Memory chips may not grab headlines the way AI models or iPhone launches do, but they sit at the center of both. As demand from data centers, smartphones, and other devices keeps building, pricing power in the memory market can shift quickly, creating big winners and losers for investors tracking the semiconductor cycle.

That is why Apple (AAPL) CEO Tim Cook’s latest warning matters. During Apple’s earnings call, Cook said memory costs are rising and expected them to have a bigger impact in the quarters ahead. For Apple, that is a margin headwind.

For Micron Technology (MU), it may be a sign that the memory market remains tight and that pricing conditions could stay favorable.

Micron has already been one of the market’s most closely watched AI-linked stocks, and Cook’s comments may add fresh fuel to that story. With demand still strong and memory prices climbing, Micron could remain one of the more interesting ways to play the semiconductor rebound.

Micron Is Becoming an AI Memory Powerhouse

Micron Technology has quietly become one of the hottest AI trades on the market.

The Idaho-based memory maker supplies the DRAM and NAND chips that power everything from smartphones to cloud data centers. Now, it is becoming an even bigger player in AI. The company recently started high-volume shipments of its HBM4 memory chips for Nvidia’s next-generation Vera Rubin platform, and management says its entire HBM capacity for 2026 is already sold out.

Micron has also been busy strengthening its financial position. In March, the company signed its first five-year Strategic Customer Agreement, a move designed to reduce the memory industry’s usual boom-and-bust cycles. It also launched a $5.4 billion debt buyback, cutting total debt significantly, while rewarding shareholders with a 30% dividend hike.

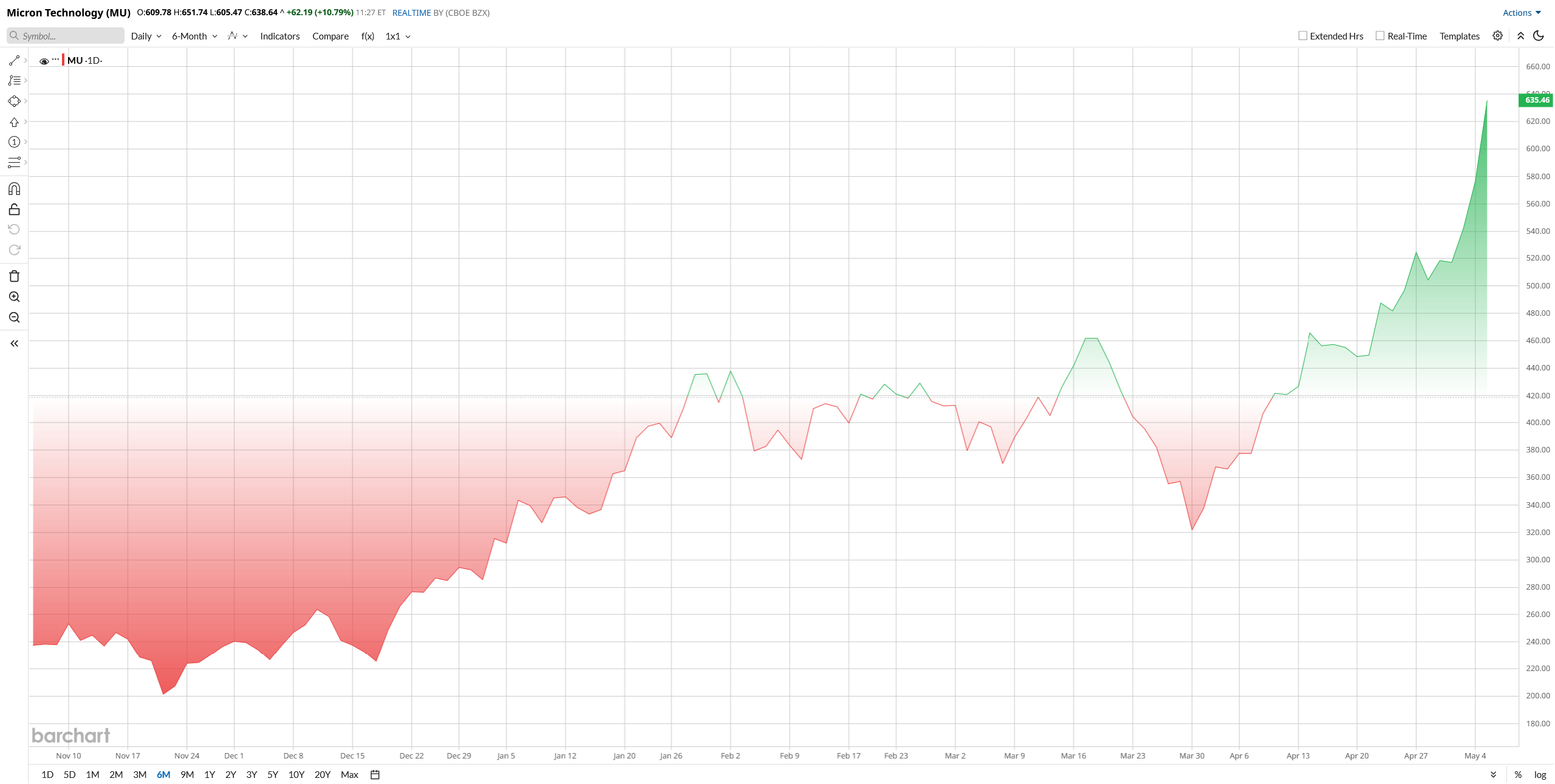

That momentum has fueled a massive rally. MU stock is up roughly 120% in 2026 and nearly 700% over the past year.

