/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)

When it comes to artificial intelligence (AI), Nvidia (NVDA) remains at the center of the global race. Demand for its cutting-edge AI chips shows little sign of slowing down. And perhaps most telling is that even in China—where Beijing has urged companies to embrace domestic alternatives—major players like ByteDance and Alibaba (BABA) are still pushing to secure Nvidia’s products.

This highlights two realities. First, Nvidia’s chips are seen as unmatched in performance and integration with its broader software ecosystem, creating what many analysts call a “moat” that domestic competitors such as Huawei and Cambricon are still struggling to replicate. Second, it underscores just how much Chinese tech giants, racing to stay at the forefront of AI, view Nvidia’s hardware as essential, even in the face of regulatory uncertainty and political headwinds.

For investors, the story raises a pressing question: with NVDA stock trading below $180, does this sustained appetite from Chinese tech giants signal a long-term buying opportunity, or should caution prevail until the political landscape clears? Let’s dive in to find out.

About NVDA Stock

Nvidia is a premier technology firm known for its expertise in graphics processing units and artificial intelligence solutions. The company is renowned for its pioneering contributions to gaming, data centers, and AI-driven applications. NVDA’s technological solutions are developed around a platform strategy that combines hardware, systems, software, algorithms, and services to provide distinctive value. The chipmaker’s market cap stands at $4.15 trillion, ranking it as the most valuable company in the world.

Shares of the AI darling have climbed 31.1% on a year-to-date (YTD) basis. NVDA stock is climbing today as a blowout outlook from Oracle boosted optimism that the AI infrastructure rollout is accelerating.

Chinese Companies Remain Eager for Nvidia Chips

In a surprising policy shift from the U.S.’s years-long technology restrictions on China, President Donald Trump in July allowed Nvidia to resume sales of its H20 AI chip tailored for the Chinese market, reversing the ban his administration had imposed in April. Still, instead of celebrating, Beijing’s reaction has been notably lukewarm, even though it has long pressed Washington to relax the strict export controls. That’s because China is concerned about alleged security risks tied to Nvidia’s H20 chips, such as “tracking and positioning” and “remote shutdown” features, which some U.S. lawmakers have pushed for but Nvidia insists are not built into its products.

Bloomberg reported in mid-August that Chinese regulators have summoned Nvidia representatives to discuss alleged “backdoor” security risks and urged local companies to avoid H20 chips. This also underscores Beijing’s push to develop a self-sufficient semiconductor supply chain and its confidence in the strides made by its fast-evolving chip industry. Notably, Chinese AI startup DeepSeek recently hinted that China would soon produce domestic “next-generation” chips to power its AI models.

Despite mounting pressure, Nvidia’s chips continue to be in high demand in China. Reuters recently reported that this is partly due to limited supplies from domestic competitors like Huawei and Cambricon. The report also noted that Nvidia’s chips perform better than local products. With that, Alibaba, ByteDance, and other Chinese tech firms remain eager to buy Nvidia’s AI chips. They are seeking confirmation that their orders for Nvidia’s H20 chips are being processed. They are also keeping a close eye on Nvidia’s plans for a more powerful chip, tentatively named B30A and built on its Blackwell architecture, according to the report.

Meanwhile, the B30A is expected to deliver up to six times the performance of the H20, which was built on the company’s previous-generation Hopper platform. The report said that the B30A will likely be priced at roughly twice the cost of the H20, which currently sells for between $10,000 and $12,000. And Chinese tech companies view the potential pricing of the B30A as attractive. However, although U.S. President Donald Trump has hinted he might allow more advanced Nvidia chips to be sold in China, U.S. regulatory approval is far from certain.

That said, let’s shift our focus back to the H20. Another reason Chinese companies are eager to get Nvidia products is the company’s powerful ecosystem, which tightly integrates its chips with its software platform, creating what experts describe as a “moat” that makes it challenging and expensive for AI developers to switch to other solutions after training their models on Nvidia’s software. “The H20 comes with a complete ecosystem covering both hardware and software support, ensuring better compatibility and ease of integration,” said Brady Wang, associate director at Counterpoint.

