/Seagate%20Technology%20Holdings%20Plc%20logo%20on%20phone-by%20rafapress%20via%20Shutterstock.jpg)

Seagate Technology (STX) delivered strong financial results for the third quarter of fiscal 2026, triggering a sharp positive market reaction. Shares of STX have surged over 10% in today's trading, reflecting investors’ growing confidence in the durability of demand for its high-capacity data storage solutions, driven by rising capital expenditures for artificial intelligence (AI) infrastructure.

Notably, strong demand and higher pricing driven by industry-wide tight supply have significantly boosted its profitability and share price. STX stock has advanced more than 132% year-to-date (YTD). Moreover, it has rallied around 605% over the past year.

Despite the significant rally, Seagate's stock has three key catalysts that could continue to drive it higher.

Durable Demand to Support Seagate’s Rally

Seagate's stock will likely sustain its rally, driven by structurally strong demand from cloud and enterprise data center customers. As large cloud providers and hyperscalers scale up their AI workloads, the need for cost-effective, energy-efficient storage is expected to remain strong. In this environment, Seagate is well positioned to benefit, thanks to its ability to deliver high-capacity, energy- and capital-efficient storage, even at large scale.

Seagate’s March-quarter results highlight the strength of this durable demand. Its top line was $3.1 billion, reflecting a 10% sequential increase and a 44% year-over-year (YoY) growth. Data center customers accounted for approximately 80% of total revenue.

In the data center segment, revenue climbed 12% sequentially and 55% YoY to $2.5 billion. Cloud customers continue to dominate this segment, contributing the majority of both revenue and capacity shipments.

Seagate’s strong profitability further strengthens its investment case. Adjusted gross profit increased to $1.5 billion, rising 23% quarter-over-quarter and 87% YoY. Gross margins expanded to 47%, up from 42.2% in the previous quarter, reflecting strong pricing and a favorable shift toward higher-capacity, higher-value products.

Looking ahead, strong demand, higher pricing, and Seagate’s build-to-order (BTO) manufacturing model are likely to drive its revenue and earnings, supporting its share price. Further, its Heat-Assisted Magnetic Recording (HAMR)-based Mozaic platform is gaining traction, supporting its future growth.

Overall, durable demand, an improving product mix, build-to-order contracts, a proven product portfolio, and innovation position Seagate to deliver solid growth, supporting its share price rally.

Seagate Strengthens Its Balance Sheet

Seagate is strengthening its balance sheet, which enhances its financial flexibility and supports its longer-term growth. During the March quarter, it repaid $641 million in debt using cash on hand. Following the repayment, Seagate’s gross debt declined to approximately $3.9 billion.

This effort is part of a broader deleveraging strategy. Since the start of fiscal 2026, Seagate has reduced its gross debt by roughly $1.1 billion, signaling a commitment to strengthen its balance sheet. The impact of these actions is evident in the company’s leverage metrics. Net leverage improved to 0.7x, supported by adjusted EBITDA of $1.2 billion in the March quarter.

Looking ahead, Seagate appears well-positioned to further reduce leverage. Continued gains in profitability and cash generation should allow the company to sustain its debt reduction trajectory. This combination of strengthening earnings and declining leverage creates the capacity to enhance shareholder value and invest in growth initiatives.

Seagate’s Valuation Supports Further Upside

STX stock has appreciated significantly. However, it still looks compelling near the current price levels. The company will continue to benefit from durable demand for mass data storage, driven by increased investment in AI infrastructure.

From a valuation perspective, the stock remains reasonably priced relative to its earnings growth outlook. Seagate is currently trading at a forward price-earnings multiple of 48.3, which is compelling considering its growth prospects. Analysts project STX’s earnings per share (EPS) to jump by 68.9% in fiscal 2026 and rise another 56.5% in 2027, suggesting further upside potential in its stock.

Conclusion

Seagate's stock is likely to sustain its upward trajectory, driven by strong demand, a solid product portfolio, improved pricing, and a strong balance sheet. Moreover, its valuation still looks attractive, supporting the ongoing rally in its shares.

