Cancer remains one of the most relentless challenges in modern medicine. In 2025, over 2 million new cancer cases are expected to be diagnosed in the United States. More than 618,000 people will die from the disease, which is equivalent to about 1,700 deaths each day. The scale of this health crisis is driving substantial investments and innovation in cancer research and treatment.

As a result, the global oncology market is projected to reach $208.9 billion in revenue by 2025, with forecasts suggesting it could surpass $900 billion by 2034. This growth is fueled by increased cancer incidence, advances in precision and immunotherapy drugs, and billions of dollars in new partnerships and funding, such as Bristol-Myers Squibb’s (BMY) recent $11 billion stake in next-generation cancer therapies.

High-potential cancer specialists like Elicio Therapeutics (ELTX), Cellectis (CLLS), and Autolus Therapeutics (AUTL) are earning coveted “Strong Buy” analyst ratings. Despite this recognition, each remains well below large-cap valuations, which leaves ample room for sharp upside if upcoming clinical and regulatory catalysts play out in their favor. Could one of these under-the-radar biotech firms deliver the next big breakthrough in cancer treatment — and major upside for investors? Let’s dive into these three cancer biotech stocks now.

Elicio Therapeutics

Elicio Therapeutics (ELTX) is a clinical-stage biotech pioneering immunotherapies for solid tumors, with a market capitalization of $158 million.

ELTX has posted a YTD gain of 92.7%, and is up 102.6% over the past 52 weeks. Its price-book ratio stands at an elevated 17.6x, well above the sector median of 2.47x.

Elicio’s lead asset, ELI-002 7P, is advancing through the pivotal Phase 2 AMPLIFY-7P trial targeting pancreatic ductal adenocarcinoma (PDAC), with a critical interim analysis focused on disease-free survival slated for Q3 2025. This interim analysis is a key milestone for the company, particularly for its potential impact on PDAC. Ahead of this readout, H.C. Wainwright analyst Robert Burns reiterated a “Buy” rating on shares and maintained his $13 price target.

Elicio reported Q1 2025 R&D expenses of $7.8 million, a slight increase from $7.6 million in Q1 2024, tied primarily to the ongoing Phase 2 AMPLIFY-7P trial. General and administrative expenses grew to $3 million, up from $2.7 million due to higher personnel costs. The Q1 2025 net loss narrowed to $11.2 million, compared to $11.8 million in the same quarter last year, with a net loss per share improving to $0.87 from $1.15.

Notably, ELTX augmented its financial position in Q2 by securing a $10 million senior secured note, extending its operational runway into early 2026 and granting the company flexibility for near-term initiatives.

