Headquartered in San Francisco, Uber Technologies Inc. (UBER) operates in four segments: Mobility; Delivery; Freight; and Advanced Technologies Group (ATG) and Other Technology Programs. UBER and Albertsons Companies, Inc. (ACI) recently announced an extension of their relationship to encompass more than 2,000 of the grocer's banner shops nationwide through Uber Eats, including Albertsons, Safeway, Jewel-Osco, ACME, Tom Thumb, Randalls, and others. Uber Eats will now have roughly 800 more locations due to this expansion.

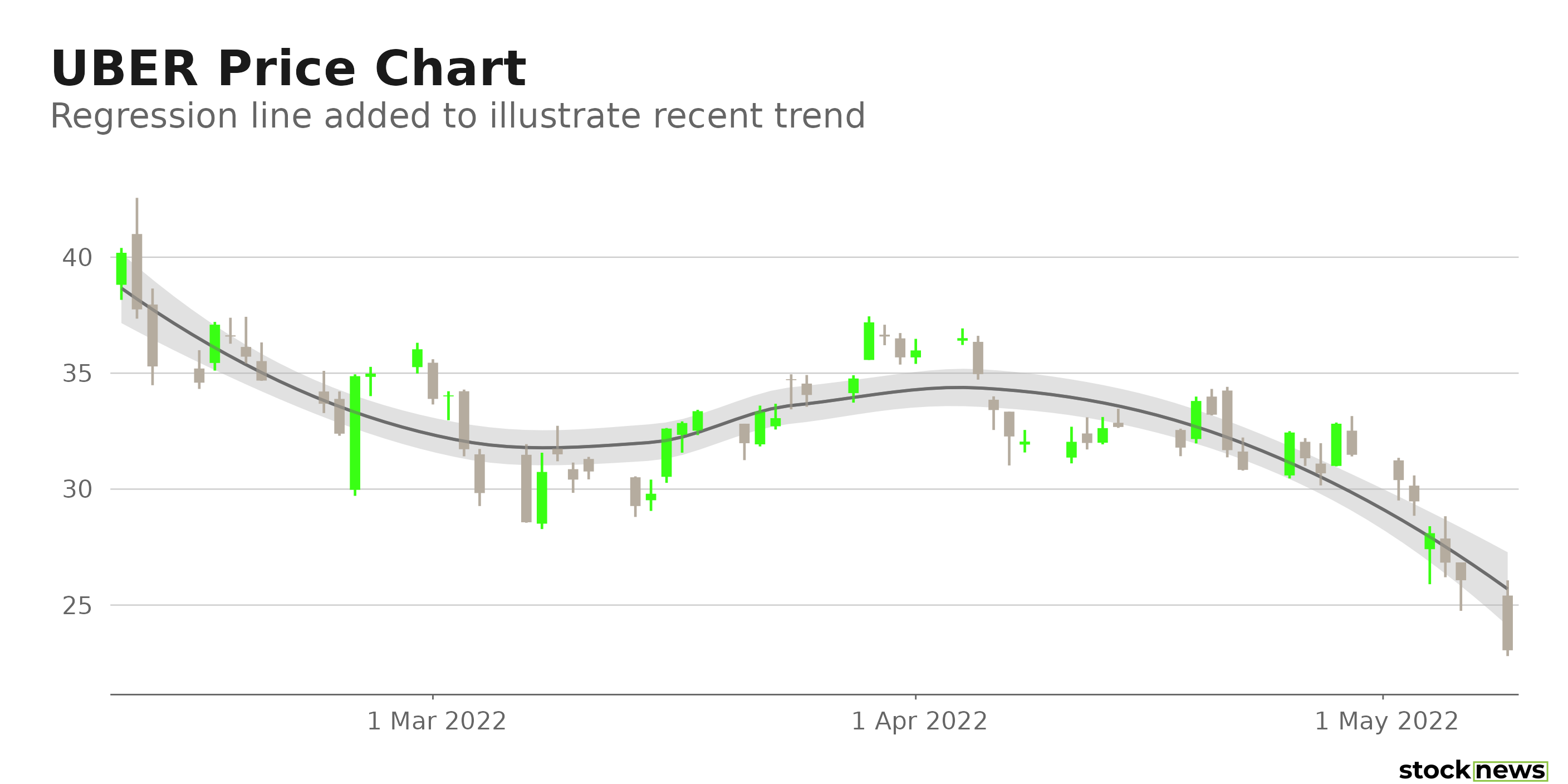

However, the company's shares are down 51% in price over the past year and 28.1% over the past month to close yesterday's trading session at $23.05. In addition, the stock is currently trading 55.9% below its 52-week high of $52.36.

