/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

Alibaba Group Holding Limited (BABA) investors may want to circle June 30 on their calendars because a new U.S. defense-related restriction tied to the company is about to take effect. The U.S. Department of Defense (DoD)has officially added Alibaba Group to its list of “Chinese military companies,” a designation that is escalating tensions between D.C. and Beijing and raising fresh questions about the future risks facing Chinese tech giants listed in the U.S.

While the designation does not immediately impose broad sanctions on Alibaba, the upcoming June 30 deadline is important because it marks the beginning of new Pentagon-related procurement restrictions involving companies placed on the list. The move is part of a broader U.S. effort to limit business ties with Chinese firms that American officials believe support China’s military-industrial ecosystem. Starting June 30, the DoD will prohibit direct contracting with designated Chinese military companies, with broader supply-chain restrictions taking effect on June 30, 2027.

Alibaba has strongly denied the allegations, arguing there is “no basis” for its inclusion and insisting it is not connected to China’s military. Still, the announcement introduces another layer of geopolitical uncertainty for investors already navigating U.S.-China trade tensions, export controls, and growing scrutiny of Chinese technology companies operating globally.

About Alibaba Group Stock

Alibaba Group Holding Limited is a Chinese multinational technology conglomerate, best known for its dominance in e-commerce (Alibaba.com, Taobao, Tmall), cloud computing, digital media, logistics, and financial services. Headquartered in Hangzhou, China, the company operates a sprawling ecosystem that serves consumers, merchants, and enterprises globally. Alibaba has a market cap of around $287.2 billion.

