I do not enjoy holding views that differ from those of others. It is never comfortable to be the odd one out because I have to defend my analysis vigorously and, at times, endure ridicule from my peers.

That happened in 1997 when I argued, against the prevailing consensus, that Thailand’s economy would collapse and the baht could not remain fixed at 25 to the US dollar. At the time, all research houses maintained the economy was sound, with GDP growth of around 7%. I predicted negative growth. The reason, which proved correct, was inadequate domestic liquidity caused by excessive reliance on foreign borrowing.

The same situation may arise again. I am confident GDP growth will be negative this year, while all research houses, including the Bank of Thailand (BoT), forecast growth of more than 2%. However, I will not discuss GDP forecasts in this article. Instead, this is a prelude to that discussion, focusing on the issue of the twin deficits: the fiscal deficit and the current account deficit.

Originally, I intended to discuss only the current account deficit. However, the two deficits are closely intertwined, making it appropriate to examine the fiscal deficit as well. With parliament currently considering the 2027 fiscal budget, I would also like to offer a few words of caution.

The 2027 budget is, in many respects, much the same as the 2026 budget. It offers little indication of any attempt to change Thailand’s economic trajectory. It is simply more of the same. Total expenditure amounts to 3.788 trillion baht, just 0.2% higher than last year’s budget.

Current expenditure accounts for 73.6% of total spending, leaving capital expenditure — the investment needed to build the country’s future — at only 20.8% of the budget. Is this really a budget for the future? Where is the investment needed to achieve that goal?

The 2027 budget requires 788 billion baht in new borrowing, equivalent to an estimated 3.8% of GDP. This comes on top of the 860 billion baht fiscal deficit for 2026 and an additional 400 billion baht in borrowing for the Thais Help Thais Plus and Energy Transformation programmes. Given these enormous financing requirements, who in Thailand has both the resources and the willingness to purchase that volume of government bonds?

The answer is: not enough. This is, and will remain, the key threat to fiscal stability in the 2026 and 2027 fiscal years. Even if investors with substantial funds, such as foreign institutions, can be found, would they be willing to buy Thai government bonds when yields are well below inflation? The five-year government bond yields about 1.5%, while inflation is around 3%. The yield is even lower than that on comparable Japanese government bonds, let alone the 4.2% yield on a five-year US Treasury note. Thailand could eventually face a situation similar to Japan’s, where the Bank of Japan has had to purchase the overwhelming majority of government bond issuance (97%) because market yields are too low to attract sufficient investors.

