/Fifth%20Third%20Bancorp%20ban%20location%20by-Joe%20Hendrickson%20via%20iStock.jpg)

With a market cap of $48.4 billion, Fifth Third Bancorp (FITB) provides a broad range of financial products and services through its principal subsidiary, Fifth Third Bank, National Association. The company operates across three segments: Commercial Banking; Consumer and Small Business Banking; and Wealth and Asset Management, serving individuals, businesses, government entities, and institutional clients.

Companies valued at more than $10 billion are generally considered “large-cap” stocks, and Fifth Third Bancorp fits this criterion perfectly. The company offers services including lending, deposit products, wealth management, investment advisory, mortgage banking, and insurance solutions.

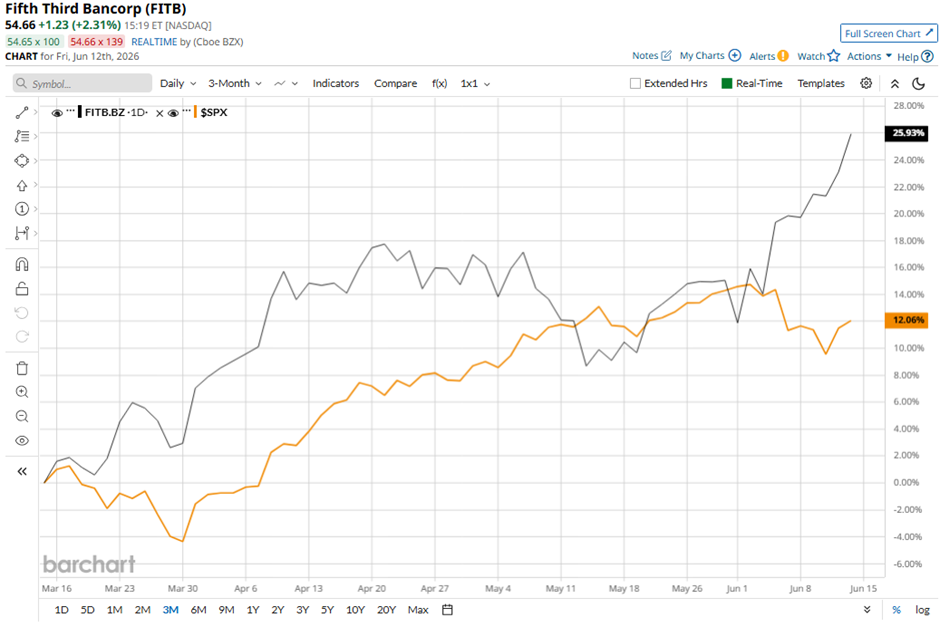

Shares of the Cincinnati, Ohio-based company have decreased 1.5% from its 52-week high of $55.44. Over the past three months, its shares have increased 25.1%, exceeding the broader S&P 500 Index’s ($SPX) 11.3% rise during the same period.

FITB stock is up 16.5% on a YTD basis, outperforming SPX's 8.5% gain. Longer term, shares of the company have returned 39.9% over the past 52 weeks, compared to the 22.9% return of the SPX over the same time frame.

The stock has been trading above its 200-day moving average since last year.

Shares of Fifth Third Bancorp rose 1.7% on Apr. 17 after the bank reported a strong Q1 2026 performance, with adjusted net income increasing to $731 million, supported by a 34% rise in net interest income to $1.93 billion. Investors were also encouraged by a 27-basis-point expansion in net interest margin and significant loan growth, as average portfolio loans and leases climbed to $157.63 billion from $121.27 billion a year ago.

Additionally, optimism surrounding the bank’s February acquisition of Comerica Incorporated and a 49% jump in capital markets fees to $134 million further boosted confidence.

In comparison, FITB stock has outperformed its rival, The PNC Financial Services Group, Inc. (PNC). PNC stock has gained 14% on a YTD basis and 33.9% over the past 52 weeks.

Due to FITB’s outperformance over the past year, analysts remain bullish about its prospects. The stock has a consensus rating of “Strong Buy” from 22 analysts in coverage, and the mean price target of $57.40 is a premium of 5% to current levels.