Despite Its Importance, China Still Holds Bad News for Nvidia

Now, it’s time for some bad news. Nvidia reported no new sales in China last quarter and expects zero AI chip sales to the country this quarter, too. That’s the exact reason why the company missed Q2 data center revenue estimates and gave Q3 revenue guidance that failed to meet investors’ lofty expectations. On the earnings call, Nvidia executives stated that while the company had obtained some export licenses for the H20, shipments had not yet begun as it was still resolving issues tied to an agreement to give 15% of its China sales to the U.S. government. Management also pointed to “geopolitical issues,” which analysts interpreted as likely referring to pressure from Chinese authorities on domestic firms to avoid buying Nvidia chips.

As I noted in my previous article, I consider China an important market for Nvidia. Nvidia’s Q2 earnings report clearly highlighted this importance. Had the company been able to sell H20 chips during the quarter, its data center revenue would have easily surpassed estimates, and more importantly, its Q3 revenue guidance would have exceeded even the loftiest expectations. Nvidia CFO Colette Kress said the company could ship between $2 billion and $5 billion worth of H20 chips to China this quarter if U.S. regulatory and “geopolitical issues” are resolved. The subdued post-earnings reaction in NVDA stock suggests to me that investors still expect the company to resume shipments this year, viewing the current situation as part of a high-stakes political chess game in U.S.-China trade negotiations.

Nvidia Continues to Fire on All Cylinders

Putting China aside for a moment and focusing on the company’s fundamentals, it’s clear that Nvidia’s growth story is still very much intact. The company delivered a double beat in its Q2 earnings report, released on Aug. 27. Its revenue continued to climb, coming in at $46.7 billion, up 6.1% sequentially and 56% year-over-year (YoY). The top-line figure surpassed estimates by $610 million. The critical Data Center segment, representing 88% of total revenue, grew 56% from a year ago and 5% sequentially to $41.1 billion, with Blackwell revenue rising 17% sequentially. Gaming revenue, the company’s second-largest revenue source, climbed 49% year-over-year to $4.3 billion. Meanwhile, Professional Visualization revenue increased 32% YoY, and Automotive and Robotics revenue surged 69% YoY.

On the profitability front, as the Blackwell ramp advances, Nvidia is experiencing a rebound in gross margins, just as management had previously outlined. Excluding H20-related charges and releases, adjusted gross margin came in at 72.3% in Q2, up one percentage point quarter-over-quarter but still below the 75.7% recorded a year ago. Its adjusted EPS stood at $1.04 (excluding H20-related charges/releases), up 52.9% and beating expectations by 3 cents.

Looking ahead, management projects Q3 revenue of $54 billion, plus or minus 2%, implying nearly 16% quarter-over-quarter growth and a 54% YoY increase. Although it fell short of investors’ lofty expectations, I view it as very solid. Moreover, as noted earlier, the outlook excludes any H20 shipments to China, leaving room for potential upside.

