Odds are, the last time you went shopping online, you had the option to use a “buy now, pay later” (BNPL) app at checkout. Affirm, Afterpay, Klarna, Sezzle, and Zip are just a few of the companies that offer consumers a way to pay for their purchases through a series of fixed installments—without added interest.

According to the Federal Reserve Bank of New York, 20% of Americans surveyed used a BNPL app in the fourth quarter of 2023, and many did so to fund their holiday shopping. Klarna, Afterpay, and Zip all posted double-digit year-over-year usage increases, with $940 million in BNPL purchases taking place on Cyber Monday alone.

More and more consumers are turning to BNPL apps as a way to finance bigger-ticket purchases without adding debt to their credit cards—which, according to Experian, now carry an average balance of $6,501. This makes sense given the Fed’s current money-tightening stance, which has caused the average interest rate on credit cards (APR) to skyrocket to 28%, an all-time high. Retailers of all stripes are rolling out BNPL payment options to their customers, including big names like Amazon and Walmart; even credit card companies are now offering their own versions of BNPL, and the sky’s the limit on the kinds of items that you can purchase, including everything from fast food items to airline tickets.

So, what’s the catch? There is one. While the ease and convenience of “buying now, paying later” can’t be beat, if you’re not careful, missed or late payments could incur fees that add up to more than you’d pay if you had used a credit card in the first place. Plus, customers who default on certain types of BNPL payments could eventually be penalized with lower credit scores, so it’s worth understanding just what you’re getting into before you click “accept.”

B4LLS/Getty Images

What is “buy now, pay later?”

The concept of “buy now, pay later” is just like it sounds: Interest-free loans that are usually payable in four installments spread out every two weeks. These loans are typically offered to online shoppers as a payment option when they check out, but they are also available in stores.

For example, if you are making a $100 purchase, you could pay for the item (or items) in four installments of $25 with 0% interest.

According to the Federal Reserve, there are two types of BNPL users:

- People with low credit scores (620 or less) who have been denied a credit application in the past year. This group makes frequent, small purchases valued at $250 or less that they might not otherwise be able to afford.

- Financially stable users who use BNP on a sporadic basis on bigger-ticket items (between $1,750 and $2,000) in order to avoid paying interest.

Credit matters to both users, but in different ways. The “financially fragile” group chooses to “buy now, pay later” because they have little or no credit, while the financially stable group doesn’t want to incur the interest that comes with making a purchase on a credit card. For both groups, BNPL offers benefits.

Related: What does your credit score mean? Ranges, history & scoring criteria

How does “buy now, pay later” work?

To be eligible for a BNPL loan, you must fill out an application, including your name, email address, date of birth, and phone number. You also need to have a debit card, credit card, or bank account to make your online payments. In addition, you must be at least 18 years of age.

“Buy now, pay later” companies make money from the fees they charge—both to customers as well as the businesses they partner with. BNPL apps charge businesses setup fees and transaction fees. They also charge customers late fees and additional fees for missed payments, which we’ll get to next, since those can play a role in determining your credit score.

How do BNPL apps affect your credit score?

Some people think that just because BNPL apps don’t ask you to provide your Social Security number, your information won’t be shared with a credit agency—but that is not true.

BNPL companies often run a credit check on their customers, and depending on which type they conduct (especially if you take out a longer-term loan), they could report your payment history to a credit bureau, which could impact your credit score.

- A soft credit inquiry includes a review of your credit file and other limited information that does not affect your credit score.

- A hard credit inquiry, or a “hard pull,” is a request for your full credit report, which stays on your credit file for two years. This has a small (5-point) impact on your credit score. However, consumers with several hard inquiries over a short period are viewed by lenders as being credit risks, giving the impression that they are desperate for loans that they may not pay back.

In 2022, Forbes reported that the country’s three major credit reporting agencies, TransUnion, Equifax, and Experian, had incorporated BNPL data into consumer credit files, but this information had yet to be included in credit scoring models—but that’s most likely a matter of when, not if. Each tagged BNPL data separately from mortgage and credit card lending reports; Equifax said it has been conducting tests that will eventually allow lenders to receive this information as part of a consumer’s credit file.

