Memory chips and storage stocks have been on a wild ride lately, driven by the memory-demand boom. However, this rally has been cooled off lately when Google’s unveiling of its new “TurboQuant” AI memory compression sent DRAM and NAND stock prices tumbling. Even Seagate (STX), a hard-drive maker, pulled back as investors worried about memory demand. But JPMorgan tells investors to look past this noise. The firm just kicked off coverage of Seagate with an Overweight rating and a $525 price target, arguing that hyperscale data center spending and pricing tailwinds should drive strong growth.

In other words, JPMorgan sees the recent pullback as a buying opportunity rather than a red flag.

New High-Capacity Drives Target AI Boom

Seagate is a leading global provider of data storage solutions. The company designs and manufactures hard disk drives, solid-state drives, and storage systems for data centers, cloud providers, and enterprises worldwide. Its high-capacity drives power the backbone of the digital economy, enabling massive AI, cloud and video workloads.

Seagate has been busy rolling out new products and tech. In January 2026, it began shipping its first 32TB hard drives for Exos, SkyHawk AI, and IronWolf Pro lines. These enormous drives target AI video-analytics and hyperscale cloud storage. SVP Melyssa Banda emphasized that AI-driven video is exploding and “demands a new kind of data backbone, mass-capacity storage at the edge and in the data center.”

Also, the company continues ramping its next-gen HAMR Mozaic drives. Management said initial production of HAMR-based Mozaic 4+ will start in Q3, and nearline HDD capacity is already fully committed through 2026. These moves show Seagate is positioning itself to satisfy the flood of data from AI and cloud workloads.

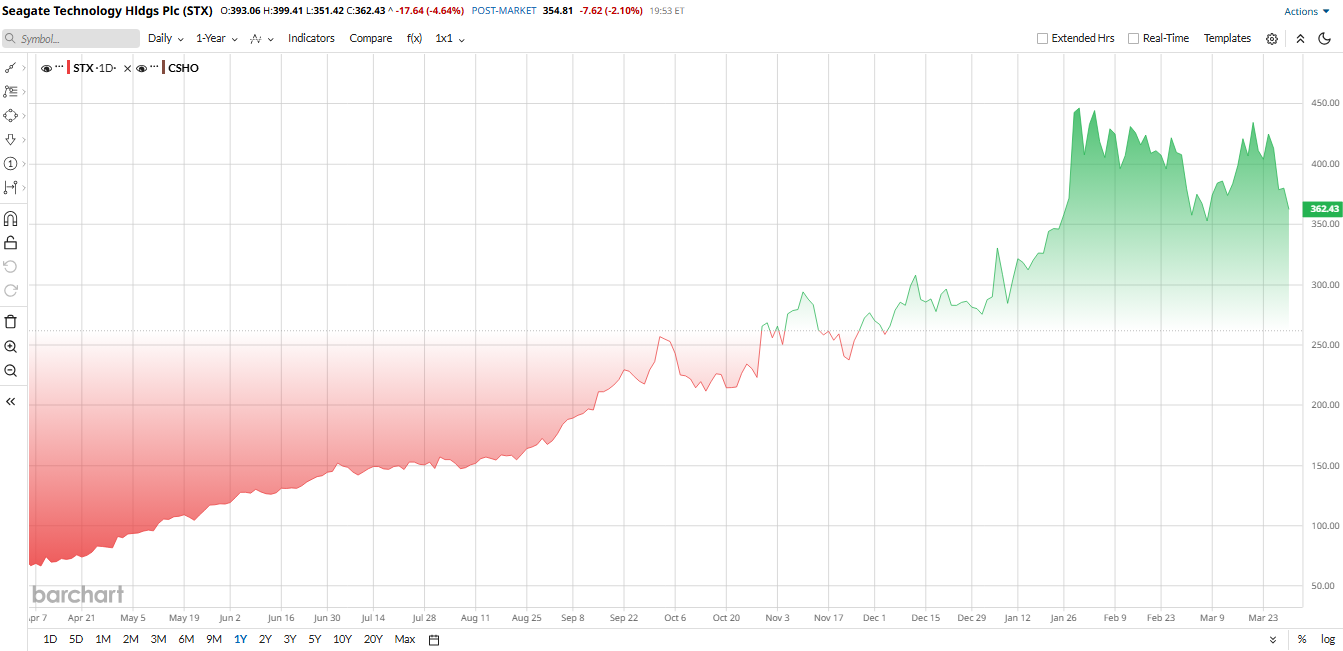

That strength has powered a huge rally in the stock. So far in 2026, Seagate shares are up about 42.26%, and over the past year, they have surged roughly 361% as AI and data-center demand accelerated. But after that run, the valuation has become very stretched. Seagate now trades at 40.35 times earnings and roughly 30.47 times EV/EBITDA, well above sector medians of around 28.79 times and 12.33 times, respectively. That leaves the stock priced for continued strong growth, with less room for disappointment.

