If you want to retire with minimum money worries, you have a few options: Marry really well, pick the Powerball along with the other winning lottery numbers or consider a personalized retirement plan that produces high levels of income while maintaining and growing liquid savings late into retirement.

Most retirees need to solve for a couple of problems. They want lifetime income to cover their budget, including the occasional splurge, and a way to pay for the real likelihood of long-term care, which 70% of us will face. We’ll cover that in more detail below.

The Kiplinger Building Wealth program handpicks financial advisers and business owners from around the world to share retirement, estate planning and tax strategies to preserve and grow your wealth. These experts, who never pay for inclusion on the site, include professional wealth managers, fiduciary financial planners, CPAs and lawyers. Most of them have certifications including CFP®, ChFC®, IAR, AIF®, CDFA® and more, and their stellar records can be checked through the SEC or FINRA.

A plan that addresses both income and savings

I wrote about how that personalized IRA4Income plan I mentioned above works, in my article What If You Could Increase Your Retirement Income by 50% to 75%?, and here’s a quick description:

IRA4Income is a multi-asset class retirement plan that addresses both income and savings. It will smooth out the effects of market gyrations and unplanned expenses, but for this article, let’s focus on long-term care expense.

Using our Go2Income planning technology, we’ve put the following assets together into IRA4Income:

- An IRA account invested 50/50 in fixed income and stock investments

- Lifetime income annuities with income starting immediately or in the future

- A home equity conversion mortgage (HECM) that generates income and liquidity

This will become important when we need to cover LTC expenses.

How big of an issue is long-term care?

More than two-thirds of retirees will incur an event requiring some form of long-term care.

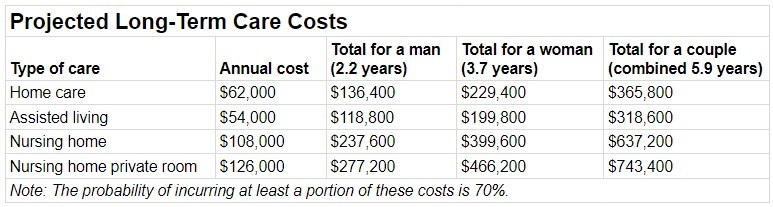

Here are the median annual costs in 2025, depending on the type of care, according to CareScout and Genworth:

- Home health aide (44 hours a week): $80,000

- Assisted living facility: $73,000

- Semiprivate nursing home: $115,000

- Private room in a nursing home: $132,000

These costs will vary considerably by region. Here’s a projection of average costs considering the duration of a stay for a man, a woman and a couple.

For the purposes of the analysis below, we’ll assume $100,000 per year for five years, for a total of $500,000.

How does a retiree address this challenge?

Long-term care insurance is one solution. However, many don’t qualify or balk at the annual cost, which averages $2,000 to $4,500 per person and usually increases every year.

There often are sizable deductibles, and premium rates are not guaranteed.

Despite these issues, it is worth considering, particularly if you can cover a large portion of the event (deductibles) with your liquid savings.

Another possible solution is to use your liquid retirement savings exclusively, provided it doesn’t have an adverse impact on your retirement income. That’s where IRA4Income comes in.

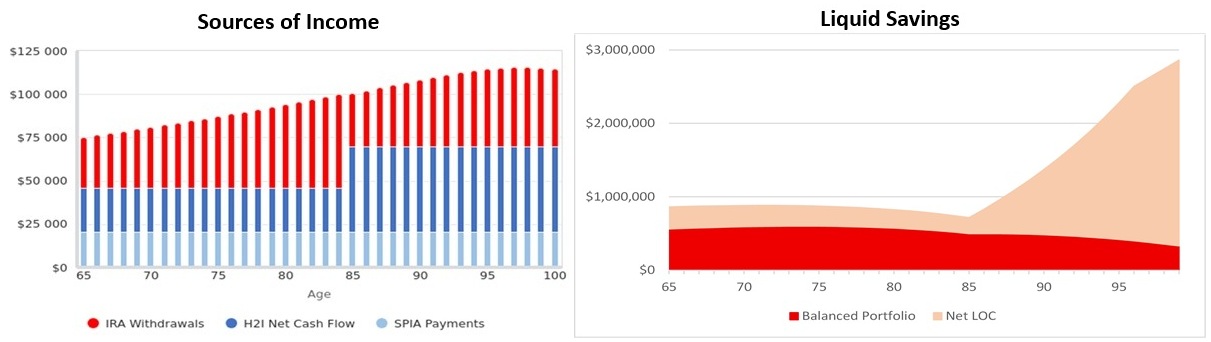

For a sample male retiree, age 65, with $1 million in IRA savings and $1 million in the value of his house, here are the income and liquid savings with no adjustment for LTC costs.

Looks pretty good. However, that $500,000 event could come at any time.

How to build a self-insured plan

We’ll assume in this example that our retiree doesn’t have LTC insurance. (According to KFF, only 14% of people who are 65 and older do.) So, let’s build a self-insured plan around IRA4Income as follows.

- Set aside a portion of higher income from IRA4Income each year into a new investment account with low income taxes. In our retiree’s case, he’ll take $5,000 per year out of his $75,000 (and growing) income each year.

- When LTC costs appear, withdraw funds from the IRA account first. Since the bulk of the LTC expenses are tax-deductible in his situation, he’s not incurring a large tax bite on these withdrawals.

- Take a portion of the costs out of the new investment account and avoid drawing down on the HECM net line of credit, therefore preserving the highest value of his house to pass to his kids.

