/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

Super Micro Computer (SMCI) has undoubtedly made its mark in the server market with high-performance systems tailored for artificial intelligence (AI) and data-heavy workloads. However, its most recent earnings report, released in early August, was a disappointment. The stock tumbled more than 18% on Aug. 6, sparking concerns about its ability to keep pace in an increasingly competitive server landscape. And now, Hewlett Packard Enterprise Company (HPE) is preparing to take the stage with its upcoming third-quarter earnings report.

As one of SMCI’s top rivals, HPE commands a broad portfolio of server offerings, including ProLiant, Synergy, BladeSystem, and Moonshot, while expanding its presence in hybrid cloud and AI-driven infrastructure. This strategy is reinforced by its latest $14 billion acquisition of Juniper Networks, a leader in AI-driven networking, which expands HPE’s reach in hybrid cloud and data center infrastructure.

With HPE stepping up its game, all eyes are now shifting to this next big server player, set to report its earnings on Sept. 3.

About HPE Stock

Hewlett Packard Enterprise is a leading provider of enterprise technology, combining AI, cloud, and networking to help organizations operate more efficiently. The company supports customers across various industries by enhancing performance, transforming data into actionable insights, and driving measurable impact. Through its edge-to-cloud platform, HPE GreenLake, the company delivers cloud services with the flexibility of on-premises control.

Most notably, HPE closed its $14 billion all-cash acquisition of Juniper Networks on July 2, 2025, following approval from the U.S. Department of Justice (DOJ). The deal, first announced in January 2024, resulted in HPE shares gaining a nearly 3.8% boost on the day of completion. Juniper adds significant strength in AI-native networking, led by its Mist AI platform for data center and cloud networking.

Valued at approximately $29.5 billion by market capitalization, shares of HPE have soared 18.8% over the past year, outshining the broader S&P 500 Index’s ($SPX) 15.4% return during the same stretch. And after a slow start to 2025, the rally has gained momentum recently, with shares climbing nearly 28% in just the last three months, outpacing the index’s 10.7% rise.

From a valuation standpoint, HPE looks relatively bargain. The stock trades at just 14 times forward earnings, well below the sector median of 23.5 times. Even compared to peers riding the AI wave, such as SMCI, which trades at around 20 times forward earnings, HPE appears to offer a more affordable entry point.

HPE Q2 Earnings Recap: Key Highlights for Investors

On June 3, HPE closed out its second quarter of fiscal 2025 with results that topped Wall Street’s expectations, fueled by strong demand for its AI servers and momentum in hybrid cloud. The company reported revenue of $7.6 billion, representing a 5.9% year-over-year (YOY) increase and exceeding consensus estimates of approximately $7.5 billion.

While non-GAAP EPS slipped 10% YOY to $0.38, the figure still cleared analyst forecasts of $0.33, reflecting solid execution despite margin pressure. Breaking it down by segment, server revenue totaled $4.1 billion, representing a 6% increase from the prior-year period, driven by strong AI-driven demand. Intelligent Edge posted revenue of $1.2 billion, marking 7% growth YOY, while Hybrid Cloud delivered $1.5 billion in revenue, climbing 13% from the same quarter last year.

Meanwhile, the Annualized Revenue Run Rate (ARR) reached $2.2 billion, soaring 46% YOY, underscoring the growing stickiness of its recurring revenue model. The company also continued its commitment to returning capital to shareholders, distributing $221 million through dividends and share repurchases during the quarter.

Commenting on the performance, Marie Myers, CFO of HPE, noted: “We drove higher revenue year-over-year in Q2 across Server, Intelligent Edge, and Hybrid Cloud, and importantly in Server, we improved margin performance over the course of the quarter. We are maintaining our focus on achieving efficiencies and streamlining operations across our businesses to position HPE for the future and deliver financial results aligned with our fiscal 2025 outlook.”

Looking ahead, HPE is set to release its Q3 results after the market closes on Sept. 3. Management guided revenue to be in the range of $8.2 billion to $8.5 billion for the quarter. The company also expects GAAP EPS to fall between $0.24 and $0.29, while non-GAAP EPS is projected in the range of $0.40 to $0.45. At the same time, analysts tracking HPE project the company’s Q2 bottom line to decline 17.8% YOY to $0.37 per share.

What Do Analysts Think About HPE Stock?

HPE shares closed up nearly 3.7% on Aug. 21 after Morgan Stanley upgraded the stock to “Overweight” from “Neutral” and raised its price target to $28 from $22. The firm sees underappreciated upside from HPE’s $14 billion Juniper Networks acquisition, which strengthens its networking portfolio just as AI-driven demand is reshaping enterprise hardware and storage markets.

