Very rarely do we stop to think what the balance printed on our bank statements really means. To most of us, most of the time, our bank balance means cash that’s readily available for us to withdraw and use. Rarely do we think about it as a kind of IOU that the bank will do its best, in conjunction with certain laws and oversight, to honor when we wish to redeem it.

Even more rarely do we consider the chance that the bank will not be able to make good on that IOU. The recent collapse of Silicon Valley Bank and Signature Bank has forced us to consider that the balance printed on our bank statements in certain cases can be very different from cash in our wallets.

For balances under $250,000, there is less to consider when it comes to safety, as the FDIC has proven an efficient operator when interceding in failing banks and making insured balances quickly available. However, the insurance limit has not changed since 2008 and is not indexed to inflation.

As we’ve seen, the insurance limit can, for all intents and purposes, be much higher in certain cases. But even in the case where Silicon Valley Bank and Signature Bank were deemed systemically important and all deposits were covered, there were a few hair-raising days where the value of those deposits was in question. Certainly not the type of uncertainty we typically associate with bank deposits.

Investors today may be asking themselves: Where else should I consider putting my cash? Below are a few alternatives to consider.

FDIC Sweep Programs

FDIC-insured sweep programs are offered by brokerage firms. These programs “sweep” client cash into FDIC-insured bank accounts. In some cases, clients’ deposits are fanned out across multiple banks to provide higher levels of FDIC protection. Like bank accounts, yield can vary across programs, with some programs offering highly competitive yields. Coupled with the potential for higher levels of FDIC insurance, brokerage sweep programs are an attractive alternative to a traditional savings account.

Money Market Mutual Fund

A money market mutual fund (MMMF) is a mutual fund that seeks to keep its share price fixed at $1 and generate interest income. MMMFs are different from money market accounts offered by banks and credit unions. MMMFs are investable securities and do not carry FDIC insurance. Funds invest in U.S. Treasuries and other high-quality fixed income securities.

There are also MMMFs that invest in municipal securities, where interest can be exempt from federal, state and local taxes. MMMFs generally offer competitive yields. These yields fluctuate with the market, since the yield is generated by the securities held by the fund.

While funds seek to keep their share price fixed, there is no guarantee. Though exceedingly rare, funds in the past have “broken the buck,” or seen the share price drop below $1. In times of stress, funds can institute gates on withdrawals to help preserve share value.

Treasuries

Generally considered one of the safest assets on the planet, U.S. Treasuries are bonds issued directly by the U.S. government. Investors should keep in mind that the value of Treasuries can fluctuate while they are being held to maturity. Interest income is also exempt from state and local taxes.

Short-Term Bond Funds

For investors who are willing to take a bit more risk, short-term bond funds can deliver increased yield while remaining relatively safe. These funds invest in fixed income securities that mature in the near future. The short maturities mean that there’s limited impact to the fund price when interest rates change, and the yield generated by the fund generally tracks changes in interest rates.

Investors can think of these funds as one step further on the risk spectrum compared to money market mutual funds. Similar to money market funds, there are also municipal versions that can generate tax-exempt interest.

Stocks?!

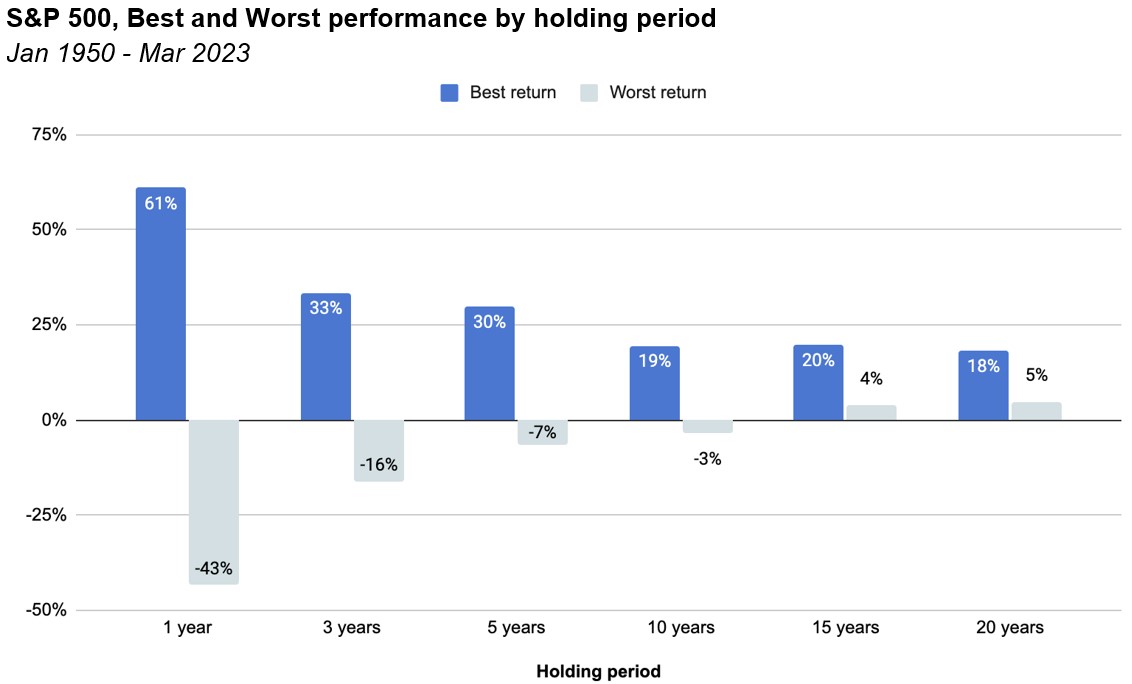

If you are holding a sizable position in cash, you might be missing out on returns. Broadly diversified stocks, measured by the S&P 500, have outperformed cash by 11% on an annualized basis since 1950.

Of course, stocks are significantly riskier, but as your holding period lengthens, the risk of loss tends to decrease. Since 1950, the worst one-year return for the S&P 500 was -43% (3/2008-3/2009). However, the worst five-year return was -6.6%. Extend your holding period to 15 years, and the worst return is actually positive (3.8%).

The last few months have surfaced risks to the traditional savings account that investors have not had to consider for some time.

Luckily, there are a number of other options for investors to park their cash that can deliver compelling yields and, in some cases, higher levels of safety.