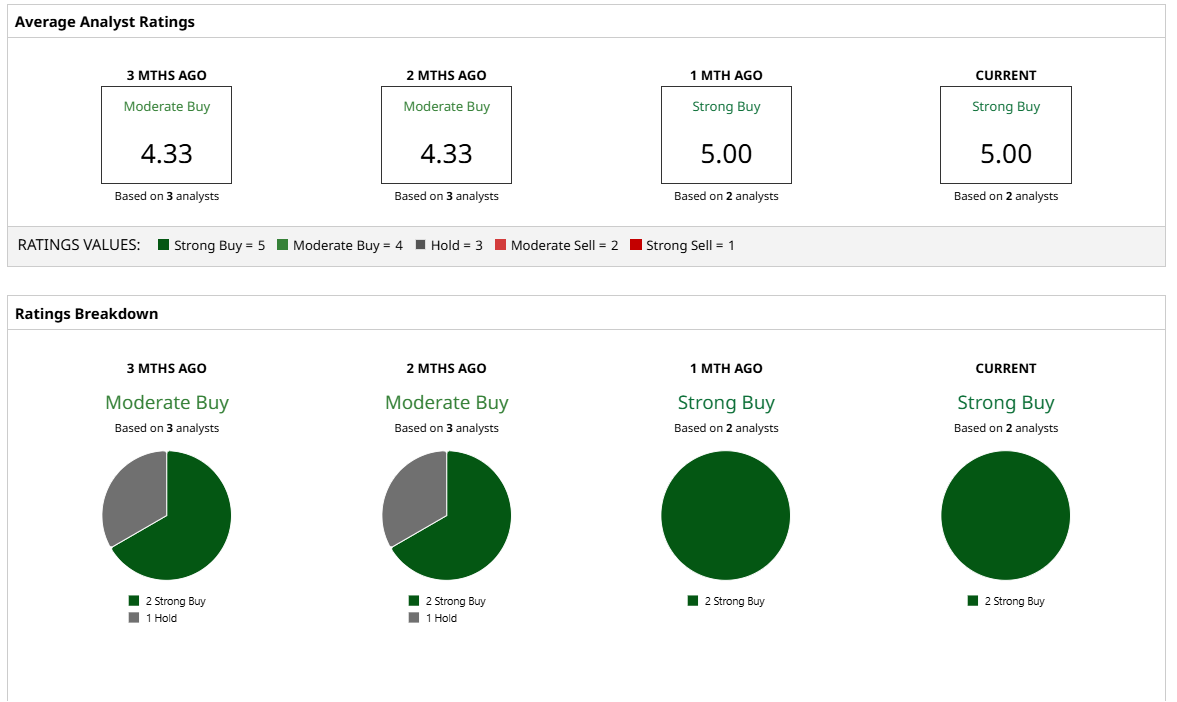

Analyst sentiment skews highly bullish as the two surveyed analysts assign ELTX a “Strong Buy” rating, with an average price target of $12.50. This places the upside potential at approximately 26% from current levels.

Cellectis

Cellectis (CLLS) is a clinical-stage biotech company specializing in gene-edited cell therapies with a market capitalization of approximately $140 million. The stock has gained 60% in the year to date, and shares are up 25.2% in the past 52 weeks.

Cellectis has a price-sales ratio of 2.26x, below the sector median of 3.6x, and a price-book ratio of 0.96x, significantly under the sector median of 2.47x, suggesting potential undervaluation relative to its peers.

CLLS reported solid results for Q1 2025, with consolidated revenues and other income rising to $12 million from $6.5 million a year prior. This increase mainly stems from $5.9 million recognized under the AstraZeneca Joint Research Collaboration Agreement (AZ JRCA).

Its cash reserves stood at $246 million as of March 31, 2025, projected to sustain operations well into the second half of 2027, providing ample runway for ongoing development. Research and development expenses slightly decreased to $21.9 million compared to the previous year, reflecting efficient management despite continued investment in pipeline advancement and manufacturing capabilities in Paris and Raleigh.

Strategically, Cellectis’ partnership with AstraZeneca is a cornerstone of its growth story. AstraZeneca’s $140 million investment enhances Cellectis’ financial footing and grants AstraZeneca exclusive rights to 25 genetic targets, with options to develop up to 10 candidate products. So far this collaboration is advancing two CAR-T programs aimed at hematological malignancies and solid tumors.

