Negative yields mean Japan’s government gets paid to borrow -- but it’s not profiting. In fact, yields below zero probably cost the treasury $3.4 billion last year.

That’s because historically low yields and high bond prices mean the Bank of Japan cut its dividend to the government, even though it had a higher income. That more than offset the extra money the Finance Ministry got each time it auctioned debt.

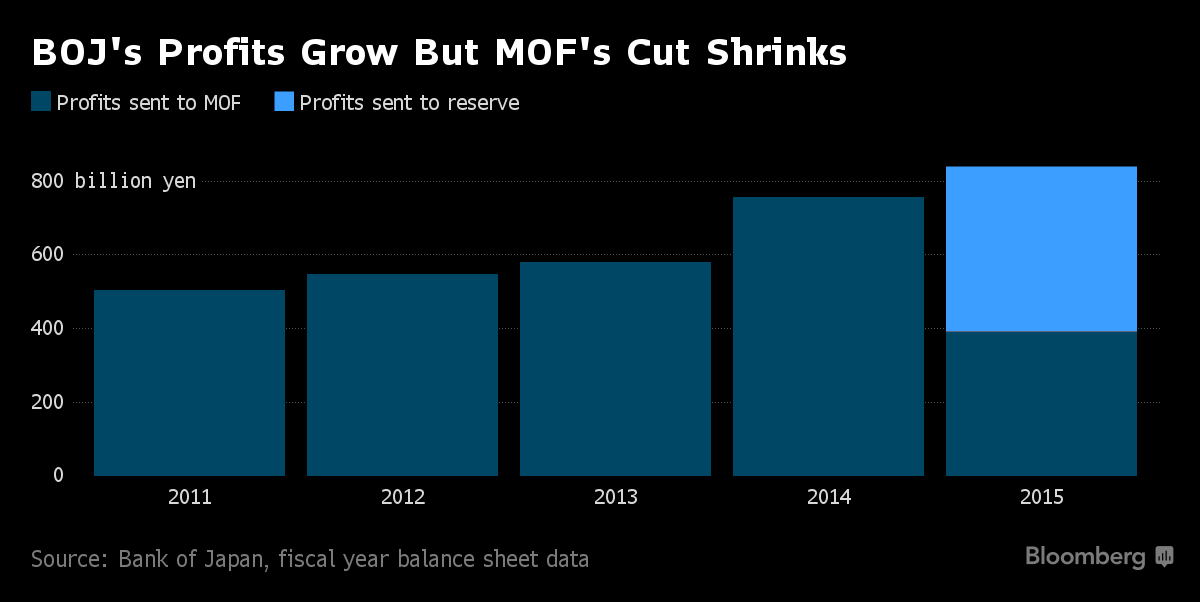

Japan’s Ministry of Finance made about 110 billion yen ($1.1 billion) more in the year to April than it would have if yields had been zero, according to Bloomberg calculations. However, the BOJ cut 450 billion yen from its dividend to the government so it could increase its reserve to cover potential losses on bond holdings.

This money-go-round shows how intertwined the finances of the BOJ and the government are, with this decline in revenue one of the side effects of the central bank’s massive stimulus. The BOJ’s record bond purchases mean it gets higher income now, but some warn its provisions for potential losses will barely be a drop in the bucket when it eventually decides to exit the current measures.

“You can’t say the Finance Ministry is making a big profit, if you consider it in conjunction with what the BOJ will suffer,” said Makoto Suzuki, a senior bond strategist at Okasan Securities Group Inc. in Tokyo. “The BOJ will hold the bonds to maturity, so will have to write off those losses.”

How does the money-go-round work?

1. The BOJ buys debt from the market. Its purchases have pushed prices up and yields down, forcing it to buy debt at prices higher than the face value. That gives extra money to the MOF.

2. The Finance Ministry then pays interest income to the BOJ for the bonds it now holds. Even with the coupon on 10-year notes currently at 0.1 percent, the central bank owns almost 327 trillion yen in sovereign debt, so it gets a lot of income: 1.29 trillion yen last financial year.

3. The BOJ then uses some of its income to pay for the amortization losses on the bonds it owns. Such writedowns rose to 874 billion yen last fiscal year. The central bank buys debt for more than the face amount, and has to write it down so that the book value eventually equals the principal.

For the most recent 10-year note, the MOF initially auctioned it for 101.96 yen and the BOJ probably paid more than that. It will now have to take a 2 yen or more loss on each of the bonds in that series it owns, so that when it matures in 2026, the price on its balance sheet will be back at 100 yen. The benchmark bond price was 101.779 yen, with a yield of minus 0.08 percent as of 10:56 a.m. in Tokyo on Thursday, according to Japan Bond Trading Co.

4. The central bank then returns much of its leftover profits to the MOF. Last year, that dividend was cut so that it could add 450 billion yen into its reserve to pay for bond losses.

For more on the BOJ’s bond holdings, click here.

This trend looks likely to continue. The BOJ has to buy 120 trillion yen of JGBs this year to achieve its goal of expanding its holdings of bonds by 80 trillion yen because it needs to replace maturing debt. And with prices high and coupons low, more and more of the debt on its books will have a negligible income and a price that needs to be written down.

So even though interest income may continue rising, profits and the money returned to MOF may fall in 2016 and beyond, as happened in 2015. Whether the profits are put into the reserves, or eaten away by amortization, there may not be much extra money after the end of this fiscal year to give back to the treasury.

Overall, this circulation of money between the balance sheets of MOF and the BOJ comes out at about even, according to Naomi Muguruma, a senior market economist at Mitsubishi UFJ Morgan Stanley Securities Co. in Tokyo, who warns that the BOJ could be facing big losses when it seeks to exits these policies.

“The BOJ will probably avoid selling its bond holdings when it exits stimulus and instead will probably try to maintain its balance sheet by raising the deposit rate,” Muguruma said. The simulation that they won’t have enough reserves is reasonable, she said.

(Updates with bond price in ninth paragraph.)

--With assistance from Jason Clenfield To contact the reporters on this story: James Mayger in Tokyo at jmayger@bloomberg.net, Shigeki Nozawa in Tokyo at snozawa1@bloomberg.net, Kevin Buckland in Tokyo at kbuckland1@bloomberg.net. To contact the editors responsible for this story: Brett Miller at bmiller30@bloomberg.net, Garfield Reynolds at greynolds1@bloomberg.net, Sandy Hendry at shendry@bloomberg.net, Tomoko Yamazaki, Ken McCallum

©2016 Bloomberg L.P.