ECB and Greece 'review the situation'

Hello again: Just to flag up a few newsflashes from Frankfurt tonight, following the talks between Greek deputy PM Dragasakis and ECB president Mario Draghi.

Nothing too spectacular, but at least both sides are talking....

#ECB: Draghi and #Greece DepPM Dragasakis reviewed Greek economy and reviewed ongoing Brussels negotiations ~BBG

— Yannis Koutsomitis (@YanniKouts) May 5, 2015

#Greece Deputy PM @YDragasakis told #ECB President that reaching an agreement is a realistic & visible target (via @MegaGegonota) #ec #imf

— Manos Giakoumis (@ManosGiakoumis) May 5, 2015

European markets end lower

As the Greek talks drag on with little sign of agreement, and next Monday’s eurogroup meeting suddenly not expected to produce much progress, stock markets turned sharply into negative territory. Disappointing US trade figures also added to the uncertain mood as did the forthcoming UK election. The final scores showed:

- The FTSE finished down 58.37 points or 0.84% at 6927.58

- Germany’s Dax dropped 2.51% to 11,327.68

- France’s Cac closed 2.12% lower at 4974.07

- Italy’s FTSE MIB fell 2.76% to 22,576.35

- Spain’s Ibex ended 2.74% lower at 11,115.6

- The Athens market dropped 3.85% to 794.23

In the US, the Dow Jones Industrial Average is currently 53 points or 0.3% lower.

European bond yields moved higher as investors fretted about the situation in Greece.

On that note, it’s time to close up for the evening. Thanks for all your comments, and we’ll be back tomorrow.

Greek gov't 'non paper' on current state of negotiations, kindly translated into English by @GreekAnalyst: https://t.co/vljoZIgS5I #Greece

— Open Europe (@OpenEurope) May 5, 2015

Here’s the start of the document:

- The serious disagreements and contradictions between the IMF and the EU are creating obstacles in the negotiations, as well as high risks. While until recently the main argument of the institutions was that the Greek side did not submit complete proposals, now it is clear that proposals have indeed been submitted and that there have been substantial concessions towards the direction of an “honorable compromise.”

- The difference of strategy, however, between the institutions is creating obstacles.

- The IMF puts its red lines on the reforms, especially on pension and labour reforms, while it has loose lines on the topic of the primary surplus. On the back of the mind of the IMF lies the thought of debt write off, so that this can be rendered sustainable.

- On the contrary, the European Commission has red lines on the topic of the primary surplus, and consequently, on the issue of not cutting the debt, and loose lines on tough reforms, such as those regarding pensions and labour relations.

Greece is considering plans to slow any capital flight, the Times is reporting.

Greek surcharge on cashpoint withdrawals & financial transactions attempts to slow capital flight/raise cash http://t.co/hVmXDMTpPA

— Bruno Waterfield (@BrunoBrussels) May 5, 2015

Here’s Bloomberg’s take on Greece blaming its creditors for the current impasse:

Greece blamed international creditors for the failure to find an agreement in bailout talks, saying a deal won’t be possible until they agree on a common set of demands.

A Greek official said that the European Commission and the International Monetary Fund are confronting the country with too many red lines and aren’t coordinated enough with each other.

The IMF won’t compromise on labor deregulation and pension reforms, while the European Commission is insisting on fiscal targets being met and is refusing to consider a debt write down, said the official, who spoke on condition of anonymity because the talks are confidential.

And here is the European Commission:

.@pierremoscovici met @yanisvaroufakis to take stock of significant progress made by Brussels group, and prep useful Eurogroup on Monday

— Olivier Bailly (@OlivierBaillyEU) May 5, 2015

So many conflicting comments coming out about where Greece and its creditors stand.

French finance minister Michel Sapin said after meeting his Greek counterpart Yanis Varoufakis that “we have the scope to reach a good compromise..There is no other solution than an accord.”

But then we have unnamed Greek officials taking a different tone:

Greece Gov Official - Disagreements between EU and IMF are creating obstacles in negotiations on Greece.

— Steve Collins (@TradeDesk_Steve) May 5, 2015

More on the growing feeling that no deal between Greece and its creditors will be reached next week, this time from the chairman of the eurogroup working group Thomas Wieser, talking to CNBC. Reuters reports:

Greece and its European creditors will not reach a comprehensive agreement by next week, as it was expected, the chairman of the eurogroup working group, Thomas Wieser, told US TV channel CNBC on Tuesday, but expressed confidence that a deal will be reached before a real crisis or bankruptcy occurs.