TurboQuant Panic Hits Memory Stocks

Last week’s headline was Google’s TurboQuant memory compression. The news rattled memory and chip stocks, including shares of Micron (MU), Sandisk (SNDK), and others, plunged on fears that future AI models would need less raw hardware. Seagate’s stock dipped in the same sell-off. But many analysts say the reaction is overdone. Lynx Equity’s KC Rajkumar noted that TurboQuant merely “relieves bottlenecks without destroying overall demand” and reaffirmed bullish targets on chip names.

In short, it won’t kill the AI-driven data deluge. JPMorgan agrees with that view: it urges investors to ignore the panic and “buy the dip” in Seagate. The bank sees TurboQuant as a short-term blip that won’t derail Seagate’s long-term growth story.

Seagate Delivers Strong Q2 Results

Seagate Technology just proved that the AI boom isn't just about chips. The data storage giant delivered a fiscal second-quarter report that crushed expectations. Revenue climbed 22% year-over-year (YOY) to $2.83 billion. Non-GAAP earnings per share (EPS) came in at $3.11, well above the $2.79 analysts were expecting and far higher than last year's $2.03. The main driver was the Red-hot demand from AI and cloud customers. Data center nearline sales surged 28% to $2.20 billion, representing 79% of total revenue. Seagate shipped 190 exabytes of drives during the quarter.

Additionally, profitability improved dramatically. Non-GAAP gross margin expanded to about 42.2%, up 670 basis points YOY on better pricing and product mix. Plus, net income nearly doubled to $593 million.

Free cash flow came in at a robust $607 million, highlighting the company's healthy cash generation. Seagate also declared its regular quarterly dividend of $0.74 per share.

CEO Dave Mosley said the results "exceeded our expectations on both the top and bottom line" thanks to strong execution and data center demand.

Looking ahead, Seagate guided for fiscal Q3 revenue of about $2.9 billion and non-GAAP EPS of roughly $3.40, both above previous Street estimates. Analysts now model fiscal 2026 EPS of $11.82, representing roughly 62.8% growth.