Furthermore, its shares were down on Monday, outpacing the wider Nasdaq market, following news that the ride-hailing company may restrict recruiting and cut its spending on marketing. Rising driver expenses, exacerbated in part by rising gasoline prices and one of the tightest labor markets on record, are eroding the company's earnings.

Here is what could shape UBER's performance in the near term:

Cuts Costs and Slows down Hiring

UBER declined 2% in premarket trading Monday after CNBC reported that the ridesharing and the food-delivery business intends to decrease marketing and incentive spending and freeze recruiting, citing an email sent to employees on Sunday by CEO Dara Khosrowshahi. "It's clear that the market is experiencing a seismic shift, and we must respond accordingly," Khosrowshahi said in an email to CNBC. The firm will now focus on free cash flow as a profitability metric rather than adjusted EBITDA, which is a modification of an already adjusted statistic that is frequently cited as a measure of success by unprofitable enterprises.

Inadequate Financials

UBER's total revenue increased 136.1% year-over-year to $6.85 billion for the three months ended March 31, 2022. Its mobility gross bookings grew 62% from the year-ago value to $10.7 billion. However, its costs and expenses increased 65.7% from their year-ago value to $7.34 billion. Its operating loss came in at $482 million. And the company's net loss increased 5391% year-over-year to $5.93 billion in the prior-year period. Its loss per share came in at $3.04 over this period.

Poor Profitability

UBER's 0.63% trailing-12-months asset turnover ratio is 20.7% lower than the 0.80% industry average. Its $181 million trailing-12-months cash from operations is 1.8% lower than the $184.30 million industry average. Also, its trailing-12-months ROA, net income margin and ROC are negative 19.3%, 29.5%, and 7.7%, respectively.

Premium Valuation

In terms of forward Price/Book, the stock is currently trading at 4.86x, which is 90.2% lower than the 2.56x industry average. Also, its 1.80x forward EV/Sales is 13.5% lower than the 1.59x industry average. Furthermore, UBER's 1.53x forward Price/Sales is 20.8% lower than the 1.26x industry average.

POWR Ratings Reflect Bleak Outlook

UBER has an overall D rating, which equates to Sell in our proprietary POWR Ratings system. The POWR ratings are calculated by considering 118 distinct factors, with each factor weighted to an optimal degree.

Our proprietary rating system also evaluates each stock based on eight distinct categories. UBER has a D grade for Stability and Value. The 1.31 stock beta is consistent with the Stability grade. In addition, UBER's higher than industry valuation is in sync with the Value grade.

Of the 81 stocks in the C-rated Technology – Services industry, UBER is ranked #63.

Beyond what I have stated above, one can view UBER ratings for Growth, Momentum, Quality, and Sentiment here

Bottom Line

While Uber reported a larger-than-expected first-quarter loss of $3.04 per share, most of which was attributed to accounting adjustments related to the group's investments in China-based ride-hailing company Didi Global (DIDI), the business is struggling to keep up with escalating costs. Also, analysts expect its EPS to decline 126% in the current year. Furthermore, considering its premium valuation and poor profitability, we think the stock is best avoided now.

How Does Uber Technologies Inc. (UBER) Stack Up Against its Peers?

While UBER has an overall D rating, one might want to consider its industry peers, PC Connection Inc. (CNXN), Celestica Inc. (CLS), and Information Services Group Inc. (III), which have an overall A (Strong Buy) rating.

UBER shares rose $0.52 (+2.26%) in premarket trading Tuesday. Year-to-date, UBER has declined -45.03%, versus a -15.91% rise in the benchmark S&P 500 index during the same period.

About the Author: Pragya Pandey

Pragya is an equity research analyst and financial journalist with a passion for investing. In college she majored in finance and is currently pursuing the CFA program and is a Level II candidate.

Should You Scoop Up Shares of Uber Under $25? StockNews.com