“We will get a deal,” Wieser was quoted as saying on CNBC’s webpage. “I think all of the polls show in Greece, the Greek population is firmly convinced its future is in euro. It has given a mandate, which is quite clear it seems to me and it seems to the Greek politicians, [to] do whatever it takes to come to a conclusion with the creditors.”

On Monday, members of the Eurogroup had hoped they would be able to signal that an agreement was in sight, but representatives for European finance ministers in Brussels are still battling over fiscal and value-added-tax issues and labor market reforms, Wieser said.

Asked about a possible Greek exit from the Eurozone, Wiesersaid that while this would have been “a real catastrophe” three years ago, today Europe is well insulated, but the outcome would still be negative.

Greek Debt Deal Needed By Beginning Of June, EU's Wieser Says

— Steve Collins (@TradeDesk_Steve) May 5, 2015

Updated

And in contrast to Markit, the Institute for Supply Management is reporting the pace of growth in the services sector rose to a five month high in April.

An increase in business activity offset a fall in exports, pushing the ISM services index to 57.8 from 56.5 in March and above forecasts of a figure of 56.2.

The contradictory evidence and disappointing US trade deficit earlier have combined to send Wall Street lower, with the Dow Jones Industrial Average now down 65 points.

Back with the US, and signs of a slowdown in growth in the service sector.

The Markit purchasing managers index for services came in at 57.4 in April, down from an initial reading of 57.8 and the 59.2 figure for March. There was a dip in new business growth but the employment component frost to a 10 month high of 55 from 54 in March. Markit chief economist Chris Williamson said:

Robust service sector growth adds to evidence that the economy is far from stalling, as indicated by the GDP numbers seen as the start of the year, supporting the [Federal Reserve’s] view of the economy growing at a moderate rate.

The ISM services report is due shortly.

It appears the “crunch” eurogroup meeting on May 11 will be nothing of the sort. No solutions expected, just more talks about progress (or lack of it?)

Varoufakis Sees No Accord On Greece At May 11 Eurogroup

— Steve Collins (@TradeDesk_Steve) May 5, 2015

Greek Finance Minister Varoufakis hopes talks next Monday will be a fruitful, however no accord is likely in his view (@RANsquawk)

— Open Europe (@OpenEurope) May 5, 2015

EC: Greece Deal At May 11 Eurogroup Is Unlikely

— Live Squawk (@livesquawk) May 5, 2015

EC: Debt Sustainability Being Linked With Pension Reforms By IMF -‘IMF Wants To Remain In Greece If Conditions Met’

— Live Squawk (@livesquawk) May 5, 2015

We r definitely going to have a discussion on May11th that will confirm the progress that has been achieved says @yanisvaroufakis

— Eleni Varvitsiotis (@Elbarbie) May 5, 2015

Seems like EU and Greek side converging that on May 11th #eurogroup no solution should be expected just progress report.

— Eleni Varvitsiotis (@Elbarbie) May 5, 2015

Updated

Summary: EC piles more pressure on Athens

Time for a recap.

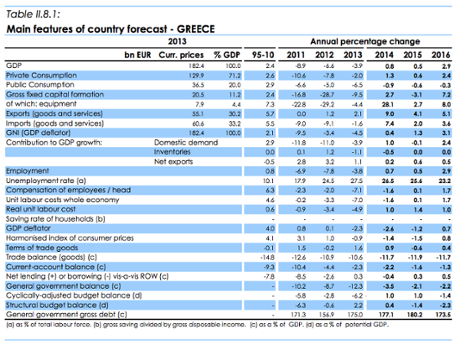

The EC now expects Greek GDP to rise by only 0.5% this year, not the 2.5% it had predicted previously. That would push the country’s debt mountain into even more unsustainable levels, of around 180% of economic output.

Commissioner Pierre Moscovici blamed the “high political uncertainty” in Greece for the downgrade.

As the report puts it:

The rise in uncertainty since the autumn of 2014 and the slowdown in the recovery have had a significant impact on Greece’s public finances, resulting in a significant shortfall in state revenues at the end of 2014 and in the first two months of 2015.

The poor revenue collection around the turn of the year resulted in a significantly weaker-than- expected fiscal outcome for 2014.

#EC slashes 2015 #Greece GDP growth forecast to 0.5%, raises debt/GDP estimate to 180%. http://t.co/CJSmvCL4E3 #economy #ecb #imf

— Manos Giakoumis (@ManosGiakoumis) May 5, 2015

The EC predicts faster growth across the wider eurozone this year; GDP is tipped to rise by 1.5%, up from 1.3% before.

