Mid-America Apartment Communities, Inc. (MAA) is a real estate investment trust (REIT) that focuses on acquiring, developing, and managing apartment properties. Based in Germantown, Tennessee, the company manages a substantial portfolio of residential units across the Southeast, Southwest, and Mid-Atlantic U.S. regions.

With over 100,000 apartment homes under its management, MAA emphasizes operational efficiency and long-term growth, offering quality housing in both urban and suburban areas. The residential REIT currently has a market capitalization of $16.67 billion.

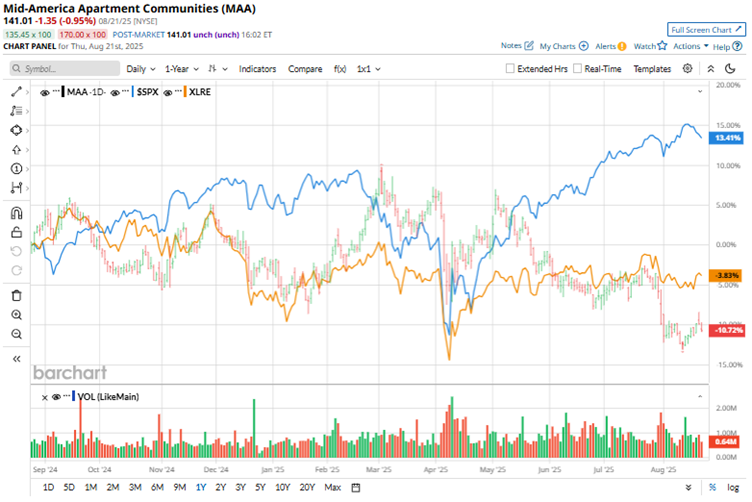

Over the past 52 weeks, MAA’s stock has declined by 7.8%. It had reached a 52-week high of $173.38 in March but is now down by 18.7% from this high. The stock is down by 8.8% year-to-date (YTD). It has broadly underperformed the S&P 500 Index ($SPX), which has gained 13.3% and 8.3% over the same periods, respectively.

Turning our focus to the sector-specific Real Estate Select Sector SPDR Fund (XLRE), we see that the ETF has declined by 1.4% over the past 52 weeks and gained 2.5% YTD, thereby outperforming MAA’s stock.

The company reported its second-quarter results for fiscal 2025 on July 30. And on July 31, MAA’s shares dropped by 4.3% despite reporting better-than-expected bottom-line results. The company’s rental and other property revenues increased marginally year-over-year (YOY) to $549.90 million, which fell short of the Wall Street analysts’ consensus estimate of $552.20 million.

As of the end of the second quarter, resident turnover in the same-store portfolio remained historically low at 41%. The company’s core FFO per share dropped from $2.22 in Q2 2024 to $2.15 in Q2 2025. However, it was higher than the $2.14 per share FFO that Wall Street analysts had expected.

MAA also declared its 126th consecutive quarterly common dividend. The REIT’s current annual dividend rate is $6.06 per common share, which yields 4.26% on the prevailing share price.

For the fiscal year 2025, ending in December 2025, Wall Street analysts expect MAA’s bottom line to decline by a modest 1.5% YOY to $8.75 per share on a diluted basis, but grow by 3.4% to $9.05 per share in fiscal 2026. The REIT has a mixed history of surpassing consensus estimates, topping them in three of the trailing four quarters and missing them on one occasion.

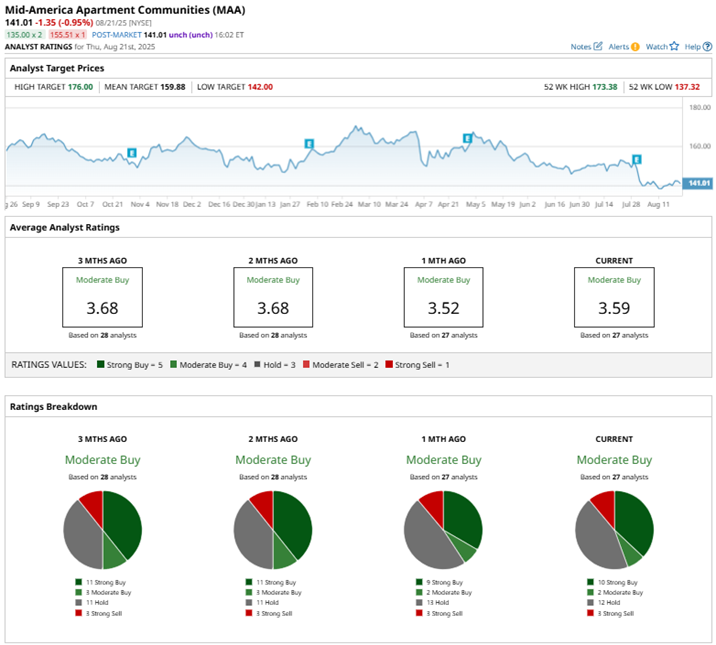

Among the 27 Wall Street analysts covering MAA’s stock, the consensus is a “Moderate Buy.” That’s based on 10 “Strong Buy” ratings, two “Moderate Buy” ratings, 12 “Hold” ratings, and three “Strong Sell” ratings.

The present configuration of the ratings is slightly more bullish than it was a month ago, when the stock had nine “Strong Buy” ratings, rather than 10.

After its Q2 results, MAA received a slew of ratings reaffirmations and price target changes. Analysts at Scotiabank maintain their “Sector Outperform” on MAA, while lowering the price target from $180 to $170. Analysts at Mizuho upgraded the stock from “Neutral” to “Outperform,” while lowering the price target from $161 to $150.

MAA’s mean price target of $159.88 indicates a 13.4% upside over current market prices. The Street-high price target of $176 implies a potential upside of 24.8%.