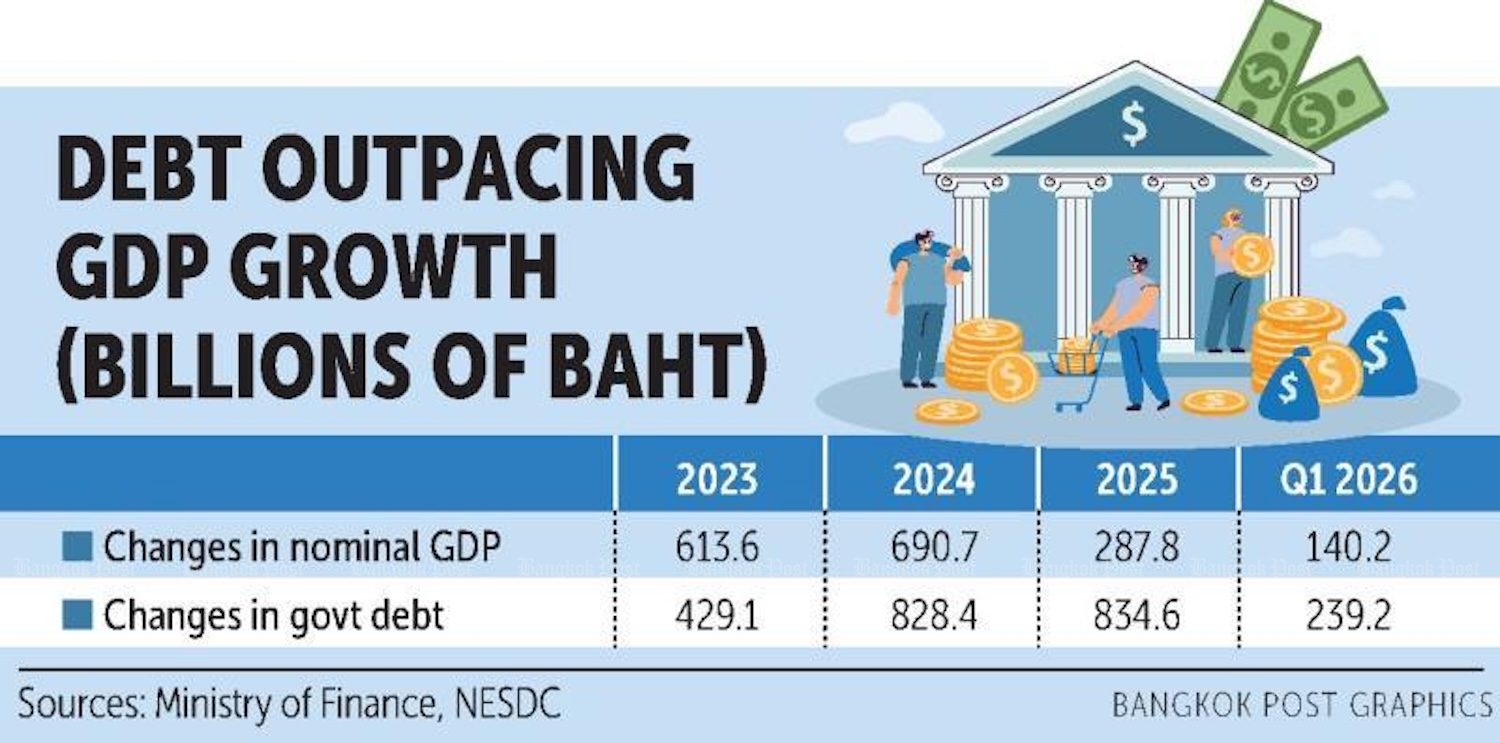

An examination of government debt and GDP provides an interesting perspective. The table above compares changes in nominal GDP with changes in government debt between 2023 and the first quarter of 2026. Three conclusions emerge. First, the Thai private sector has effectively stalled since 2023 and is no longer capable of driving economic growth. Government support has become indispensable.

Second, if Thailand is to achieve positive GDP growth, the government must continue borrowing heavily, as virtually all recent growth has been financed through public debt.

Third, fiscal deficits are becoming progressively less effective in generating economic output. By the first quarter of 2026, every one baht of additional government borrowing generated only 0.59 baht of GDP (see table).

The table shows that, with the private sector largely paralysed, fiscal deficits have become the economy’s life support system. Remove that support and the economy risks grinding to a halt. The critical question is how these deficits can continue to be financed. Over just three years and one quarter, government debt has increased by 2.33 trillion baht.\

How much additional borrowing capacity remains? Can the economy finance another 788 billion baht of borrowing in the 2027 fiscal year? Moreover, the 2026 fiscal year has not yet ended, and a further 485 billion baht in borrowing will still be required. In my view, the answer is highly unlikely, for two reasons.

First, the so-called excess liquidity has already been exhausted. The finance minister and the BoT governor have argued Thailand had around 1 trillion baht of excess liquidity available to finance government borrowing. I believe that liquidity has already been absorbed by the 860 billion baht fiscal deficit for 2026 and the additional 172 billion baht required for the Thais Help Thais Plus programme. In other words, there is no excess liquidity left to finance the 2027 budget deficit.

Second, Thailand’s principal external source of income — its current account surplus — is unlikely to be available this year. In 2025, Thailand recorded a current account surplus of US$15.9 billion, equivalent to around 530 billion baht. That external inflow helped finance last year’s government deficit of 834 billion baht. The BoT projects the current account balance will fall to zero in 2026 because of higher oil import costs. I reach a very different conclusion. My estimates suggest not a balanced current account but a deficit of $21.9 billion.

That may sound pessimistic, but the figures already point in that direction. During the first five months of the year, the current account was already $12.4 billion in deficit. June is also likely to record a deficit of about $6 billion, leaving the first-half shortfall at around $18 billion. For the BoT’s projection of a balanced current account for the full year to prove correct, Thailand would need to generate a surplus of $18 billion in the second half of the year — something I believe is impossible, even if world oil prices were to fall to $60 a barrel.

My own projection assumes an average oil price of $80 a barrel for the remainder of the year. The current price of around $70 is, in my view, temporary. It reflects an oversupply created by approximately 165 million barrels of oil stored on stranded tankers, together with increased exports from Saudi Arabia amid concerns that the Strait of Hormuz could again face disruption. That temporary glut is unlikely to last, and oil prices are likely to return to the levels they should be.

Even if the BoT’s projection proves correct and the current account merely balances this year, Thailand would still lose around 530 billion baht in external financing that was available last year to help fund the fiscal deficit. If my forecast proves correct, the financing shortfall would approach 1.2 trillion baht. For the country’s sake, I hope I am wrong.