Moscovici says:

“The European economy is enjoying its brightest spring in several years, with the upturn supported by both external factors and policy measures that are beginning to bear fruit.

But more needs to be done to ensure this recovery is more than a seasonal phenomenon.”

Highlights of the press conference start here.

Greece’s debt crisis ratcheted up another notch this morning, after the Financial Times reported that the International Monetary Fund was seriously worried about its bailout programme.

According to the FT, the Fund had warned it could walk away from the Greek bailout unless unless European lenders write off significant amounts of its sovereign debt.

That report helped to drive up yields on Greek bonds, and sent the Athens stock market spiralling down 4.5% in late trading.

Germany’s Wolfgang Schäuble has confirmed that the Fund raised concerns last month, but denied that it was pushing for an immediate write-off.

Athens has speeded up its push for a breakthrough; Yanis Varoufakis is meeting with Moscovici in Brussels this afternoon.....

...., and deputy PM Greek PM Yiannis Dragasakis is sitting down with ECB chief Mario Draghi tonight.

Dragasakis is expected to push for some breathing room from the ECB, which decides tomorrow whether to extend even more emergency liquidity to Greek banks.

Greece is becoming an increasingly painful problem for the ECB, insiders say.

As one senior official put it to Reuters:

“People are fed up...But withdrawing ELA altogether would be a nuclear bomb.”

Greece’s stock market has fallen deeper into the red; the main Athens index is down 4.5% today.

Bank shares are leading the fallers, as traders react to reports that the IMF was pushing for a new debt writedown.

The surge in America’s monthly trade deficit means that the US economy “undoubtedly contracted slightly in the first quarter of 2015”, says Paul Ashworth, Chief US Economist at Capital Economics.

But he expects growth to bounce back in the second three months of this year, meaning America would avoid falling into a technical recession.

Updated

US trade deficit soars to highest since 2008

Just in.... America’s trade deficit has widened unexpectedly to its largest since the financial crisis began, suggesting that its economy could actually be contracting.

The US commerce department says that the US trade deficit surged to a jaw-dropping $51.4bn in March, up from $35.9bn in February.

That’s the largest one-month gap between imports and exports since October 2008, after the collapse of Lehman Brothers.

There is a one-off factor to consider; some West Coast US ports has been disrupted by strike action in February, so imports were playing catch-up last month.

But even allowing for that, the figures suggest the US economy may actually have contracted in the first three months of 2015, rather than scraping annualised growth of 0.2%.

Looks like another downward revision to US Q1 GDP...$DXY

— Michael Hewson (@mhewson_CMC) May 5, 2015

GDP for Q1 now looking at a -0.5 number ? https://t.co/w1PzU2DFzJ

— fred walton (@fredwalton216) May 5, 2015

Surge in imports likely to result in Q1 GDP being revised below zero...looking a lot like last year (minus the mid-year surge).

— Carl Riccadonna (@Riccanomix) May 5, 2015

Updated

Remember the oil price crash of autumn 2014? Well, it’s a different story today - US crude oil just hit the $60/barrel mark for the first time this year.

WTI CRUDE RISES TO $60 A BARREL FOR FIRST TIME SINCE DEC. 11

— Steve Collins (@TradeDesk_Steve) May 5, 2015

That’s quite a recovery since mid-March, when US crude briefly nudged $42 per barrel.

Still, $100 per barrel is still a long way off:

We’ve not heard much from Greece’s finance minister today.... but Yanis Varoufakis has just arrived in Brussels, for talks with Pierre Moscovici.

Cue the usual scrum to catch a glimpse of Varoufakis; despite the recent reshuffle of Greece’s negotiating team, he retains his magnetic attraction to the media.

And the #Greek fin min @yanisvaroufakis is in the house. Media frenzy the least I can say pic.twitter.com/W47AzKtRfh

— Eleni Varvitsiotis (@Elbarbie) May 5, 2015

Schäuble: IMF didn't demand Greek debt relief

Germany’s finance chief, Wolfgang Schäuble, has denied that the International Monetary Fund pushed the eurozone to cut Greece’s debt burden last month.

Schäuble told the Foreign Press Association in Berlin that IMF European chief Poul Thomsen had indeed warned that Greece’s debt reduction path had become ‘more challenging’.

However, Thomsen didn’t insist on debt relief at last month’s Eurogroup meeting in Riga, he added.