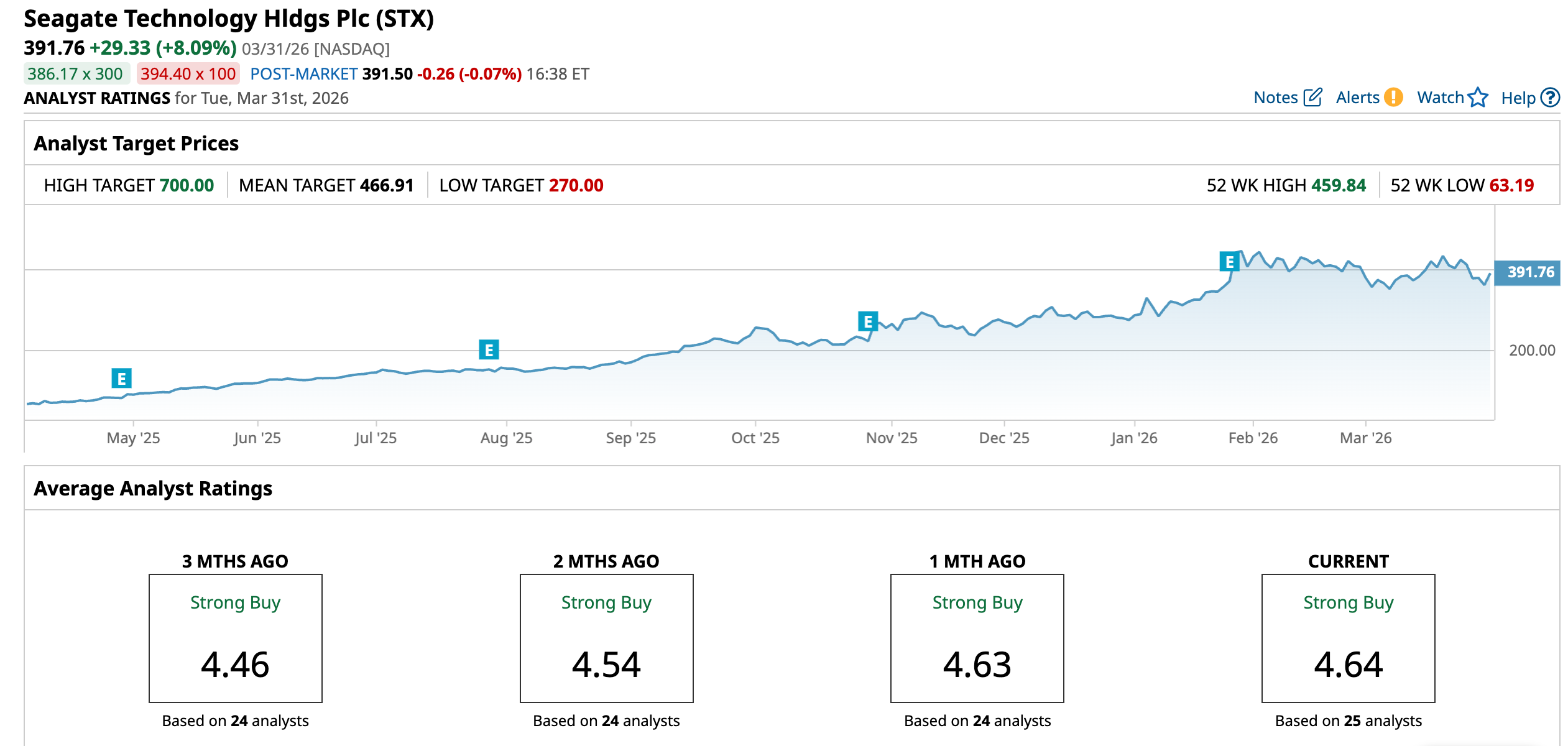

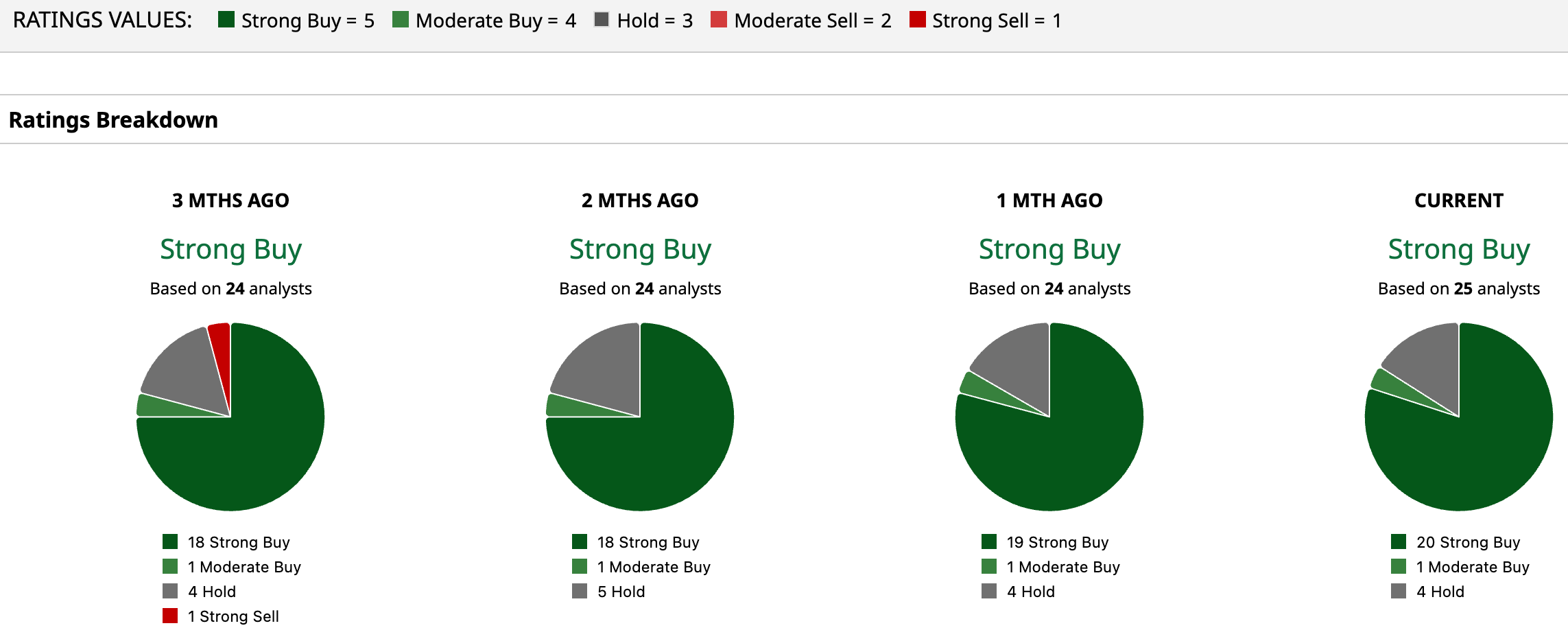

What Do Analysts Think of Seagate Stock?

Wall Street remains highly bullish on Seagate stock. The consensus rating is “Strong Buy,” with the average 12-month price target around $447, roughly 70% above today's level.

Moreover, in recent weeks, several firms have raised their outlook. JPMorgan kicked off coverage at Overweight with $525 PT. Citigroup reiterated a Buy and bumped its target to $480, noting that enterprise customers are “expanding data center capacity to accommodate growing AI workloads”.

Morgan Stanley kept an Overweight stance with a PT of $372, and pointed out that “cloud storage demand trends remain very strong, with upside optionality to pricing and margins.”

Also, Bank of America raised its target to $400, expecting Q2 results to exceed consensus. In short, most analysts see upside. Even the average target assumes gains from here.

As one Putnam note put it, Seagate is well-positioned in an AI/data boom, and JPMorgan agrees, so the stock still looks like a buy despite the recent sell-off.