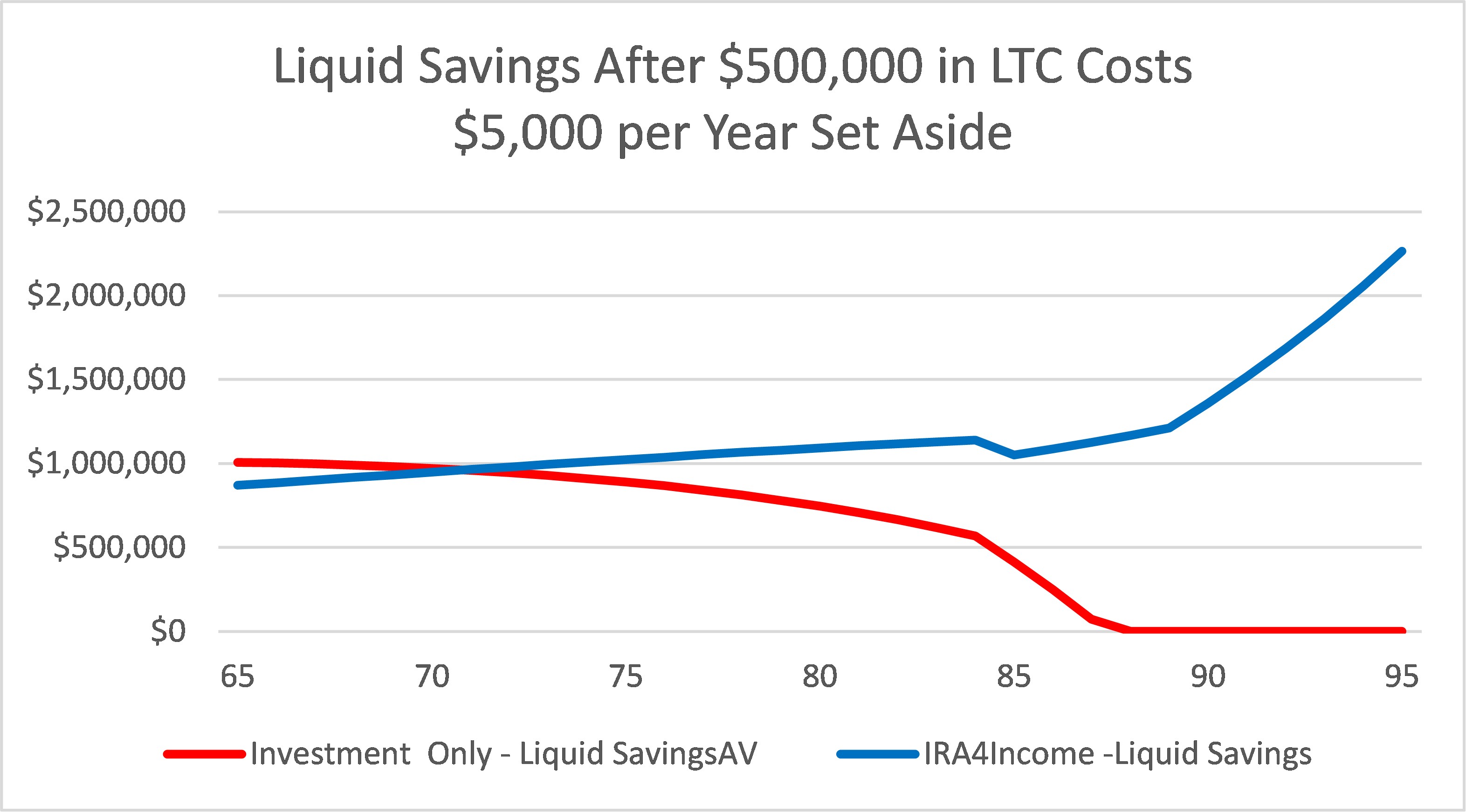

Now compare this to building a plan with only an IRA account, allocated solely to investments. Here’s what the savings under these two strategies look like.

In this scenario, the savings run out under the IRA-only strategy, and our retiree will have to sell his house or spend down the assets to qualify for Medicaid to pay for his long-term care.

Looking for expert tips to grow and preserve your wealth? Sign up for Building Wealth, our free, twice-weekly newsletter.

How to get started

Here’s a list:

- Check out LTC insurance. The earlier you buy it, the lower the premiums, although the insurance companies are allowed to increase premiums every year. An IRA4Income plan, with its higher income and savings, means your policy can have a large deductible.

- Get an estimate of costs in your region. The cost of services varies significantly, with the Northeast and West Coast being the most expensive. Insurers price policies based partly on expected future claims, so regions with higher caregiving costs lead to higher premiums.

- When building your own IRA4Income approach, request a plan that considers LTC costs. You can decide which options work best for you and make further adjustments until you have a plan that fits the needs of you and your family.

- Make sure your plans are communicated to family members or an adviser.

If you’re ready to consider an IRA4Income plan, visit Go2Income and create your own plan.

Related Content

- What if You Could Increase Your Retirement Income by 50% to 75%? Here's How

- What the HECM? Combine It With a QLAC and See What Happens

- Transform Your Retirement Plan With This Powerful Combo

- How Combining Your Home Equity and IRA Can Supercharge Your Retirement

- How Your Home Can Fill Gaps in Your Retirement Plan

This article was written by and presents the views of our contributing adviser, not the Kiplinger editorial staff. You can check adviser records with the SEC or with FINRA.