Reuters has the details:

“The IMF of course did not make such a comment,” Schäuble said, noting however that Thomsen had been clear that Greek finances were deteriorating because of a pause in reforms linked to the election there.

Thomsen did say things “had become more difficult,” Schäuble said.

If you’re just tuning in, this is in response to the FT’s front page story this morning that the IMF is taking a tough line on Greece, due to its deteriorating finances.

And that story stated clearly that Thomsen did push the debt relief issue.

With the large surplus now turning into a sizeable deficit, Greece’s debt levels would begin to spike again. This would force either Athens to take drastic austerity measures or eurozone bailout lenders to agree to debt write-offs to get Athens’ debt back on a sustainable path, the IMF believes. Officials said Mr Thomsen specifically mentioned the need for debt relief during the three-hour meeting.

“The IMF thinks the gap between the two realities is very large right now,” said one senior official involved in the talks. He noted that both Athens, which was resisting new economic reforms, and eurozone creditors would probably fight the IMF on the issue.

Wolfgang still reading his script https://t.co/0pCD4KmMHU

— Yiannis Mouzakis (@YiannisMouzakis) May 5, 2015

Updated

Don’t take the risk of a Greek exit lightly.

That’s the warning from Italy’s foreign minister Paolo Gentiloni this morning. He told reporters in Milan that:

“Italy’s government considers short-sighted and dangerous to underestimate the Greek crisis.”

Another interesting development. A senior Greek privatisation official has told Reuters that Athens is eager to crack on with two deals, seemingly in a bid to placate its lenders.

That includes reopening bidding for a majority stake in Piraeus Port, and agreeing a €1.2bn deal with German operator Fraport to run regional airports in Greece.

Chinese shipping giant Cosco had been in line to buy Piraeus Port, which it already partly controls, before the Syriza government suspended the privatisation after taking office.

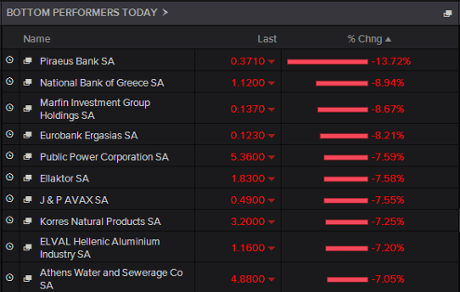

Greek stock market drops 3%

Over in Athens, the stock market has fallen by 3% today.

Bank shares are leading the fallers, with Piraeus Bank sliding by 9.5%.

Investors are understandably concerned by reports that the IMF might walk away from the Greek bailout. The EC’s new growth forecasts are adding to the gloom.

Most other European markets are up, though. The FTSE 100 and the German DAX have both gained 0.5%.

Updated

The Greek government has revealed that prime minister Alexis Tsipras and German chancellor Angela Merkel held a telephone call last night:

As #Greece seeks solution in bailout negotiations, PM #Tsipras spoke with #German Chancellor #Merkel by phone last night, his office says.

— Elena Becatoros (@ElenaBec) May 5, 2015

No detail on what was said. The two leaders had agreed to stay in touch during the bailout talks.

And that’s the end of the press conference. Brussels reporters have scrambled for country-specific briefings, so I suspect we’ll hear more shortly....

Could Greece be given some new liquidity assistance at the next eurogroup meeting, on May 11?

Moscovici replies that he hopes to see significant progress by the time eurozone finance ministers meet on May 11, but doesn’t go any further.

Last night, EC president Jean-Claude Juncker warned that “Anglo-Saxons will try to break up the eurozone” if Greece were to exit the single currency.

Bruno Waterfield of The Times asks Pierre Moscovici what Juncker meant, exactly.....

Moscovici says he didn’t catch his boss’s speech (why not?!) but completely agrees with Juncker on this issue (good recovery).

The single currency is irreversible, and if one member quit then people would begin to speculate about who was next. That’s why Grexit isn’t even being considered, he explains.