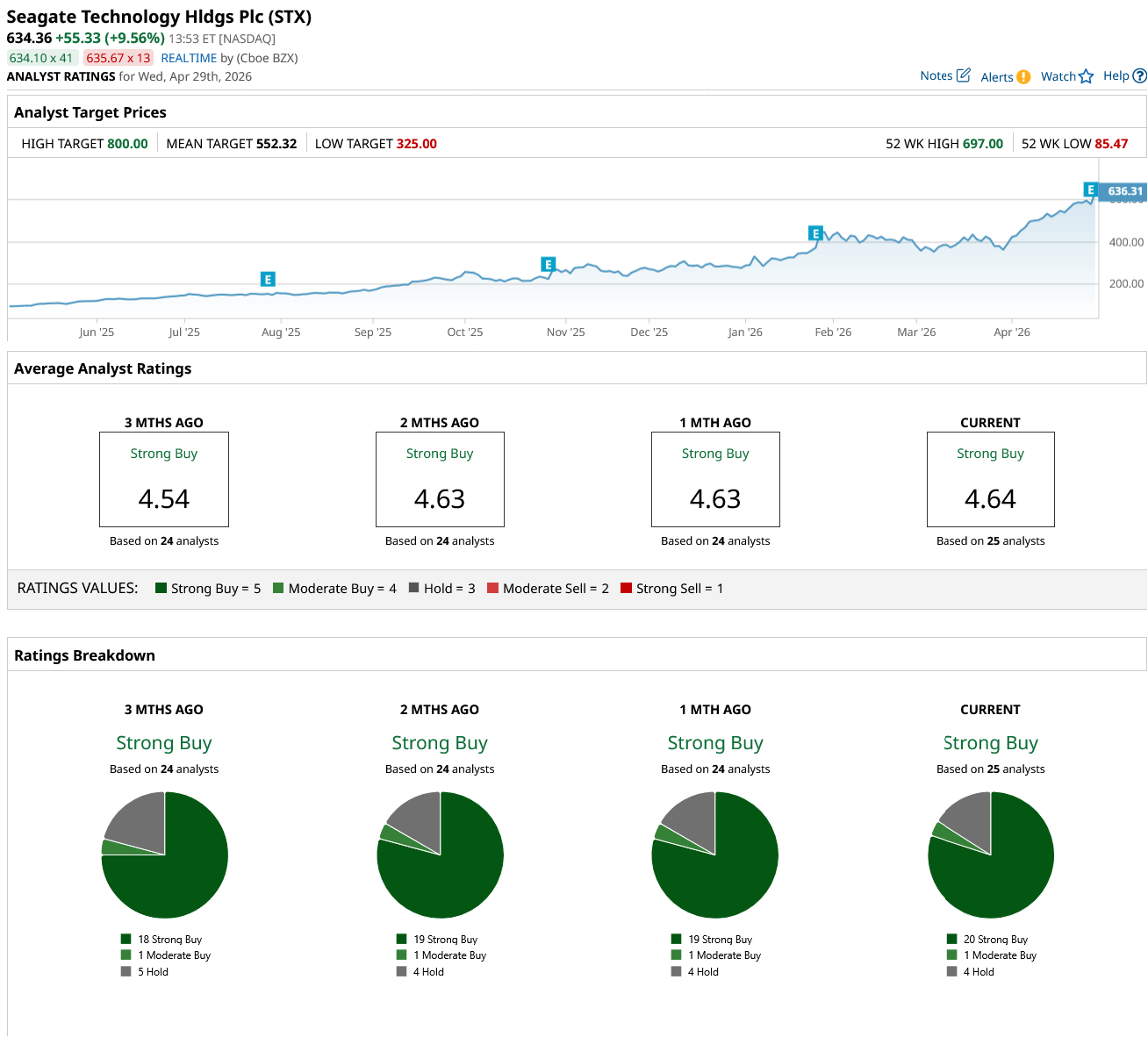

Analysts are bullish and maintain a consensus “Strong Buy” rating on STX stock.