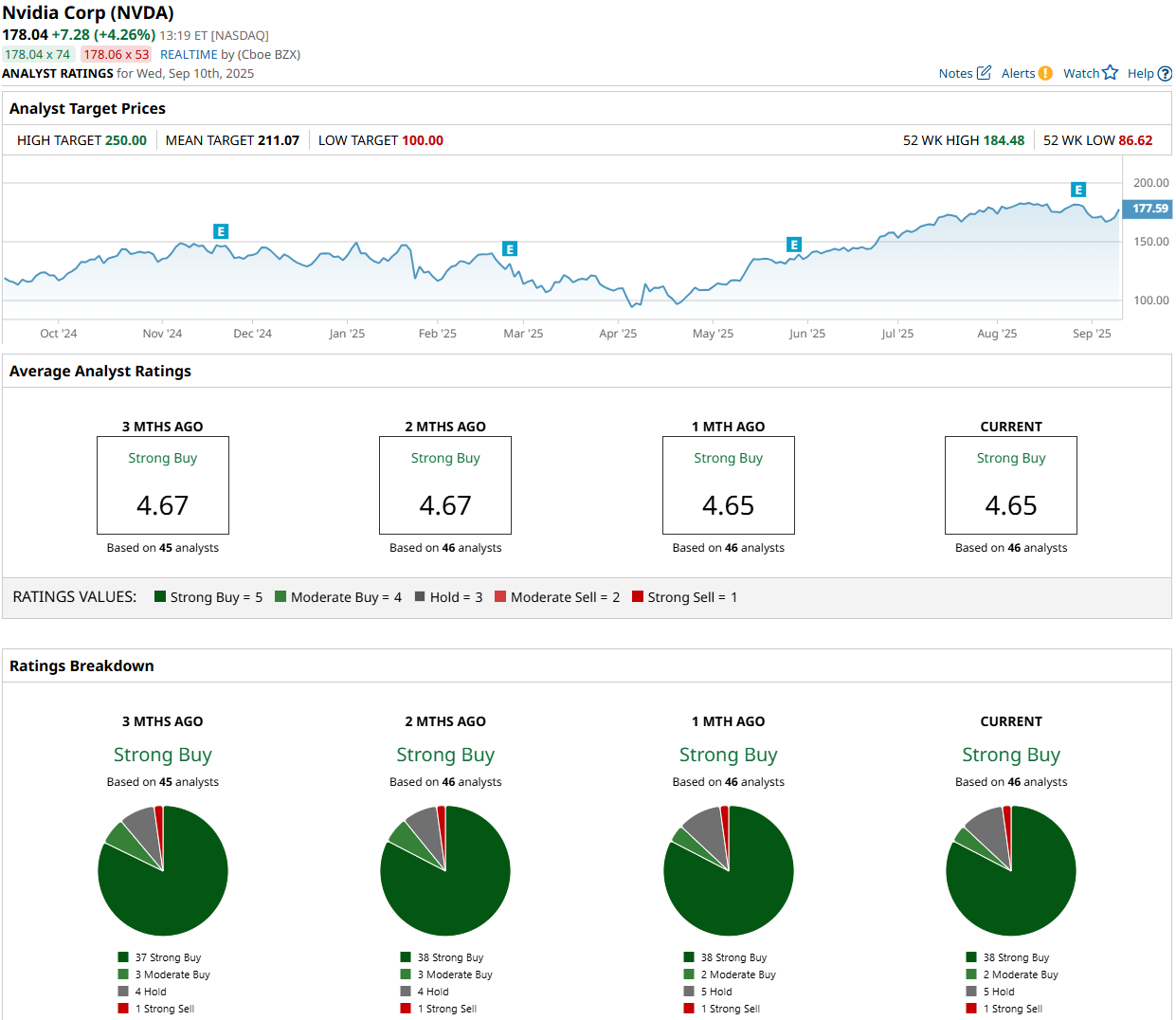

What Do Analysts Expect for NVDA Stock?

Wall Street analysts remain highly bullish about Nvidia’s growth prospects, as reflected in its consensus “Strong Buy” rating. Out of the 46 analysts covering the stock, 38 rate it a “Strong Buy,” two assign a “Moderate Buy” rating, five advise holding, and one rates it a “Strong Sell.” The average price target for NVDA stock stands at $211.07, indicating a potential upside of 18.6% from current levels.

The Bottom Line on NVDA Stock

Putting it all together, I believe every pullback is a buying opportunity for NVDA stock—and yes, it’s a “Buy” below $180. Nvidia’s most recent quarterly results reinforced its leadership in the AI market, highlighted by robust growth in both revenue and earnings. If political pressure surrounding the H20 eases from both the U.S. and China, Nvidia’s top line would receive a solid boost, likely prompting a revaluation of the company and a rise in its stock price. Nvidia CEO Jensen Huang noted that the Chinese market could represent a $50 billion opportunity for Nvidia with 50% annual growth. However, even without H20 shipments to China, the company is capable of delivering tremendous growth. That said, I believe we are still in the early stages of the AI revolution, with significant upside potential remaining for NVDA stock.