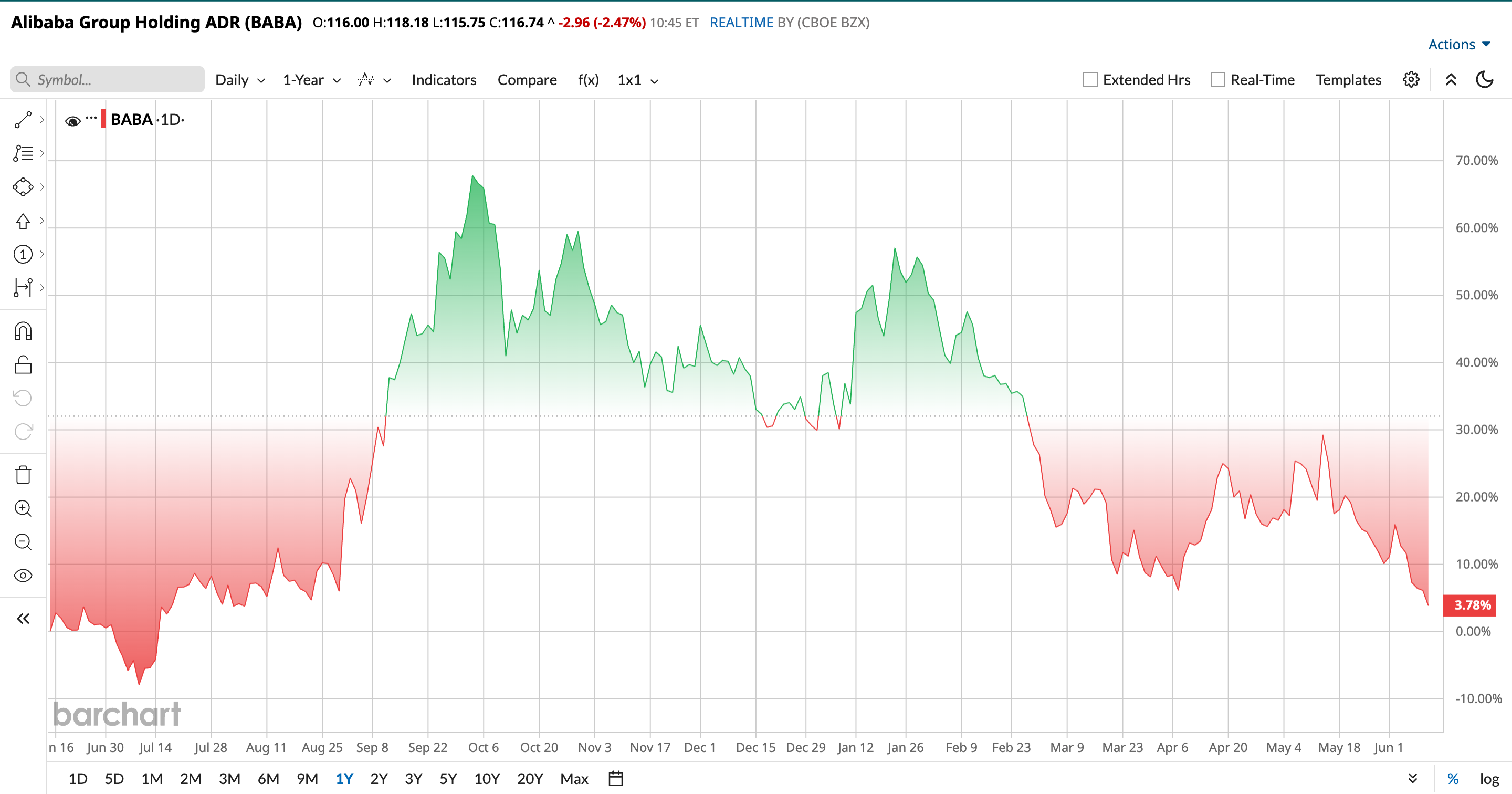

Shares of Alibaba Group have come under heavy pressure in recent weeks, with investor sentiment deteriorating amid rising geopolitical tensions, renewed regulatory concerns, and broader weakness. BABA stock has declined 16.1% over the past month, erasing a significant portion of its earlier AI-driven rally as investors reassess the risks tied to the U.S.-China relations.

The recent sell-off accelerated after the U.S. Department of Defense added Alibaba to its list of Chinese military companies, a move that raised fears about potential procurement bans, supply-chain restrictions, and tighter U.S. investment scrutiny. Those concerns have weighed heavily upon market sentiment even as Alibaba continues to push aggressively into artificial intelligence, cloud computing, and e-commerce expansion.