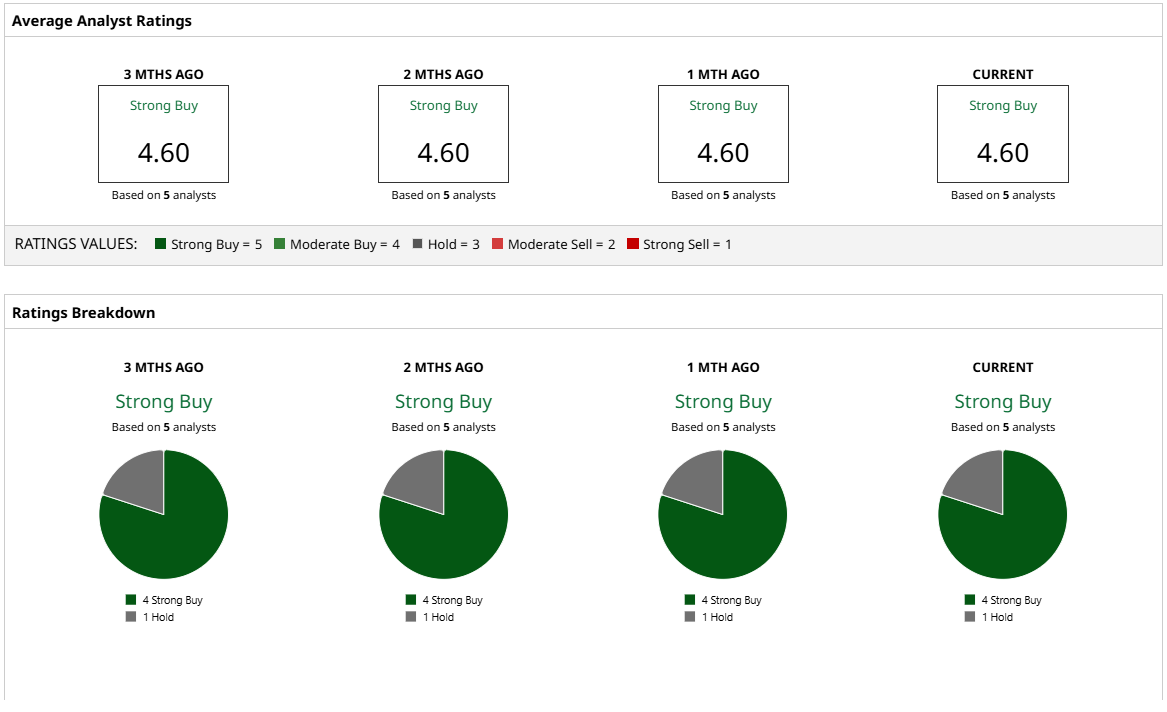

Analyst sentiment is unanimously bullish, with the five surveyed analysts assigning Cellectis a consensus “Strong Buy” rating. The average price target of $5.60 implies compelling upside of approximately 91% from the current share price.

Autolus Therapeutics

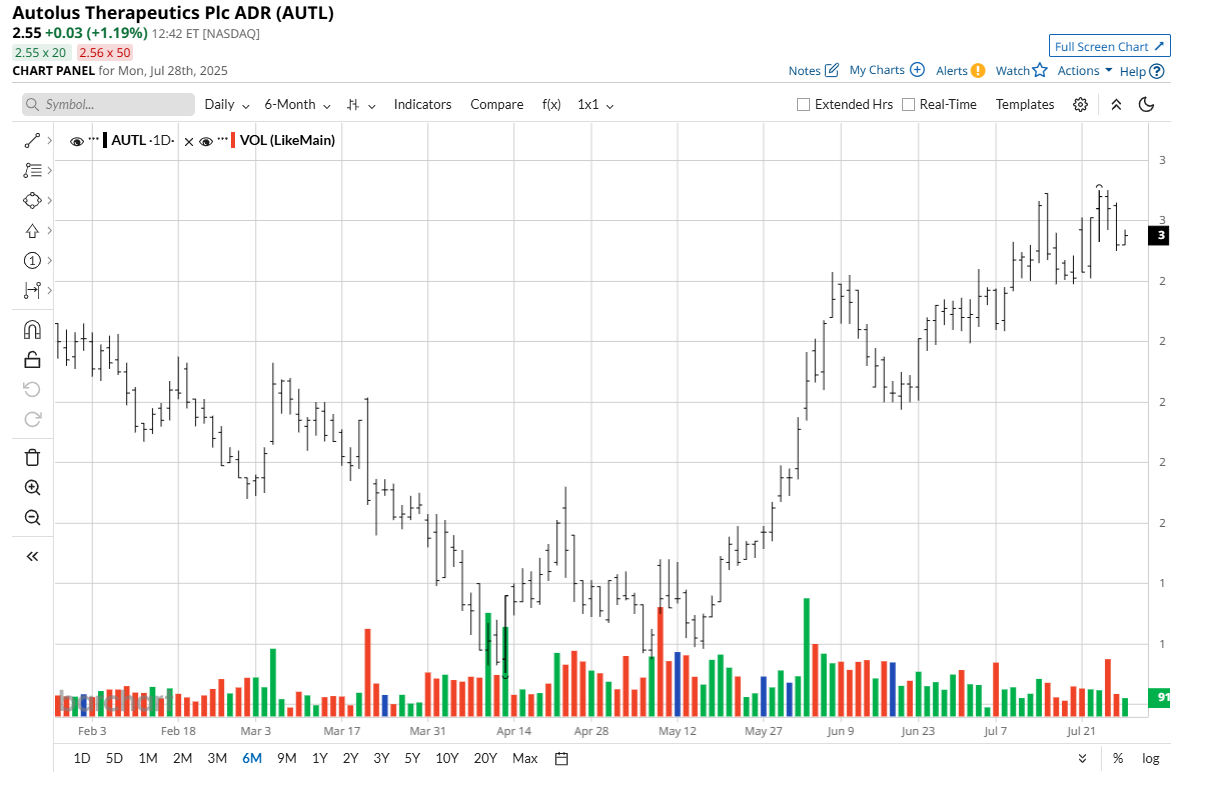

Autolus Therapeutics (AUTL) develops advanced autologous CAR-T cell therapies for blood cancers, with a market capitalization of $670 million. The stock is up 8.7% year-to-date, but down 45% over the past 52 weeks.