Eurozone a single currency, decision to join irreversible. If one country leaves then you have the question who's next,@pierremoscovici

— Bruno Waterfield (@BrunoBrussels) May 5, 2015

Updated

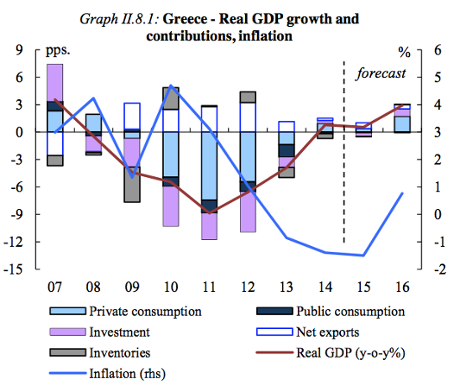

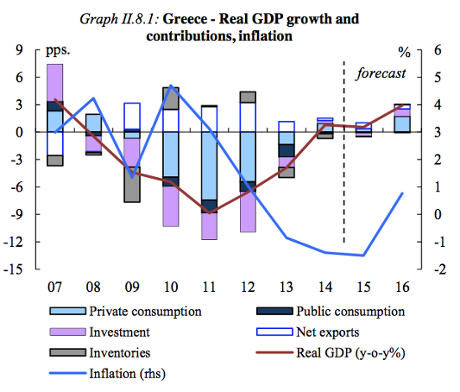

Greece: the key charts

You can read the Commissions’s concerns about Greece on page 80 of the new Spring Forecasts.

This charts show how growth is expected to flag this year, and deflation likely to continue until 2016:

And this table shows all the new forecasts:

(apologies if it’s too small to read; this link may be better)

Today’s forecast also contain bad news for Finland; the EC has slashed its growth forecast this year from 0.8% to just 0.3%.

Finland is also expected to run a deficit above 3% of GDP this year, breaching EU rules. Brussels is planning to give the new Finnish government some advice next week:

Moscovici on #Finland, breaking debt rules: Next week we will provide our country specific recommendations. There will be food for thought.

— Jarno Hartikainen (@JarnoHa) May 5, 2015

Moscovici: Greece suffering from political uncertainty

Finally, the EC allow a question on Greece.

The FT’s Peter Spiegel gets the mike, and whether today’s growth downgrade mean that more needs to be done in the current negotiations to get Greece’s bailout programme back on track.

And does it also mean that any future programme (a third bailout) would have to be larger than expected in February?

Commissioner Moscovici give a long answer (in French, merci Pierre....). The gist is that uncertainty in Greece has hit growth prospects this year. Growth could recover in 2016, if suitable reforms are agreed.

Europe and Athens both want Greece to remain in the eurozone, and neither side wants to see any “accidents”, he adds.

#Moscovici giving long answer on #Greece but not really saying too much

— Open Europe (@OpenEurope) May 5, 2015

Moscovici ruining all the fun by answering Greek related questions in French... #EC

— Mehreen (@MehreenKhn) May 5, 2015

The outlook for Europe’s economy looks brighter than at any time since the financial crisis began in 2008, according to today’s report.

It says:

The recovery from the crisis and the double-dip recession has been a long and tedious one, marked by numerous setbacks, but now there are clear indications that a cyclical upswing is underway, supported by economic tailwinds.

And those tailwinds include the ECB’s quantitative easing programme, the weaker euro (thanks to QE!), and the cheaper oil price.

The EC’s new Spring forecasts are online here (pdf).

Despite Greece’s woes, the EC believes Europe’s economy is healing -- with faster-than-expected growth forecast this year.

In the EU, the #deficit is forecast to decline from 2.9% of GDP in 2014 to 2.5% this year and 2.0% in 2016 @ecfin #ECForecast

— Pierre Moscovici (@pierremoscovici) May 5, 2015

The fiscal outlook is improving: in the euro area, the #deficit is forecast to fall from 2.4% of GDP in 2014 to 2.0% this year #ECForecast

— Pierre Moscovici (@pierremoscovici) May 5, 2015

It has also raised its inflation forecast, and no longer fears a long stretch of falling prices:

Annual consumer price #inflation in both the EU and euro area is expected to rise from 0.1 % this year to 1.5 % in 2016 @ecfin #ECForecast

— Pierre Moscovici (@pierremoscovici) May 5, 2015

#BREAKING The Eurozone deflation that wasn't. https://t.co/DmBOnNwnVG

— Frederik Ducrozet (@fwred) May 5, 2015

Moscovici: We had to cut Greece's growth forecasts

European Commissioner Pierre Moscovici is outlining today’s growth forecasts now.

He tells reporters in Brussels that the EC was forced to cut its forecast for 2.5% growth in Greece this year, to just 0.5%, given recent events.

In the light of the persistent uncertainty [in Greece], a downward revision has been unavoidable.

The EC has also revised down its forecast for 2016, from 3.6% growth to 2.9%. That assumes, though that there is a deal over its bailout this summer.