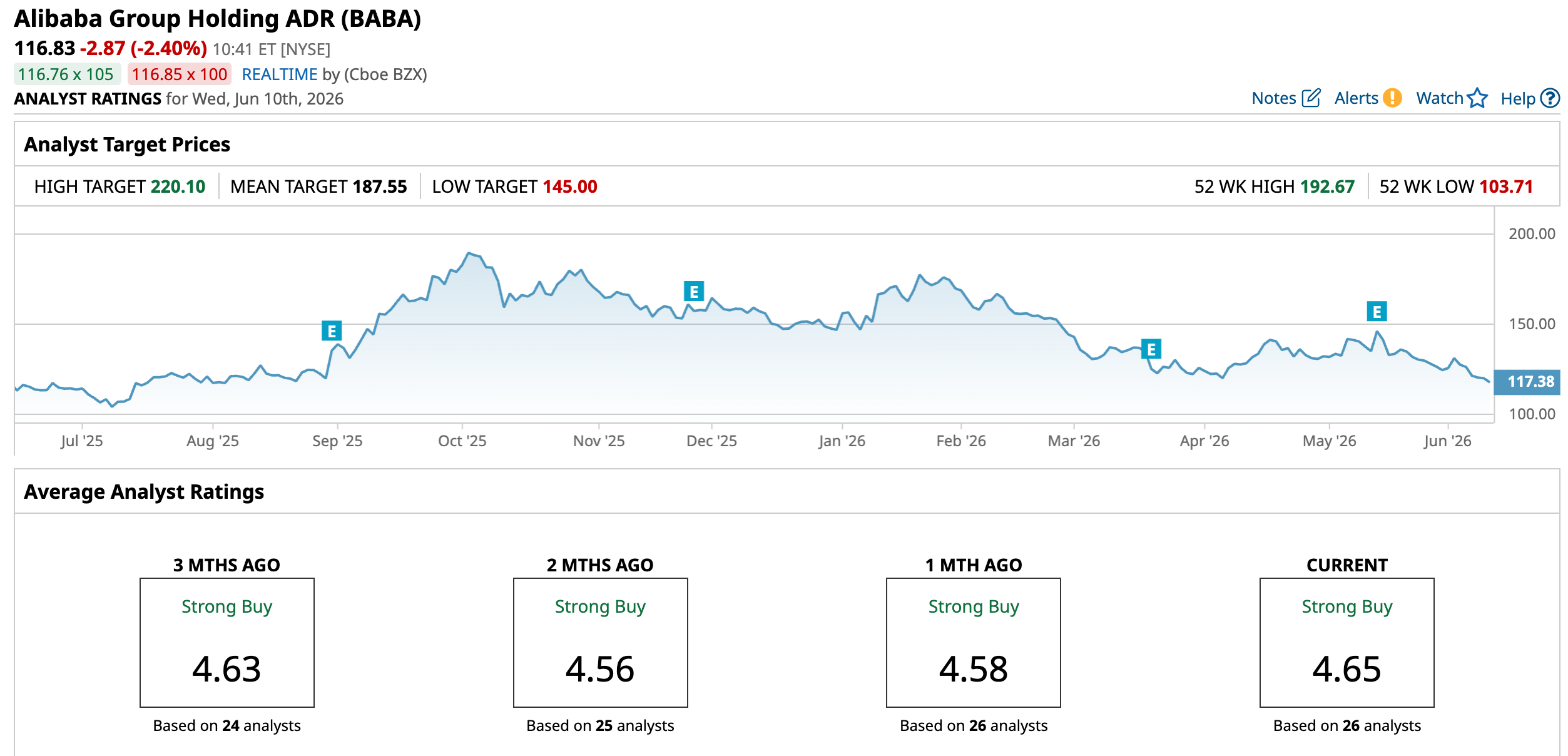

The stock is also down 19.8% year-to-date (YTD) and 3.6% over the past year. Meanwhile, shares are trading 39.4% below their 52-week high of $192.67 reached in October 2025, highlighting the magnitude of the recent pullback.

The stock is trading at a lofty valuation compared to its industry peers at 17.94 times forward price-to-earnings.

Bleak Bottom-Line Performance

Alibaba Group reported its fiscal fourth-quarter and full-year 2026 financial results on May 13, 2026, with results highlighting a major strategic shift toward AI, cloud infrastructure, and quick commerce investments.

For the fiscal fourth quarter ended March 31, Alibaba generated revenue of RMB 243.4 billion ($35.3 billion), representing 3% year-over-year (YOY) growth. Moreover, Cloud Intelligence revenue surged 38% YOY, with external cloud revenue accelerating 40%, fueled by strong enterprise AI demand. Management said AI-related products now account for roughly 30% of external cloud revenue.

Despite the revenue growth, profitability deteriorated sharply. Quarterly non-GAAP net income plunged significantly to just RMB 86 million ($12 million) from RMB 29.85 billion in the prior-year quarter. Non-GAAP earnings per ADS fell to RMB 0.62, missing analyst expectations by a wide margin. Income from operations swung to a loss of RMB 848 million ($123 million) compared with operating income of RMB 28.5 billion a year earlier, as Alibaba ramped up spending on AI infrastructure, cloud capacity, user acquisition, and quick commerce expansion.

For the full fiscal year 2026, Alibaba reported revenue of RMB 1.02 trillion ($148.4 billion), up 3% YOY. However, operating profitability weakened materially. Income from operations declined 64% YOY to RMB 50.2 billion ($7.3 billion), while adjusted EBITA dropped 56% to RMB 76.4 billion ($11.1 billion).

Full-year non-GAAP net income fell 62% to RMB 60.7 billion ($8.8 billion), while non-GAAP earnings per ADS dropped 59% YOY to RMB 26.80, a decrease of 59%. Free cash flow was an outflow of RMB 46.6 billion ($6.8 billion) compared with an inflow of RMB 73.9 billion in fiscal 2025.

Management emphasized that the deterioration in near-term profitability was intentional and tied directly to long-term AI monetization opportunities. Management stated that Alibaba plans to exceed its previously announced RMB 380 billion ($56 billion) AI investment target over the next three years, citing strong early returns from AI cloud demand and enterprise adoption.

Analysts expect the company’s EPS to improve 109% YOY to $6.75 in fiscal 2027 and rise 40.4% to $9.48 in fiscal 2028.