BNPL users should note when their payments will be due; late fees on missed payments can range from a few dollars to up to 25% of the amount of the loan. And if you default on a loan and the balance is sent to collections, credit bureaus will be notified.

Need to return the item you purchased? If you used a BNPL app, things could get complicated. In a comprehensive report detailing the risks of BNPL, the Consumer Financial Protection Bureau said that 5% of BNPL consumers surveyed had difficulty obtaining a refund for an item they purchased or never received, because they couldn’t stop the payments.

How can you safely use a BNPL app?

The allure of using a “buy now, pay later app” is just how easy it is to finance whatever you want to buy. That makes it particularly easy to overspend, if you’re not careful. Stripe, the payment terminal company, reports that businesses who offer BNPL services enjoy an astounding 27% increase in sales volume.

So that’s why it’s worthwhile to reiterate a few best practices:

- Before you accept the terms of your BNPL loan, be sure to read the fine print. That way, you’ll know when your payments are due, the price you will need to pay, and what the penalties are.

- Try to pay off your BNPL loan in full as soon as you can.

- And, as always, don’t buy what you can’t afford.

What is the best BNPL app?

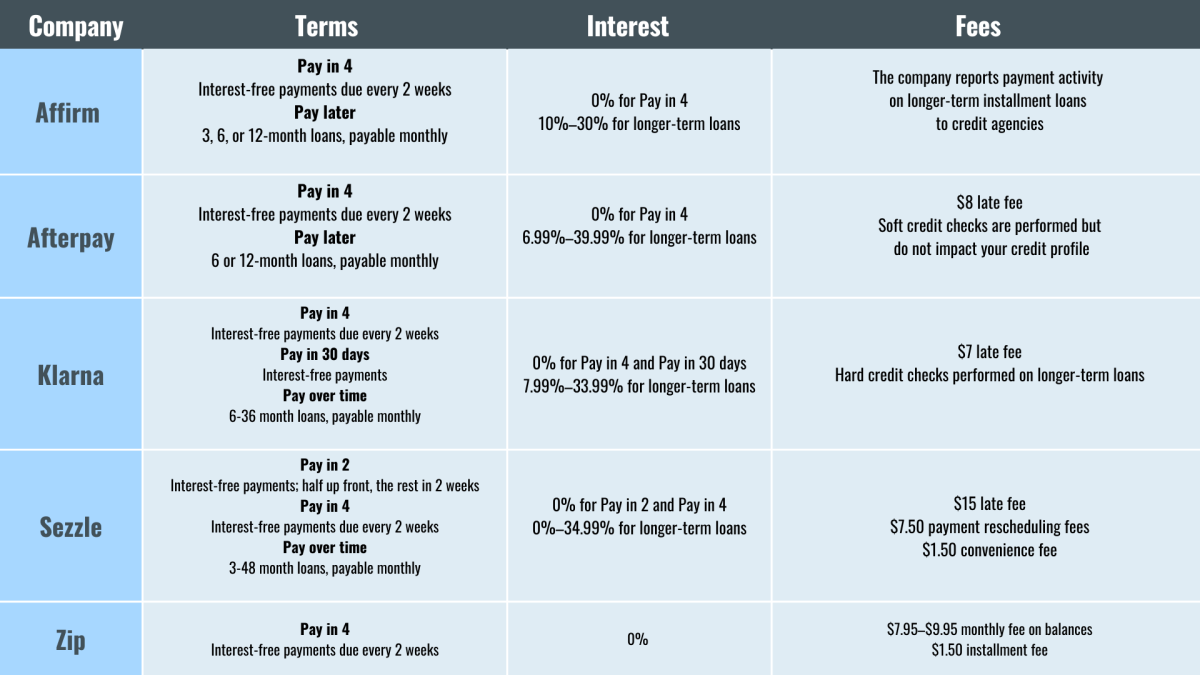

We’ve put together a handy chart so you can see how the BNPL apps stack up.

“Buy now, pay later” comparison chart

TheStreet