Google, a subsidiary of Alphabet (GOOG) (GOOGL), stands as one of the world’s most influential technology companies, driving innovation across search, digital advertising, cloud computing, and artificial intelligence (AI). The company has expanded far beyond its iconic search engine, generating the bulk of its revenue through digital ads while aggressively investing in AI and next-generation technologies.

Founded in 1998, the company operates globally, with offices in over 60 countries.

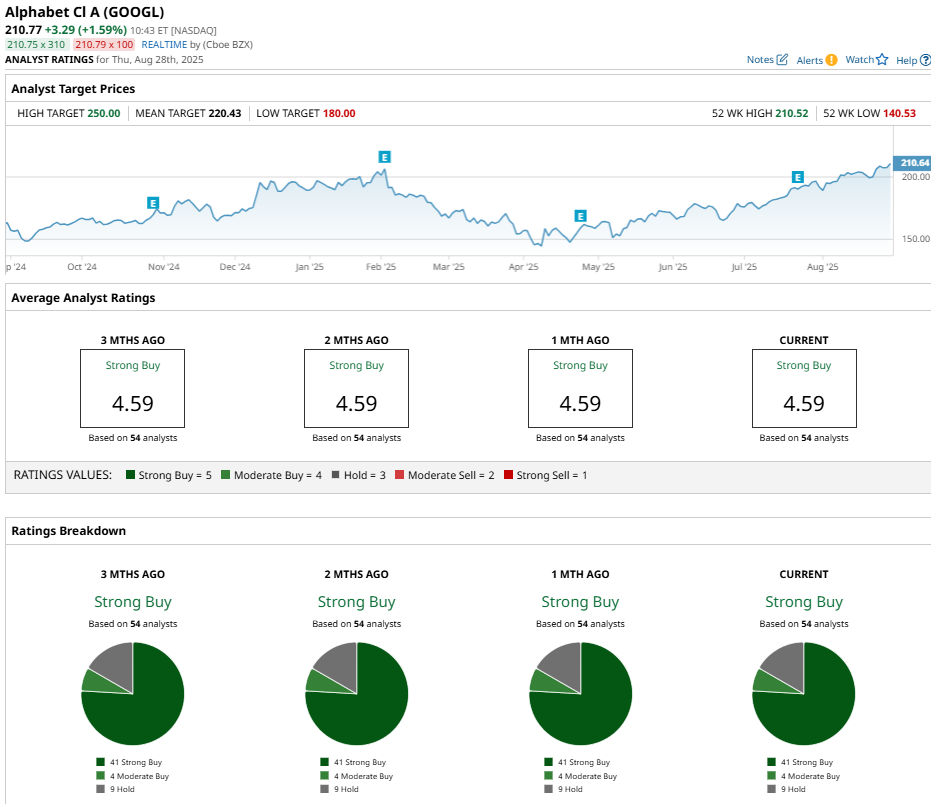

About GOOGL Stock

GOOGL stock has demonstrated strong performance recently. Over the past five days, the stock rose approximately 6%, while its one-month gain stands at nearly 10%. Over the past six months, the stock has gained 24%. When compared to the benchmark S&P 500 ($SPX), GOOGL has outperformed over the long term, delivering higher returns with a more volatile profile.

Google and Meta Join Hands

According to recent reporting, Meta Platforms (META) has entered into a major cloud computing agreement with Google Cloud, agreeing to invest over $10 billion over six years. This partnership is primarily focused on supporting Meta’s artificial intelligence ambitions by providing access to Google’s vast infrastructure, including servers, storage, networking, and specialized AI processors like Tensor Processing Units (TPUs) and GPUs.

Despite being competitors in digital advertising and other fields, Meta requires substantial cloud capacity to accelerate its AI projects, supplementing its own data centers with Google’s resources. Meta’s 2025 capital expenditure is expected to be between $114 billion and $118 billion, with significant investment directed toward AI development, including its Llama AI models.

This deal strengthens Google Cloud’s position in the cloud services market, helping it compete more effectively against leaders Amazon (AMZN) Web Services and Microsoft (MSFT) Azure. Google Cloud reported a 32% revenue growth in Q2 2025, outperforming overall company growth, and holds a growing backlog exceeding $100 billion. Meta’s strategy involves both building new AI-centric data centers and leveraging partnerships like this with Google, highlighting a trend where major tech rivals collaborate in cloud infrastructure to meet the massive demands of advanced AI technology

Google’s Solid Q2 Results

Alphabet, Google's parent company, reported strong Q2 2025 financial results, surpassing Wall Street expectations on both earnings and revenue. The company posted earnings per share of $2.31, ahead of the estimated $2.17, and revenue reached $96.4 billion, a 14% year-over-year (YoY) increase that exceeded the projected $93.9 billion. This robust growth was driven by its core advertising business, YouTube, and significant gains in the rapidly expanding Google Cloud and AI services.

Financially, Alphabet showed solid operating performance, with operating income rising 14% to $31.27 billion and maintaining a stable operating margin of 32.4%, similar to last year’s quarter. Google Cloud stood out with a 32% revenue increase to $13.6 billion and operating income more than doubling to $2.83 billion, reflecting improved scale and efficiency. Free cash flow was $5.3 billion despite higher capital expenditures, which surged 70% YoY to $22.45 billion, highlighting heavy investments in AI and cloud infrastructure. The company closed the quarter with approximately $95 billion in cash and marketable securities, underscoring its financial strength.

Looking ahead, Alphabet expressed confidence in continued growth driven by AI innovation, cloud expansion, and digital advertising resilience. The company raised its capital expenditure guidance to about $85 billion for 2025, signaling a commitment to long-term technology investment and market leadership.

Should You Buy Google?

Google’s recent six-year, $10 billion cloud deal with Meta is a strong vote of confidence in Alphabet’s cloud and AI capabilities. For investors, this strategic partnership highlights Google’s leadership in AI infrastructure, suggesting strong long-term growth potential.

As for analysts, the stock has a consensus “Strong Buy” rating with a mean price target of $220.43, reflecting an upside of 4.7% from the market rate. The stock has been studied by 54 analysts so far, receiving 41 “Strong Buy” ratings, four “Moderate Buy” ratings, and nine “Hold” ratings.