Valued at a market cap of $21.9 billion, Williams-Sonoma, Inc. (WSM) is an omni-channel specialty retailer that offers various home products. The San Francisco, California-based company offers a wide array of cookware, furniture, home furnishings, and decorative accessories.

Companies worth $10 billion or more are typically classified as “large-cap stocks,” and WSM fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the specialty retail industry. The company commands a significant presence in the e-commerce landscape and maintains a strategic network of retail stores across the United States, Canada, Australia, and the United Kingdom, supplemented by franchise agreements in various international markets.

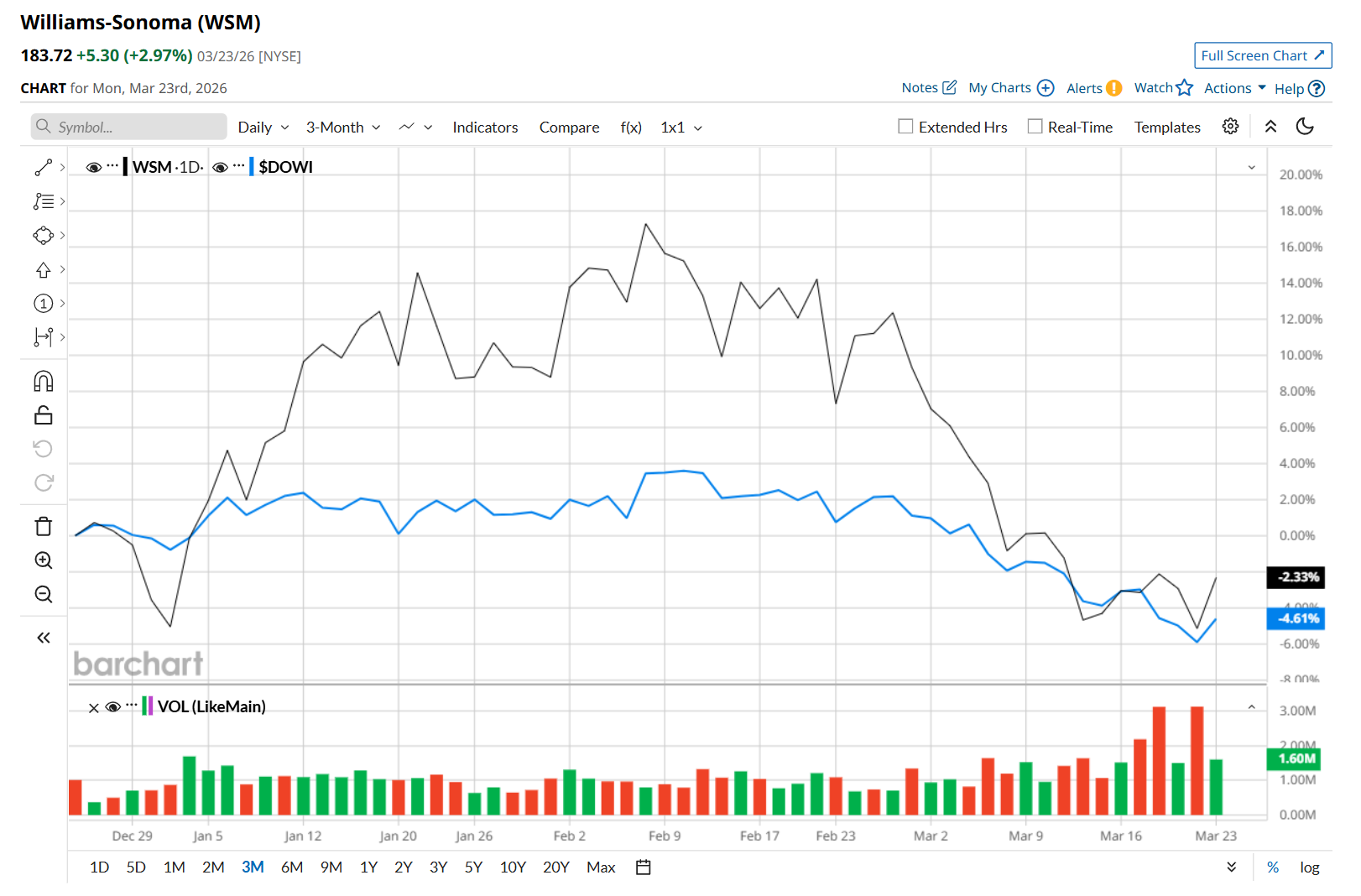

This specialty retailer has dipped 17.2% from its 52-week high of $222, reached on Feb. 20. Shares of WSM have declined 2.3% over the past three months, outperforming the Dow Jones Industrial Average’s ($DOWI) 4.6% drop during the same time frame.

Moreover, on a YTD basis, shares of WSM are up 2.9%, compared to DOWI’s 3.9% loss. In the longer term, WSM has surged 12.3% over the past 52 weeks, outpacing DOWI’s 10.1% uptick over the same time frame.

To confirm its recent bearish trend, WSM has been trading below its 200-day moving average since early March and has remained below its 50-day moving average since late February.

On Mar. 18, shares of WSM surged 1.1% after it reported mixed Q4 results. The company posted earnings per share of $3.04, beating analyst estimates of $2.89, supported by a 3.2% increase in same-store sales and an improved gross margin. However, its total revenue declined 4.3% year-over-year to $2.4 billion, missing Wall Street forecasts. Additionally, its operating margin narrowed to 20.3% from 21.5% in the prior-year quarter, reflecting higher operating expenses. Despite the revenue miss, investors seemed encouraged by the stronger-than-expected profitability amid a challenging sales environment.

WSM has considerably outpaced its rival, RH (RH), which declined 49.8% over the past 52 weeks and 27.8% on a YTD basis.

Looking at WSM’s recent outperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 20 analysts covering it, and the mean price target of $210.28 suggests a 14.1% premium to its current price levels.