I’ll collect all the growth forecast together shortly, but in the meantime this map shows the hot spots and the laggards:

#ecforecast for #EU - GDP up to 1.8% in 2015, 2.1% in 2016 http://t.co/PvwXoZE3z5 pic.twitter.com/zQ1BJEdLmE

— DG ECFIN (@ecfin) May 5, 2015

New @EU_Commission forecast for #Greece pretty dire, but based on assumption of bailout deal "by June" & subsequent return to biz confidence

— Peter Spiegel (@SpiegelPeter) May 5, 2015

The EC is also warning that Greece is failing to get to grips with tax collection.

In forecasts, @EU_Commission says #Greece tax collection at end-2014 was so low that 2014 primary surplus only 0.4%, down from 1.7% estimate

— Peter Spiegel (@SpiegelPeter) May 5, 2015

The EC is warned that Greece’s recovery has stalled since the previous government called snap general elections at the end of last year.

Political uncertainty has been fuelled by the “lack of clarity” over the present administration’s polities, it says, adding that the Greek factory sector is still locked in a depression.

#ecforecast Grim for Greece pic.twitter.com/e0N1fTV9Lf

— Bruno Waterfield (@BrunoBrussels) May 5, 2015

EC slashes Greek growth forecast

The EC has also slashed its forecast for Greece’s growth rate this year, in another signal that its bailout programme is off track.

Brussels now expects Greece’s GDP will expand by just 0.5% in 2015, down from a previous forecast of 2.5%.

And that pushes up the country’s debt/GDP ratio even higher, to 180% of national output.

In new forecasts, @EU_Commission slashes #Greece outlook. 2015 growth to 0.5% from 2.5% in Feb. Debt from 170.2% to 180.2%

— Peter Spiegel (@SpiegelPeter) May 5, 2015

This will surely surely fuel concerns over Greece’s financial position, with the IMF already warning that Athens is missing its target for a primary surplus (see earlier post)

As Antonio Garcia Pascual, Barclays’ chief European economist, explained on Bloomberg TV a few minutes ago:

Both from the European and IMF perspective, the programme must be fully funded...

The bigger the hole, the more funds must come in.

Breaking: The European Commission has raised its growth forecast for the eurozone this year, from 1.3% to 1.5%.

Reminder, it’s nearly time for the European Commission to publish its new spring forecasts (live feed here from 10am BST/11am Brussels time)

Press conference w/@pierremoscovici on #ecforecast @ 11am here: http://t.co/rmUNKa0V6h pic.twitter.com/Pls6L6NFo9

— DG ECFIN (@ecfin) May 5, 2015

We’re expecting the EC to cut its growth forecasts for Greece.....

UK construction growth slows as political deadlock looms

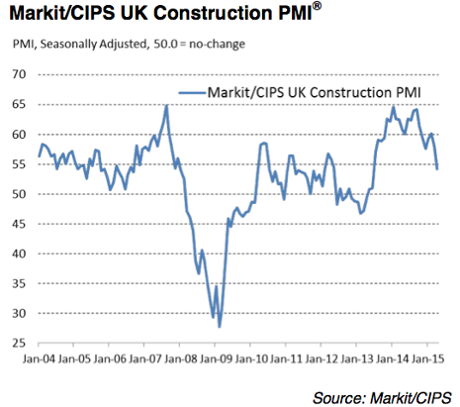

Growth in Britain’s construction sector slowed last month, as Thursday’s general election casts a shadow over building work.

Although the sector expanded, growth was the weakest in almost two years, with firms reporting a sharp drop in new work. But it’s not all bad -- firms are still hiring new workers.

Markit’s construction PMI, based on interviews with hundreds of UK building firms, dropped to 54.2, from 57.8 in March. That’s the lowest since June 2013 (and closer to the 50-point mark splitting expansion from contraction).

It’s the latest sign that the recovery is losing some momentum. But.... business confidence is still quite high; it appears clients are holding back from taking spending decisions until Britain has gone to the polls, given forecast of a hung parliament.

Tim Moore of Markit explains:

“April’s survey highlights another growth slowdown across the UK construction sector, with new work expanding at the weakest pace for almost two years.

“The uncertain general election outcome appears to have put some grit in the wheels of decision making. Construction firms widely noted delays with clients’ budget setting and a reduced propensity to commit to new projects.

“Despite experiencing pre-election risk aversion among clients in April, construction companies indicated a strong degree of confidence regarding the year-ahead outlook.

Greek 10Y bonds wider by 52bps over German 10Ys after FT article suggesting Greece may lose support of IMF weighs on Greek assets

— RANsquawk (@RANsquawk) May 5, 2015

Greek bonds hit by IMF fears

Greek bonds are weakening this morning, after it emerged that the International Monetary Fund believes Greece’s finances are badly off track (see earlier post for details).

