/Yum%20Brands%20Inc_%20sign%20by-%20JHVEPhoto%20via%20iStock.jpg)

Louisville, Kentucky-based Yum! Brands, Inc. (YUM) develops, operates, franchises, and licenses quick service restaurants. Valued at $40.3 billion by market cap, the company prepares, packages, and sells a menu of food items. The fast-food company is expected to announce its fiscal second-quarter earnings for 2025 before the market opens on Tuesday, Aug. 5.

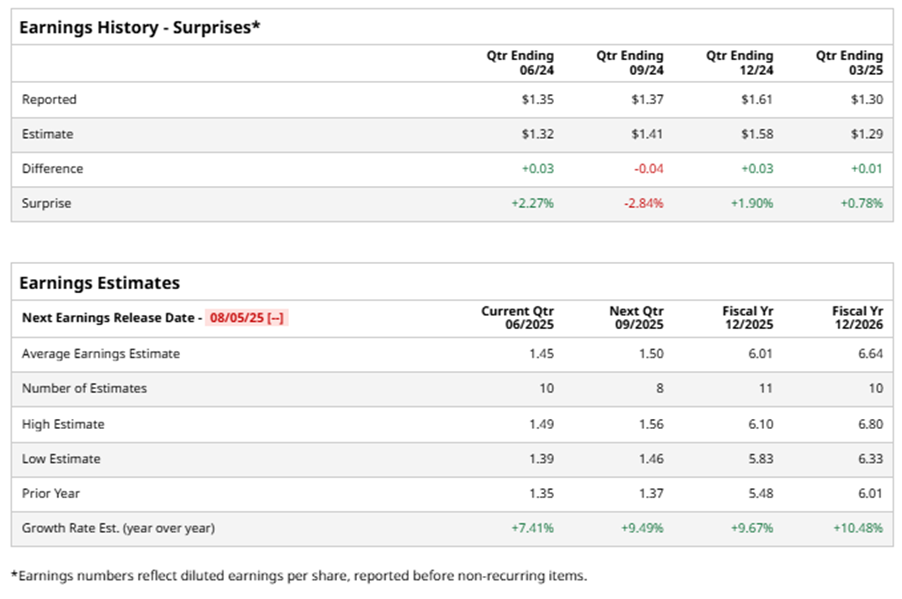

Ahead of the event, analysts expect YUM to report a profit of $1.45 per share on a diluted basis, up 7.4% from $1.35 per share in the year-ago quarter. The company surpassed the consensus estimates in three of the last four quarters while missing the forecast on another occasion.

For the full year, analysts expect YUM to report EPS of $6.01, up 9.7% from $5.48 in fiscal 2024. Its EPS is expected to rise 10.5% year-over-year to $6.64 in fiscal 2026.

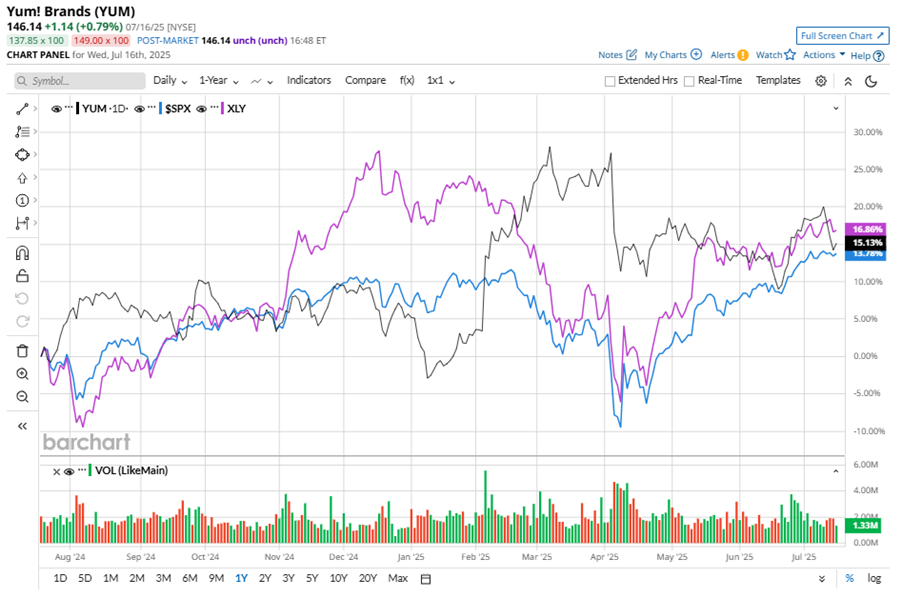

YUM stock has outperformed the S&P 500 Index’s ($SPX) 10.5% gains over the past 52 weeks, with shares up 13.4% during this period. Similarly, it outperformed the Consumer Discretionary Select Sector SPDR Fund’s (XLY) 12.7% gains over the same time frame.

YUM is outperforming due to strong menu pricing, average check growth, and an aggressive expansion strategy. The company is seeing success with strategic partnerships, digital transformation, and operational streamlining. Additionally, global development is progressing well, with a focus on key markets such as China and India. Comps' growth is strong, fueled by international markets and localized innovation. YUM aims to continue driving growth through market penetration and expanded offerings in 2025.

On Apr. 30, YUM shares closed up more than 1% after reporting its Q1 results. Its adjusted EPS of $1.30 surpassed Wall Street expectations of $1.29. The company’s revenue was $1.79 billion, falling short of Wall Street forecasts of $1.84 billion.

Analysts’ consensus opinion on YUM stock is reasonably bullish, with an overall “Moderate Buy” rating. Out of 27 analysts covering the stock, nine advise a “Strong Buy” rating, and 18 give a “Hold.” YUM’s average analyst price target is $162.04, indicating a potential upside of 10.9% from the current levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.