens rate in 2025, with NAND growing in the low double digits. Over the medium term, both markets are projected to expand at a mid-teens pace. With Micron carefully managing its supply growth, pricing conditions could remain favorable.

Micron’s Guidance Signals More Upside

Micron has raised its Q4 FY2025 outlook, signaling stronger-than-expected momentum. The company now projects revenue of $11.2 billion plus or mind $100 million, up from its prior forecast. Adjusted gross margin guidance has improved to 44.5% plus or minus 0.5% (from 42% plus or minus 1%). At the same time, adjusted EPS is expected at $2.85 plus or minus $0.07, versus the earlier $2.50 plus or minus $0.15.

The upgrade reflects strong DRAM pricing and solid execution, supported by surging demand from AI and data centers. Hyperscalers continue to invest in AI servers and infrastructure, creating strong demand and a tailwind in pricing for the company.

Micron Stock Is Too Cheap to Ignore

Micron stock has registered notable gains in 2025. However, the drivers of its growth, including AI adoption, robust data center spending, and rising memory requirements across devices, show no signs of slowing. With pricing momentum strong and new products on the horizon, Micron looks positioned to extend its gains into 2026 and beyond.

Micron currently trades at a forward price-earnings ratio of just 16.25x. That’s a modest multiple for a company expected to deliver solid earnings growth. Analysts forecast Micron’s earnings per share will climb nearly 73% in fiscal 2026, suggesting that the stock remains deeply undervalued.

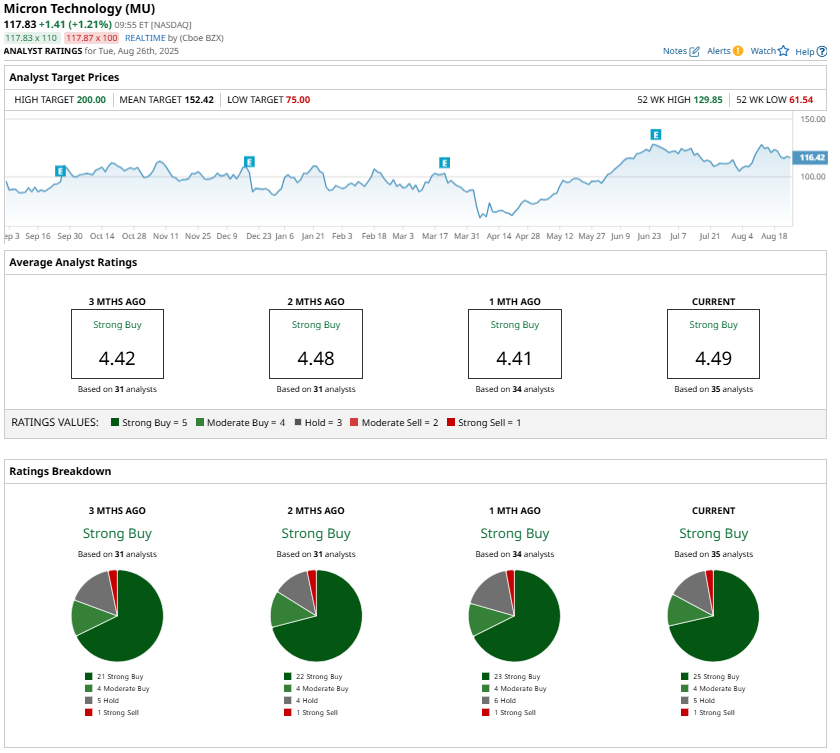

Wall Street is bullish about MU stock, and analysts maintain a “Strong Buy” consensus rating.