The yield (effectively the interest rate on Greece’s two-year bonds has jumped by more than one percentage point this morning to 20.7%, up from 19.5% on Monday night.

Greece’s 10-year debt is also under some pressure, pushing its yield up over 11%, from 10.4%. Yields rise when prices fall.

The IMF is due to provide around half the €7.2bn of outstanding bailout funds to Greece; so the consequences could be severe if the Fund does withhold its share.

Updated

Austria: Progress, but no Greek breakthrough

Austria’s finance minister, Hans Jörg Schelling, has warned that there’s no guarantee of a deal with Greece in time for next week’s meeting of eurozone finance ministers (on May 11)

Schelling added that Greece has made some compromises, but is still holding firm on other issues.

Reuters has the details:

- 08:40:00 - AUSTRIAN FINANCE MINISTER SCHELLING SAYS SEES PROGRESS IN GREEK DEBT TALKS, NO BREAKTHROUGH YET

- 08:40:00 - AUSTRIA’S SCHELLING - CAN’T SAY IF THERE WILL BE A DEAL ON GREEK DEBT ON MAY 11, NEGOTIATIONS CONTINUE

- 08:40:00 - AUSTRIA’S SCHELLING SAYS GREECE HAS CHANGED POSITIONS IN SOME AREAS, NO MOVEMENT IN OTHERS AREAS

Updated

What can Greece hope to achieve by meeting Mario Draghi today?

Well, according to the Kathimerini newspaper, Greek deputy PM Dragasakis has an “optimistic plan” to push the ECB to lift its restrictions preventing Greece issuing more short-term debt. More here.

I’d be surprised if Draghi was swayed -- given the amount of support the ECB has already given to Greece, and concerns that its banks are suffering deposit outflows.

The meeting also comes a day before the ECB decides whether to continue providing liquidity assistance to Greece’s banks.

Spanish unemployment tumbles by 118k

Spain’s unemployment total has fallen by a record amount last month, as the country’s recovery continues to gain pace.

The number of people unemployed across Spain tumbled by over 118,000 in April, twice as much as economists had expected.

That’s a record drop for any April, according to Madrid. But it still leaves more than one in five adults out of work.

Nearly 5x as fast as the average (-25k) for the last seven Aprils.

— Mike Bird (@Birdyword) May 5, 2015

Spain registered unemployment falls 118.923 in April, government claims biggest monthly fall on record. pic.twitter.com/Pu30h04uUg

— The Spain Report (@thespainreport) May 5, 2015

Updated

Athens could come under even more pressure if the European Commission downgrades its economic forecasts for Greece this morning, points out analyst Yannis Koutsomitis.

#EU Commission to publish Spring 2015 Economic Forecast today. Possible revision of #Greece growth forecast wll heavily affect bailout talks

— Yannis Koutsomitis (@YanniKouts) May 5, 2015

The BBC ran an interesting piece last night, explaining how Greece’s government has already missed a swath of payments to Greek workers and companies.

That doesn’t count as an official default, of course, but it underlines how perilous Greece’s financial position has become this year.

Here’s a flavour:

A junior doctor told the BBC that although wages were paid regularly to medical staff, the government was more than four months behind on payments for on-call time.

“Last week we got paid on-call time for the month of December,” she said.

Hospital suppliers that provide healthcare units with everything from bandages to dialysis machines warned last week that they may be forced to stop supplying hospitals.

“In the past four months we are experiencing an undeclared suspension of payments,” their associations said in a recent statement.

Greece's undeclared domestic default http://t.co/GX8YqOTSUS

— Simon Nixon (@Simon_Nixon) May 5, 2015

Eurozone crisis experts are alarmed by the news that the IMF could pull funding for Greece unless it receives debt relief.

Here’s some early reaction:

#IMF gradually pulling rug out from under #Greece by saying that #eurozone Govs need to take debt rightdown before they’ll extend bailout

— Robin Bew (@RobinBew) May 5, 2015

Focus remains on Greece with the latest reports suggesting the IMF could reduce financial aid to the nation....

— RANsquawk (@RANsquawk) May 5, 2015

IMF may hold back its half of the €7.2bn bailout aid that Greece needs. Without the funds, Greece could run out of cash this month.

— James Bevan (@jamesbevan_ccla) May 5, 2015

A new Greek opinion poll shows that a majority of the population want to stick with the euro, with roughly a third favouring Grexit.

