/Becton%20Dickinson%20%26%20Co_%20BACTEC%20by-%20TheBlueHydrangea%20via%20Shutterstock.jpg)

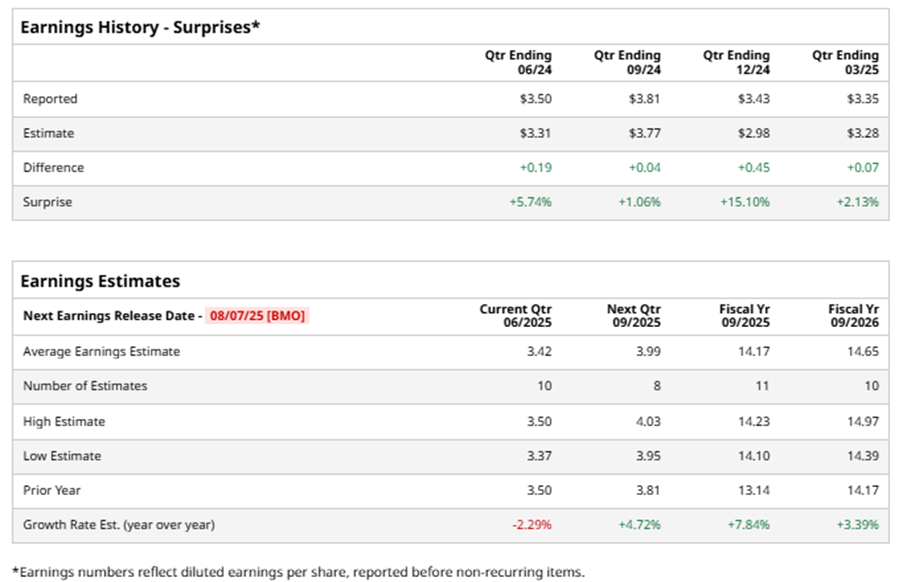

Becton, Dickinson and Company (BDX) develops, manufactures, and sells medical supplies, devices, laboratory equipment, and diagnostic products. Valued at $52.3 billion by market cap, the company offers solutions that help advance medical research and genomics, enhance the diagnosis of infectious diseases and cancer, improve medication management, and promote infection prevention. The global medical technology giant is expected to announce its fiscal third-quarter earnings for 2025 before the market opens on Thursday, Aug. 7.

Ahead of the event, analysts expect BDX to report a profit of $3.42 per share on a diluted basis, down 2.3% from $3.50 per share in the year-ago quarter. The company has consistently surpassed Wall Street’s EPS estimates in its last four quarterly reports.

For the full year, analysts expect BDX to report EPS of $14.17, up 7.8% from $13.14 in fiscal 2024. Its EPS is expected to rise 3.4% year over year to $14.65 in fiscal 2026.

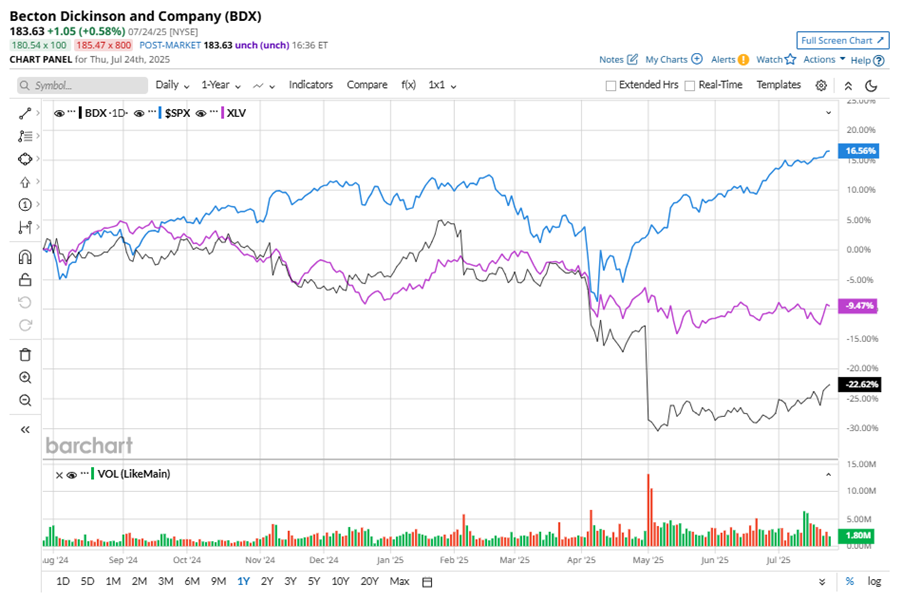

BDX stock has significantly underperformed the S&P 500 Index’s ($SPX) 17.3% gains over the past 52 weeks, with shares down 22.6% during this period. Similarly, it underperformed the Health Care Select Sector SPDR Fund’s (XLV) 9.4% dip over the same time frame.

BDX's underperformance is attributed to a software recall in its Alaris infusion pump systems. Software issues in the Alaris Systems Manager and Care Coordination Engine Infusion Adapter can cause delayed responses and potentially incorrect therapy administration, posing risks to patient safety. The recall affects critical components that integrate the pump with hospital electronic medical record systems.

On May 1, BDX shares closed down more than 18% after reporting its Q2 results. Its adjusted EPS of $3.35 exceeded Wall Street's expectations of $3.28. The company’s revenue was $5.3 billion, falling short of Wall Street forecasts of $5.4 billion. BDX expects full-year adjusted EPS in the range of $14.06 to $14.34, and expects revenue in the range of $21.8 billion to $21.9 billion.

Analysts’ consensus opinion on BDX stock is reasonably bullish, with an overall “Moderate Buy” rating. Out of 17 analysts covering the stock, seven advise a “Strong Buy” rating, one suggests a “Moderate Buy,” and nine give a “Hold.” BDX’s average analyst price target is $213.71, indicating a potential upside of 16.4% from the current levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.