Burlington, Massachusetts-based Keurig Dr Pepper Inc. (KDP) owns, manufactures, and distributes beverages, as well as single-serve brewing systems. Valued at $45.9 billion by market cap, the company offers soft drinks, juices, teas, mixers, water, and other beverages.

Shares of this beverage giant have underperformed the broader market over the past year. KDP has declined 4.3% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 16.6%. In 2025, KDP stock is up 1.7%, compared to the SPX’s 7.8% rise on a YTD basis.

Zooming in further, KDP’s outperformance is apparent compared to the First Trust Nasdaq Food & Beverage ETF (FTXG). The exchange-traded fund has declined about 9.2% over the past year. Moreover, KDP’s gains on a YTD basis outshine the ETF’s 4.1% dip over the same time frame.

On Jul. 24, KDP shares closed up marginally after reporting its Q2 results. Its revenue stood at $4.2 billion, up 6.1% year over year. The company’s adjusted EPS increased 11.1% year over year to $0.49.

For the current fiscal year, ending in December, analysts expect KDP’s EPS to grow 6.8% to $2.05 on a diluted basis. The company’s earnings surprise history is impressive. It beat or matched the consensus estimate in each of the last four quarters.

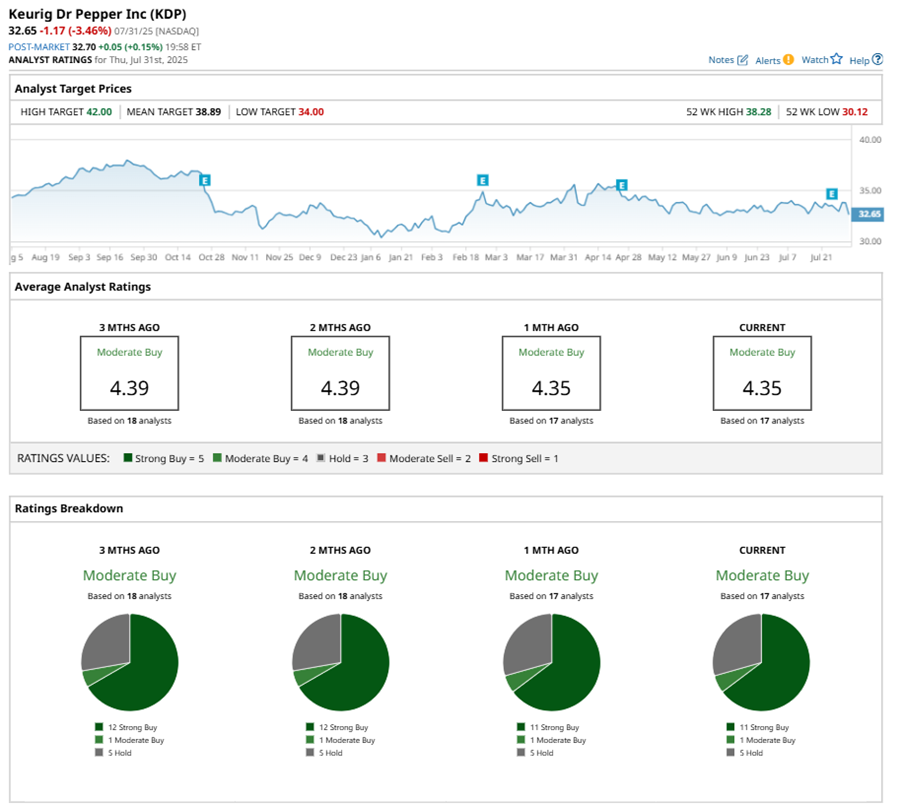

Among the 17 analysts covering KDP stock, the consensus is a “Moderate Buy.” That’s based on 11 “Strong Buy” ratings, one “Moderate Buy,” and five “Holds.”

This configuration is less bullish than two months ago, with 12 analysts suggesting a “Strong Buy.”

On Jul. 28, Barclays PLC (BCS) kept an “Overweight” rating on KDP and raised the price target to $39, implying a potential upside of 19.4% from current levels.

The mean price target of $38.89 represents a 19.1% premium to KDP’s current price levels. The Street-high price target of $42 suggests an upside potential of 28.6%.