Macedonia Uni poll for Skai TV In referendum on euro with new MoU vs drachma, what would you choose? Euro 55.5% Drachma 35% N/A 9.5% #Greece

— MacroPolis (@MacroPolis_gr) May 5, 2015

And few people think things would be better if New Democracy were still in power:

Macedonia Uni poll for Skai TV If Samaras was in power, economic situation would be Worse 56.5% Same 21.5% Better 15.5% N/A 6.5% #Greece

— MacroPolis (@MacroPolis_gr) May 5, 2015

Overnight, Australia’s central bank cut interest rates to a fresh record low of 2%.

The move (covered in this liveblog), is intended to ward off an economic slowdown in Australia. But if the RBA hoped to weaken the Aussie dollar, it’s been disappointed -- the currency did drop (as you’d expect) before bouncing back smartly:

Do "currency wars" reach a new phase when rate cuts don't have any negative effect? RBA cut, A$ up.

— kit juckes (@kitjuckes) May 5, 2015

So RBA cut, bonds yields up, Shares down and aud up. Maybe better if held and kept easing bias #ausecon

— Con Michalakis (@MichalakisCon) May 5, 2015

FT: IMF is pushing for more Greek debt relief

Today’s meetings are overshadowed by the news that the International Monetary Fund fears that Greece’s debt mountain has become unsustainable again.

According to the Financial Times, the IMF believes Greece may run a primary budget deficit of 1.5% this year, far from the 3% surplus it was aiming for.

That would push Greece’s debt/GDP levels even higher, meaning it could face even tougher austerity unless eurozone creditors agreed to write off some debts.

The FT’s Peter Spiegel explains:

Greece is so far off course on its $172bn bailout programme that it faces losing vital International Monetary Fund support unless European lenders write off significant amounts of its sovereign debt, the fund has warned Athens’ eurozone creditors.

The warning, delivered to eurozone finance ministers by Poul Thomsen, head of the IMF’s European department, raises the prospect that it may hold back its portion of a €7.2bn tranche of bailout aid that Greece is desperately attempting to secure to avoid bankruptcy.

Full story: IMF takes hard line on aid for Greece

IMF says #Greece now running primary deficit of nearly 1.5% of GDP; warns #eurogroup debt relief may be necessary http://t.co/qsM7aGUqWS

— Peter Spiegel (@SpiegelPeter) May 4, 2015

Greece’s national debt is already 177% of GDP; which many economists believe is simply unsustainable without some relief.

And if the IMF are right, it would also mean that a third Greek bailout might have to be even larger than the €50bn that had been predicted.

Updated

The Agenda: Greek meetings, EC forecasts....

Good morning. We’re back after Monday’s Bank Holiday break to track the latest developments around Greece’s bailout talks, plus the world economy, the financial markets, the eurozone and business.

Coming up....Greece’s government is scrambling to reach a breakthrough over its bailout before running out of cash.

Finance minister Yanis Varoufakis is in Paris this morning to meet his French counterpart, Michel Sapin, before heading on Brussels to see European Economic and Monetary Affairs commissioner Pierre Moscovici.

But the key meeting could be in Frankfurt this afternoon, when deputy Greek PM Yiannis Dragasakis meets ECB chief Mario Draghi. Euclid Tsakalotos, who is now leading Greece’s negotiations with its creditors, is also attending.

With no deal in sight, despite days of negotiations in Brussels, Greece is still pushing for a breakthrough with its creditors ahead of the next Eurogroup meeting on May 11th. But the two sides are still divided over key issues such as pensions and labour market reforms.

Yesterday, Greece insisted it would continue to meet its debt repayments, as the crisis grinds on:

In other news...

The European Commission is set to sound the alarm over Greece’s economy, when it publishes its latest growth and inflation forecasts at 10am BST. It may cut its Greek forecasts, but also predict faster expansion across the wider eurozone.

Banking giant HSBC is releasing its first-quarter results this morning, at 9.15am BST. It’s expected to put more money aside to cover the cost of its role in the foreign-exchange rate-rigging scandal.

Markit releases its latest assessment of the UK’s construction industry, at 9.30am BST.

And we get the latest Spanish unemployment data sometime after 8am BST.

London’s stock market is expected to rally, as City traders play catch-up after yesterday’s break. Here’s IG’s opening prices:

-

FTSE 7033 +47 points

-

German DAX 11603 -17

-

French CAC 5078 -4

-

Spanish IBEX 11424 -5

-

Italian FTSE MIB 23180 -37

Updated