Morgan Stanley argued that the market hasn’t fully priced in the potential earnings boost from the Juniper deal. In fact, if HPE were valued more in line with peers, analysts believe the stock could trade up to $39 in the most bullish scenario, offering far more upside than investors currently expect.

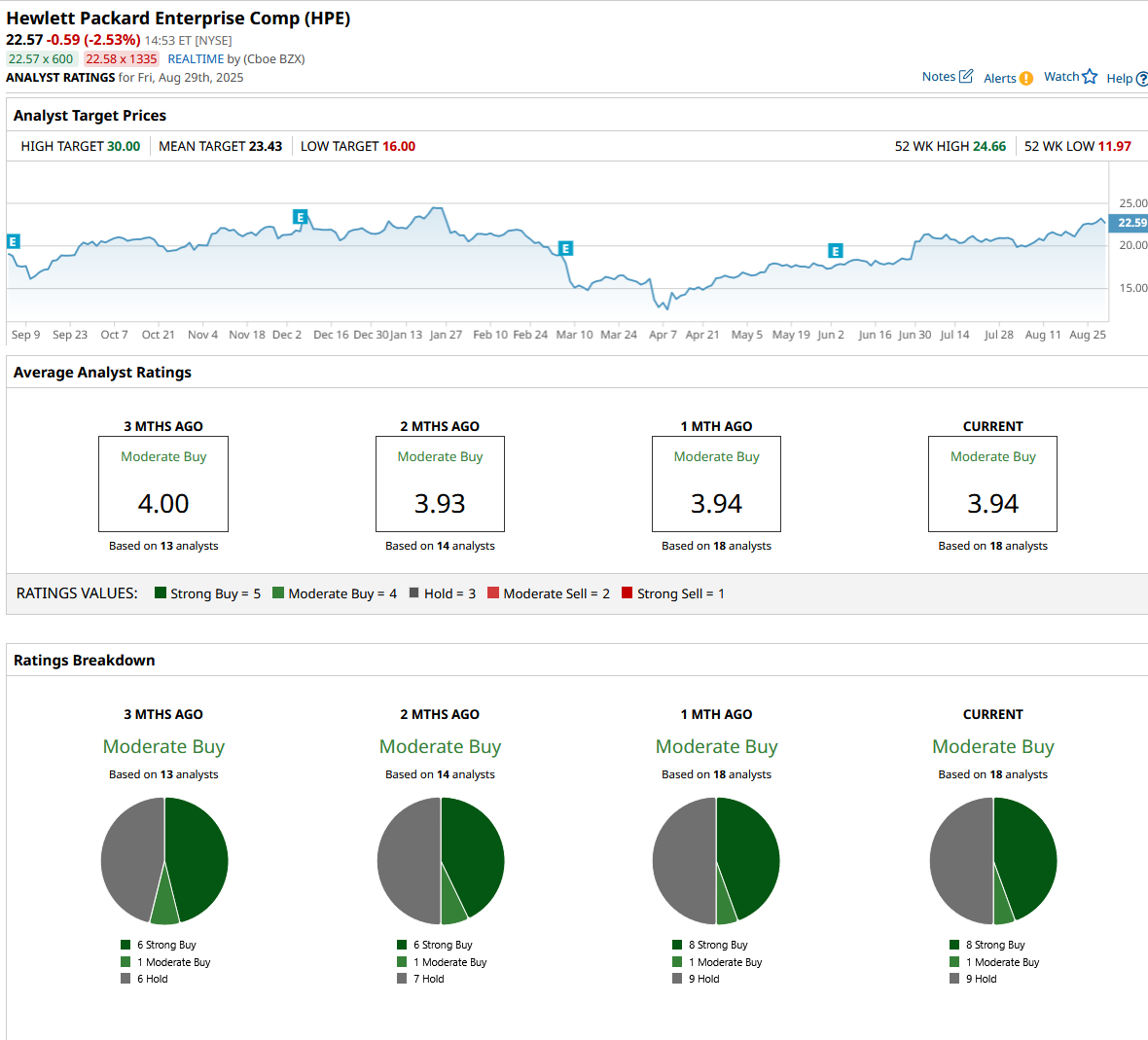

With the clock ticking down to HPE’s Q3 earnings, sentiment on Wall Street is leaning positive, with the stock carrying a consensus “Moderate Buy” rating overall. Of the 18 analysts offering recommendations, eight advocate a “Strong Buy,” one leans toward a “Moderate Buy,” and the remaining nine urge investors to “Hold.”

The average analyst price target of $23.43 represents potential upside of only 3.8% from current market prices. However, the Street-high target of $30 suggests an impressive 33% rally from current levels.