Its price-sales ratio of 69.4xx is markedly above the sector’s 3.54x median, while its 1.89x price-book ratio remains below group averages of 2.47x.

In Q1 2025, Autolus reported $9 million in net product revenue, driven largely by the commercial rollout of AUCATZYL (Obe-cel), its lead CAR-T therapy, across 39 fully activated U.S. centers. Patient access continues to grow, capturing coverage for roughly 90% of U.S. medical lives as payer uptake accelerates. Costs of sales totaled $18 million, including delivered but as-yet-unrecognized product tied to deferred revenue and royalty obligations, a natural part of early stage commercial launches.

Research and development expenses dropped to $26.7 million from $30.7 million year-over-year, with much of that shift driven by the transition of manufacturing expenses to sales costs. Loss from operations widened to $65.2 million due to launch investments, and net loss reached $70.2 million or $0.26 per share.

On the regulatory front, Autolus scored a critical win in July as AUCATZYL secured European approval for adults with relapsed or refractory B-cell precursor acute lymphoblastic leukemia. This unlocks a larger addressable market and enhances the company’s global competitive position in engineered cell therapies.

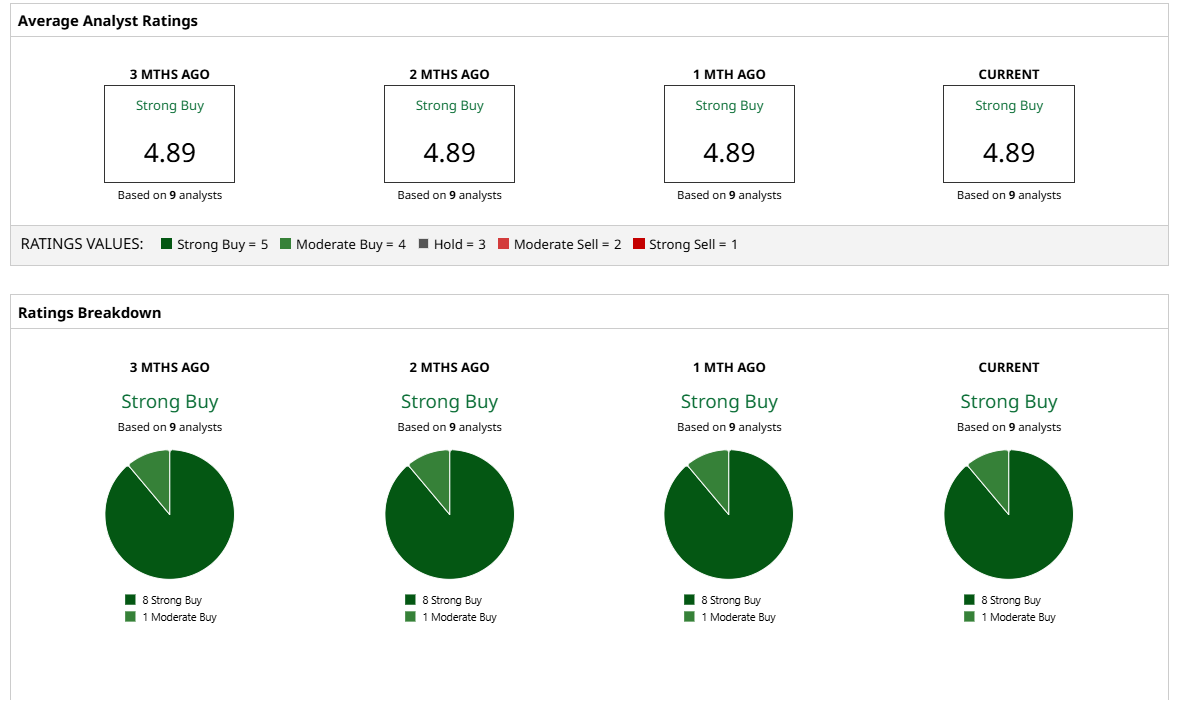

The analyst outlook remains unequivocally positive as the nine surveyed analysts rate AUTL a consensus “Strong Buy,” with a mean target of $9.84, implying 285% upside potential from current levels.

Conclusion

With major catalysts ahead and strong analyst backing, the odds favor upward momentum as data readouts and commercial expansion play out. Given their positioning and partnerships, these three stocks could deliver outsized gains in the coming quarters, especially if results come in strong.