In 2025, the market has been less than welcoming to DocuSign (DOCU) stock.

Despite an upbeat second quarter in its fiscal 2026, the stock has fallen 10.7% year to date, lagging the overall market. However, its second-quarter earnings painted a picture of a company accelerating toward a new phase of long-term growth as it aggressively integrates artificial intelligence (AI) across the whole agreement lifecycle.

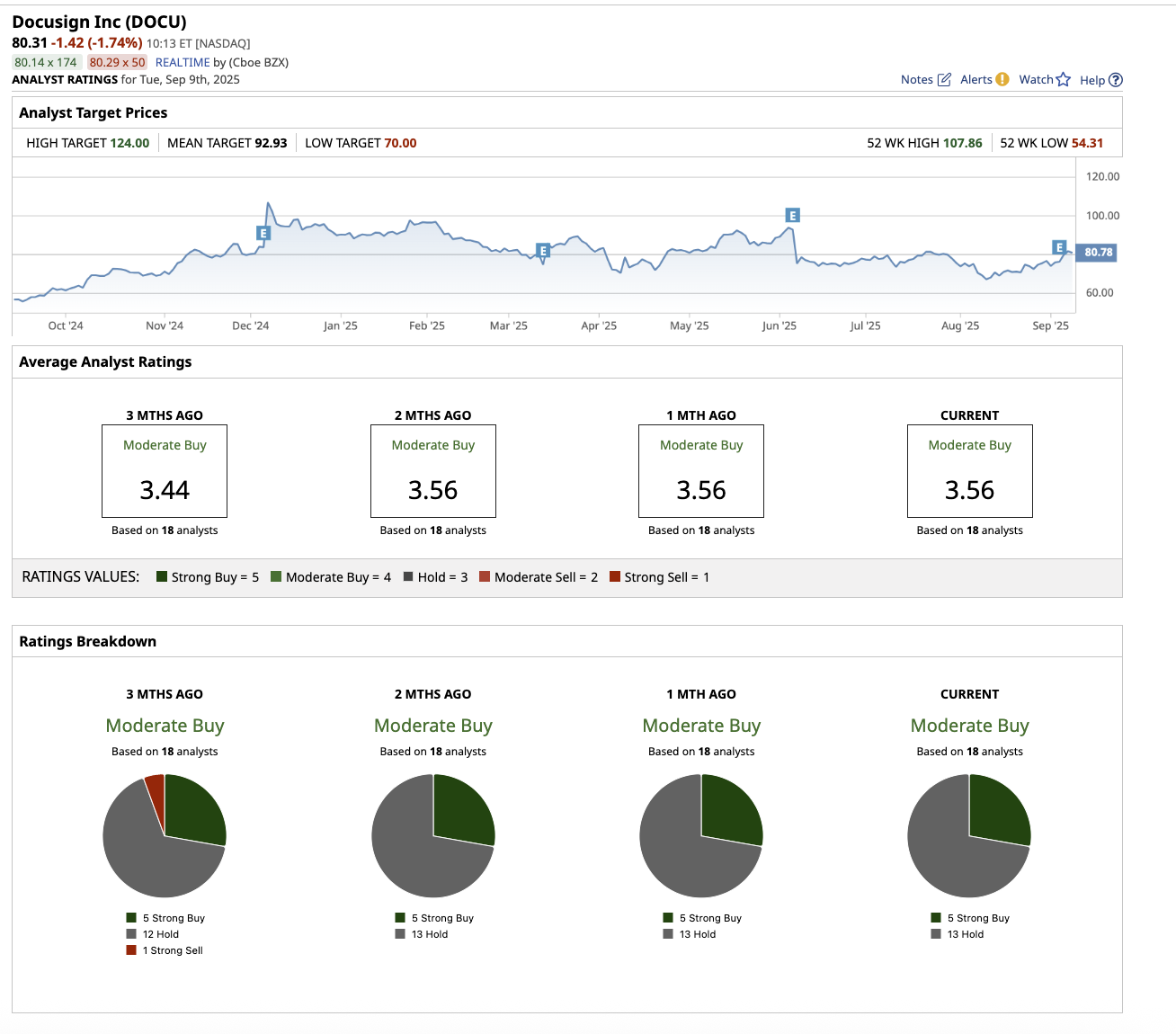

This is likely why Wall Street analysts predict the stock can recover and soar by 50% to achieve its high target price of $125. However, as a small player in the software market, is DOCU worth the risk?

About DocuSign

Valued at $16.5 billion, DocuSign is a software company that allows businesses and people to sign, send, and manage contracts online. Its eSignature and agreement management solutions replace paper processes, making transactions faster, more secure, and legally enforceable. It serves clients in a variety of industries, including real estate, banking, healthcare, law, government, and technology, who require contracts completed promptly and securely. DocuSign is redefining its business model around AI-powered agreement management. In the second quarter, revenue climbed 9% year over year to $801 million, led by a 13% increase in billings, making it one of the greatest growth quarters in the last two years.

During the earnings call, CFO Blake Grayson stated that direct customer demand, improved gross retention, early renewals, and the transition to yearly billing contracts drove the growth. Dollar net retention grew to 102%, indicating improved gross retention and increased utilization. DocuSign’s entire customer base increased 9% year over year, topping 1.7 million.

The highlight of the quarter was the increasing use of DocuSign Intelligent Agreement Management (IAM), an AI-native platform that extends beyond e-signature and contract lifecycle management (CLM). Enterprise adoption is beginning to pick up, with more than half of enterprise reps closing at least one IAM deal in Q2. DocuSign expects IAM customers to account for a low double-digit proportion of its book by the end of the year.

DocuSign plans to implement AI agents within IAM, which promises to uncover even more use cases and extend the company's addressable market. Beyond IAM, DocuSign’s Contract Lifecycle Management (CLM) division also stood out, with double-digit year-over-year growth in Q2, one of the company’s best quarters in recent history.

Unlike many software companies in aggressive transformation phases, DocuSign is profitable. However, adjusted earnings fell 5.1% to $0.92 per share for the quarter. DocuSign is promoting itself not only as an e-signature vendor, but also as the category leader in AI-powered agreement management. Financially, the company also remains in a good position with $1.1 billion in cash and no debt. The company also generated $218 million as free cash flow and repurchased $200 million worth of stock.

For the full year fiscal 2026, management expects around a 7% increase in revenue driven by an 8% increase in subscription revenue and 7% growth in billings. Analysts’ estimates for fiscal 2026 align with the company’s predictions. Analysts also predict a 3.07% increase in earnings in fiscal 2026, followed by 9.5% growth in fiscal 2027. Currently priced at 20 times forward 2027 earnings, DocuSign is overvalued for a stock with low-single-digit estimated earnings growth.

What Does Wall Street Say About DOCU Stock?

Overall, Wall Street rates DOCU stock as a Moderate Buy.” Out of the 18 analysts covering the stock, five rate it a “Strong Buy,” and 13 rate it a “Hold.” Based on its average target price of $92.93, the stock has upside potential of 15.6% from current levels. Plus, its high price estimate of $124 suggests the stock could rally as much as 55% over the next 12 months.

Is DOCU a Buy Now?

If DocuSign can accelerate revenue growth considerably beyond the current 7% target and show re-accelerating billings and large-account expansion, the stock has a better chance of hitting $124.

That said, DocuSign remains a risky stock as electronic signature and agreement management is a small sector with limited growth potential. The company faces huge competition in the software space from bigger players such as Adobe (ADBE), Salesforce (CRM), and Microsoft (MSFT). Therefore, I believe that if you are seeking a great growth stock for the long term, DOCU may not be worth the risk.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.