Still, not everything has been smooth. Shares pulled back after management revealed aggressive capital spending plans, with fiscal 2026 capex expected to top $25 billion. That revived old investor fears about oversupply.

Even after the rally, the valuation still looks compelling. Micron trades at just 8.4 times forward earnings, well below the semiconductor industry average of 24 times, suggesting the stock may still have room to run.

Tim Cook Just Lit the Fuse

On April 30, Cook told analysts that Apple expects “significantly higher memory costs” in the June quarter and beyond. He warned that these costs will “drive an increasing impact” on the business. Apple spent more on memory chips in March than in previous quarters and had to lean on stockpiled inventory to keep costs in check.

That well is now running dry. The market got the message loud and clear. Micron shares popped more than 4.8% on May 1 following Cook’s commentary, hitting a new 52-week high. When the world’s biggest hardware company tells you memory is getting pricier, memory stocks become the trade.

Record-breaking quarterly results

Micron’s fiscal second quarter, reported March 18, was nothing short of excellent. Revenue hit $23.86 billion, up 196% year-over-year (YoY) from $8.05 billion a year ago. That crushing number sailed past analyst estimates of around $19.2 billion. The company posted adjusted earnings per share of $12.20, a staggering 682% increase from the $1.56 reported in the same quarter last year. Wall Street had been looking for just $8.79.

Free cash flow also reached a quarterly record of $6.9 billion. The company ended the quarter sitting on $16.7 billion in cash and investments.

“Micron set new records across revenue, gross margin, EPS, and free cash flow in fiscal Q2, driven by a strong demand environment, tight industry supply, and our strong execution,” said CEO Sanjay Mehrotra.

Looking ahead, Micron guided for fiscal third quarter revenue of $33.5 billion, plus or minus $750 million. Adjusted EPS is expected to hit $19.15. Those numbers crushed consensus estimates of roughly $24.3 billion in revenue. Gross margins are projected to reach an eye-popping 81%

For the full fiscal year, analysts expect revenue around $35.6 billion and adjusted earnings per share near $57.71.

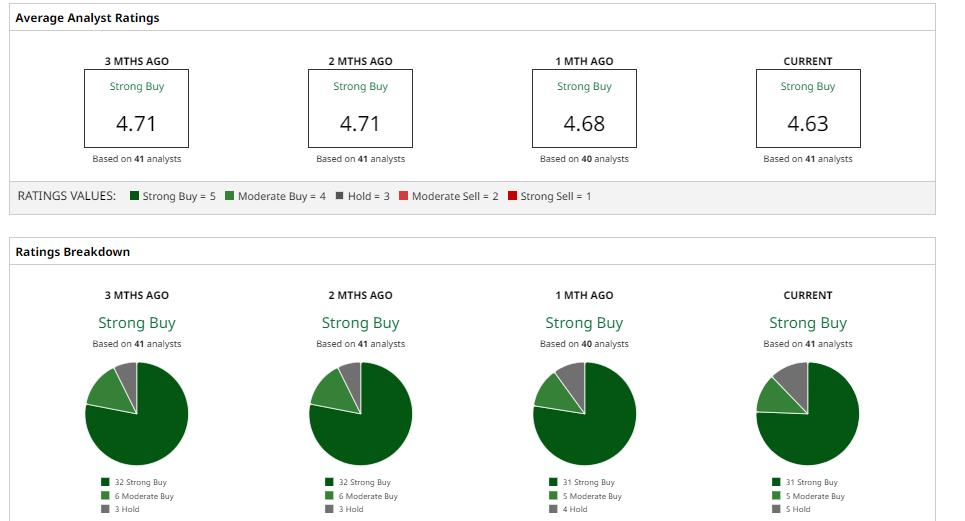

Wall Street is Extremely Bullish on MU Stock

Analysts have scrambled to raise targets after the blowout quarter.

DA Davidson initiated coverage on April 28 with a Street-high price target of $1,000 and a “Buy” rating. Analyst Gil Luria said artificial intelligence is “creating a longer-than-usual memory cycle” and argued the market underestimates how long this upcycle can run.

TD Cowen’s Krish Sankar, a top-ranked analyst, raised his target to $660 from $550, writing that the “next leg for the stock is more about durability than earnings upside.” UBS lifted its target to $535 from $510, pointing to long-term supply agreements that lock in demand and pricing.

According to Barchart data, Micron holds a consensus “Strong Buy” rating from 41 analysts. The average price target sits around $562, which MU stock has shot past after its monstrous run.