With the rising popularity of equities market trading following the COVID-19 pandemic, it was practically inevitable that interest would boom toward the options space. In many ways, options represent a market within a market. Since the underlying contracts exchange hands at a fraction of the rate of the actual security, the leverage can be tremendous.

At the same time, unlike securities in the open market, options expire. So while there are incredible rewards to be had, the debit that you put can be completely nuked in a busted transaction. Even worse, in a credit-based position, tail risk — which is the phenomenon where you must make good on the risk you underwrote — can potentially beat your portfolio to a pulp.

Therefore, people turn to indicators like Barchart’s Unusual Stock Options Volume screener to find potential opportunities. Fundamentally, it’s a smart strategy because the options market tends to be the arena of the smart money. So, if you can decipher where the most intelligent traders are putting their funds, you can potentially gain an edge over everyone else.

To be sure, interpreting unusual activity in the derivatives arena is both an art and a science. Here’s the rub. Even if you were the world’s best expert on the financial markets, you would know instinctively that there’s no way all 500 stocks identified as “unusual” represent compelling wagers. There has to be another mechanism to sort the wheat from the chaff.

I believe that energy giant BP (BP) is the only enterprise from Monday’s list that passed the sniff test.

Let’s quickly go over the stats since this is a story about unusual options activity and all. Yesterday, BP’s total options volume hit 58,533 contracts, representing a lift of 215.73% over the trailing one-month average. Call volume stood at 47,156 contracts while put volume was 11,377 contracts, generating a put/call ratio of 0.24.

Again, I’m not going to be overly excited but you should know that on Monday, options flow — which focuses exclusively on big block transactions likely placed by institutional investors — showed that net trade sentiment stood at more than $1.05 million above parity. This metric favors the bulls so the above ratio could be read intuitively.

Okay, with the details out of the way, I’m going to get to the good stuff.

BP Stock Flashes a Statistically Significant Signal

One of the common traps that you’ll find in the broader financial publication space is the concept that bullish options flow (or insert any other line of reasoning, such as a cheap earnings multiple) is automatically a “good” opportunity. However, if the analyst making the assertion fails to define what “good” means, the argument is likely to be a presuppositional fallacy.

Essentially, merely stating that bullish options flow makes BP stock a “good” opportunity smuggles the conclusion (that BP is favorably mispriced) into the premise (that there is an objective standard in the market for what “good” means).

If you really break down the argument, it’s basically stating that BP stock is good because it has bullish options flow, implying that bullish flow is good because it means BP is good. This type of circular logic — also known as begging the question — runs up and down the financial publication industry.

Go read the articles and find out for yourself. Heck, read my articles before my red pill moment, which occurred around April of this year.

As far as I’m aware, the only objective truth in the equities sector is that, at the end of the day, the market is either a net buyer or a net seller. It’s kinesis or stasis, one or the other.

Yes, this may seem like an obvious point but with this framework, we can now much more easily observe recurring patterns and their forward probabilities. For example, in the past 10 weeks, the market voted to buy BP stock four times and sell six times. Despite distributive sessions outweighing accumulative, the overall trajectory of BP was upward. For brevity, we can label this sequence 4-6-U.

Now, we all understand that the probability of upside under all conditinos is not a fixed percentage. Have you seen baseball or any team sports in general? Then you know that certain players (the great ones) rise to the occasion. I want to know when BP is in clutch mode and when it’s not. To do this, I need to create a decision-tree logic across 10-week intervals (in this case, going back to January 2019):

