Yum! Brands (YUM) stock is virtually unchanged despite news that the fast food giant is set to sell its Pizza Hut operations in two transactions worth $2.7 billion. According to the announcement, Pizza Hut operations outside mainland China will be sold to LongRange Capital for about $1.5 billion, while Pizza Hut operations in China will be bought out by Yum China for $1.2 billion.

This deal can be viewed as one of the most important strategic moves of Yum! Brands, and it does not indicate the weakening of the company. On the contrary, the company is looking to simplify its business structure and concentrate efforts on developing its strongest-performing brands. Yum! Brands will generate about $2.3 billion in net proceeds from the deal.

About Yum! Brands Stock

Yum! Brands is one of the leading worldwide fast-food companies with well-known restaurants like Taco Bell, KFC, and Pizza Hut. The company is headquartered in Louisville, Kentucky, and has a market capitalization of about $41.8 billion, operating through a franchise-based model generating highly predictable royalties.

YUM stock has shown decent performance over the past year despite market volatility. Shares trade at roughly $152, which is approximately 11% higher than the 52-week low of $137.33 but still 10% lower than the 52-week high of $169.39. A low beta of 0.57 shows the defensive properties of the stock compared to the market.

The valuation multiples of YUM stock are quite high, however. Yum! Brands trades at 22.5 times and 24.6 times forward and trailing earnings, respectively. However, considering that the company is trading at these ratios due to its asset-light business model, global presence, and high cash-generation capabilities, its price-to-sales ratio of 5.1 times makes sense.

Currently, Yum! Brands pays a quarterly dividend of $0.75 as one of the most shareholder-friendly names in the restaurant sector.

Yum! Brands Beats on Earnings

Yum! Brands reported strong first-quarter 2026 results that exceeded expectations. The firm reported GAAP EPS of $1.55, while adjusted EPS excluding special items stood at $1.50, up 15% year-over-year (YOY).

Overall, the trends in operations remain positive. Worldwide system sales increased 6% YOY excluding foreign exchange impact, while unit count increased 5% with the company opening more than 1,000 restaurants. Core operating profit increased 6%, while GAAP operating profit increased 17%.

Management highlighted solid performance from the company's biggest growth drivers. Taco Bell increased same store sales by 8%, outperforming much of the quick-service restaurant industry. KFC also showed good growth in units and same store sales in numerous international markets.

The Q1 earnings report also confirmed the growing digital capabilities of the company. Digital system sales increased to $11 billion, reaching a record digital mix of 63%. CEO Chris Turner noted that technology and AI investments have helped Yum! maintain momentum in sales and customer engagement, although Pizza Hut is facing a lawsuit from a franchisee over issues with its AI delivery system.

The planned sale of Pizza Hut could help Yum! Brands achieve further growth. Excluding Pizza Hut, the company reported 7% growth in system sales, 6% growth in unit count, and 10% growth in core operating profit. This performance shows that Taco Bell and KFC can be main growth drivers for the company going forward.

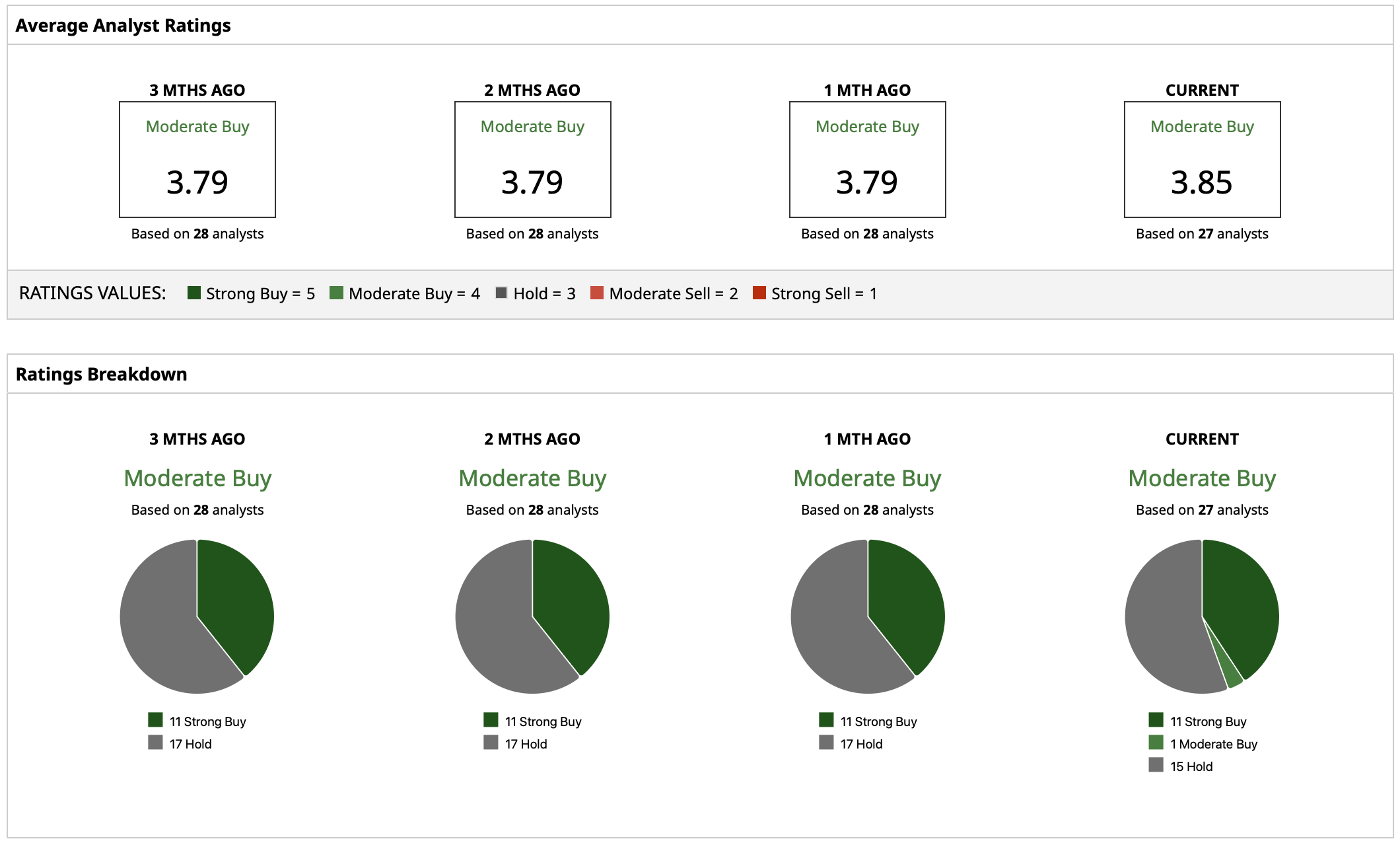

What Do Analysts Expect for Yum! Brands Stock?

Analysts remain positive toward YUM stock despite its rather premium valuation with a consensus “Moderate Buy” rating. The mean target price of $173.61 implies potential upside of approximately 14% from current levels. The Street-high price target for YUM stock stands at $191, while the lowest price target stands at $145.

The divestment of Pizza Hut could become an additional catalyst if management successfully utilizes the proceeds from the transaction. With net proceeds of about $2.3 billion, investors will have to watch how Yum! allocates this money. For now, the deal looks like a continuation of Yum! Brands' long-term strategy to concentrate on growth opportunities and maintain its asset-light business model. Investors can consider YUM stock as a potential defensive growth opportunity.