What Do Analysts Expect for Alibaba Stock?

Despite ongoing regulatory concerns, Wall Street analysts remain broadly optimistic on Alibaba’s long-term outlook. Many investors are increasingly looking beyond the near-term geopolitical and policy headwinds and instead focusing on the company’s core strengths, including the rebound in its cloud computing division, accelerating AI-driven revenue growth, and its dominant position within China’s massive e-commerce market.

Last month, Benchmark maintained its “Buy” rating and $220 price target on Alibaba. The firm highlighted strong momentum in AI and cloud computing, improving quick commerce economics.

Also, Bernstein SocGen reiterated its “Outperform” rating and $180 price target on Alibaba.

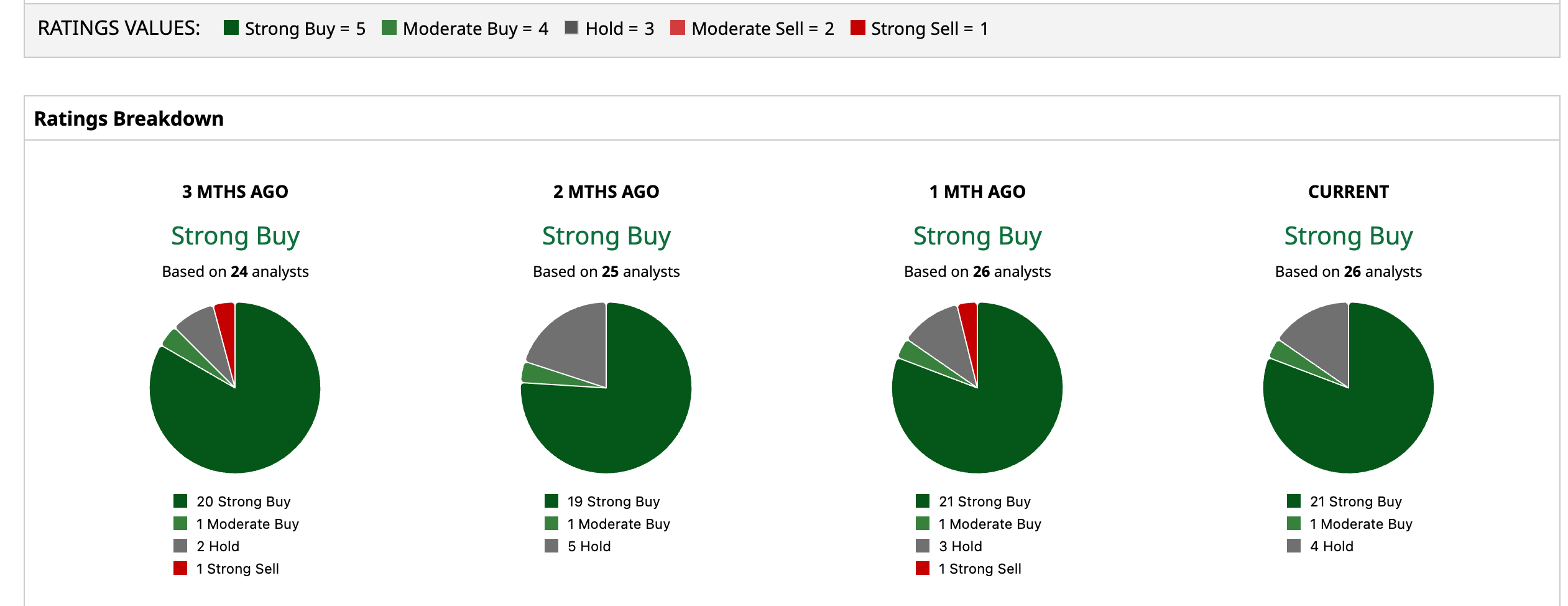

Overall, Alibaba has a consensus “Strong Buy” rating. Of the 26 analysts covering the stock, 21 advise a “Strong Buy,” one suggests a “Moderate Buy,” and the remaining four analysts give a “Hold” rating.

The average analyst price target for BABA is $187.55, indicating a potential upside of 60.5%. The Street-high target price of $220.10 suggests that the stock could rally as much as 88.4%.