L10 Category |

Sample Size |

Up Probability |

Baseline Probability |

Median Return if Up |

1-9-D |

8 |

37.50% |

44.77% |

1.73% |

2-8-D |

24 |

41.67% |

44.77% |

4.65% |

3-7-D |

39 |

56.41% |

44.77% |

1.37% |

3-7-U |

4 |

50.00% |

44.77% |

7.70% |

4-6-D |

63 |

36.51% |

44.77% |

2.38% |

4-6-U |

29 |

62.07% |

44.77% |

1.79% |

5-5-D |

24 |

33.33% |

44.77% |

2.12% |

5-5-U |

54 |

48.15% |

44.77% |

2.86% |

6-4-D |

7 |

42.86% |

44.77% |

2.72% |

6-4-U |

50 |

44.00% |

44.77% |

2.11% |

7-3-U |

14 |

14.29% |

44.77% |

3.15% |

From the table above, the chance that a long position in BP stock will rise is only 44.77%, a negative bias. This is effectively our null hypothesis, the assumption of no mispricing. In contrast, our alternative hypothesis is that because the 4-6-U sequence is flashing, the upside probability for the following week is actually 62.07%. Therefore, an incentive exists to consider a debit-based options strategy.

Assuming the positive pathway, the median return is 1.79%. If so, that would imply that BP stock may poke its head above the $33 level quickly.

Putting the Math to Good Work

Based on the market intelligence above, a sensible idea is to consider the 32/33 bull call spread expiring Sep. 19. This transaction involves buying the $32 call and simultaneously selling the $33 call, for a net debit paid of $54 (the most that can be lost in the trade). Should BP stock rise through the short strike price ($33) at expiration, the maximum profit is $46, a payout of over 85%.

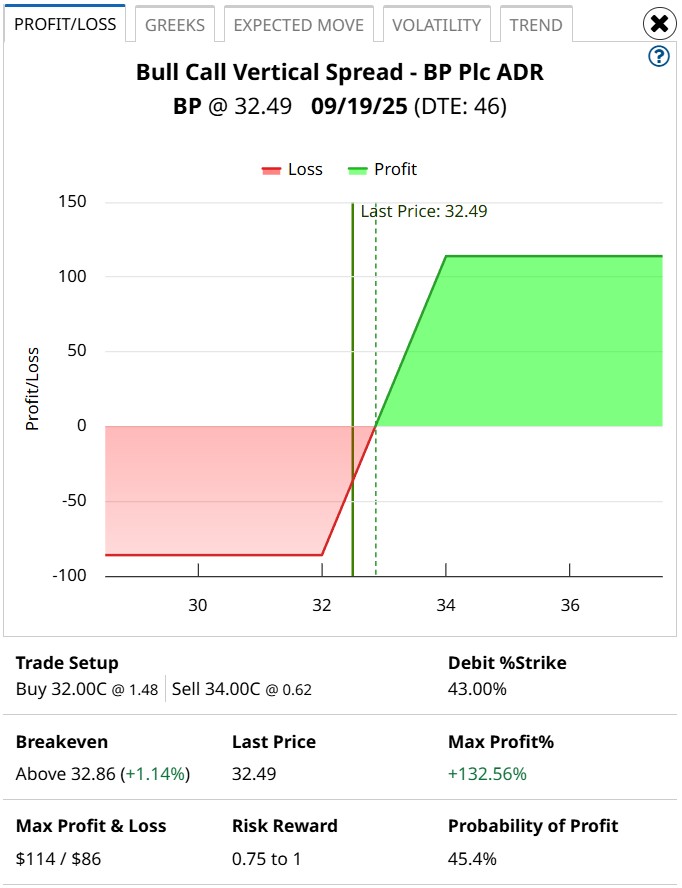

However, the most aggressive traders may consider the 32/34 bull spread also expiring on Sept. 19. This trade calls for a net debit of $86, which is pricier than the 32/33 spread. However, the max payout stands at roughly 133%, which is a very tempting proposition. The breakeven for this trade is $32.86, which as mentioned earlier is a realistic target.

I mentioned in the title that BP stock passed the quantitative sniff test and that’s not clickbait. Running a one-tailed binomial test on the 4-6-U sequence reveals a p-value of 0.0478. This means that there’s a 4.78% chance that the implications of the sequence could materialize randomly as opposed to intentionally.

Scientists will scoff at this ratio and state that it barely falls under the threshold of statistical significance of 5%. Yet in the context of an open, entropic system like the stock market, this is an awfully compelling signal. No, it doesn’t guarantee a positive outcome. However, the usage of Markovian principles helps to rationalize your wagers rather than depending on empirically unanchored opinions and vibes.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.