/The%20sign%20for%20Marvell%20Technology%20out%20front%20of%20a%20corporate%20office%20by%20Valeriya%20Zankovych%20via%20Shutterstock.jpg)

Marvell Technology (MRVL) will release its second-quarter fiscal 2026 financial results on Thursday, Aug. 28. After dropping significantly from its 52-week high of $127.48, shares of this semiconductor giant have staged a comeback, rising 17.4% in three months. That rebound reflects growing optimism around Marvell’s positioning in the artificial intelligence (AI) space.

Marvell is seeing robust AI-driven demand from the data center end markets, which could boost its financials and share price. On the technical side, the stock may still have room to climb. Its 14-day Relative Strength Index currently sits at 50.30, a level that suggests shares are not overbought. For investors, that signals the recent rally may not be running out of steam just yet.

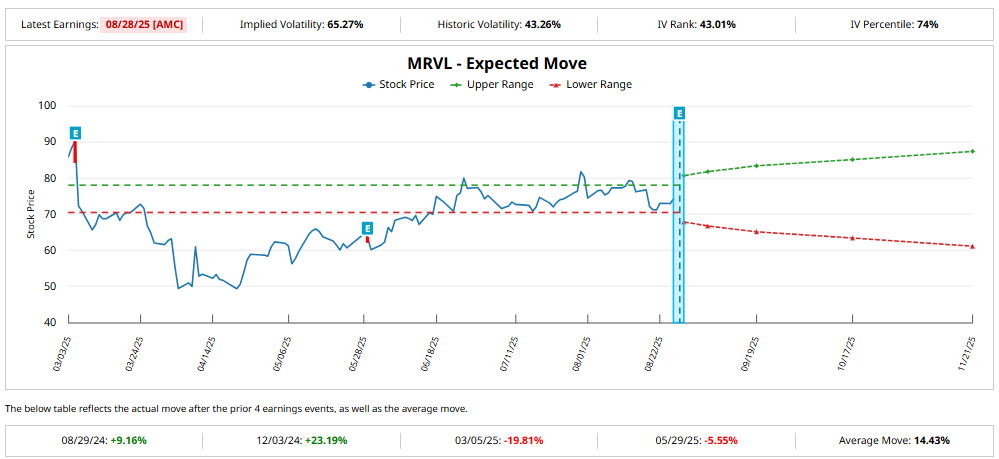

However, broader macroeconomic uncertainty could spark volatility, and the options market is factoring that in. Contracts are pricing in an earnings-day swing of about 8.5% in either direction. While that’s below Marvell’s average move of 14.4% following earnings over the past year, the history is mixed. Shares have fallen after two of the last four reports, implying that even solid numbers may not guarantee a positive reaction.

With this background, let’s take a look at Q2 expectations.

Marvell Could Deliver Strong AI-Powered Revenue

Following a strong start to fiscal 2026, Marvell appears well-positioned to sustain this momentum into the second quarter, with AI demand continuing to drive growth.

Management has guided for revenue of around $2 billion at the midpoint for Q2, marking a 57% year-over-year increase. Much of this growth is driven by Marvell’s data center end market, which generated $1.44 billion in revenue during Q1, representing a 76% increase from the prior year and a 5% sequential increase. That strength is expected to carry forward, with sequential growth projected to continue at a mid-single-digit pace in Q2, while maintaining a robust annual expansion.

The foundation of this growth lies in Marvell’s custom AI silicon programs, which are scaling into high-volume production, alongside strong shipments of its electro-optics products for AI and cloud workloads. At the same time, the company is advancing its technology platform to support full rack-level custom infrastructure, integrating high-bandwidth memory (HBM) and co-packaged optics, which could significantly improve efficiency and performance for AI compute systems and drive its financials.

Marvell is pushing forward with co-packaged optics, which can replace copper interconnects with optical fiber to scale up AI clusters. This transition increases system capacity and speed and opens the door to new revenue opportunities in interconnect technology.

Outside of the data center, Marvell is also seeing recovery across enterprise networking and carrier infrastructure end markets, both of which are expected to post sequential growth again in Q2. Even its consumer segment, which fell sharply in Q1, is forecast to rebound by roughly 50% in Q2 thanks to seasonal trends and gaming-related demand.

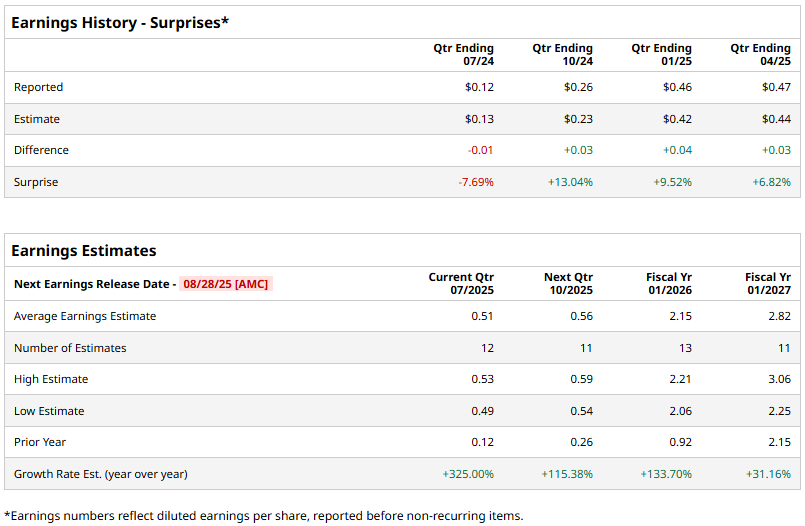

With these tailwinds, Marvell’s earnings outlook remains solid. Management projects Q2 earnings per share in the range of $0.62 to $0.72, more than double the $0.30 reported in the same quarter a year ago. Analysts, however, are more conservative, with a consensus at $0.51 per share. Notably, Marvell has topped Wall Street expectations in three of the past four quarters, most recently beating by 6.8%, suggesting upside surprise remains possible.

Is MRVL Stock a Buy, Sell, or Hold?

Marvell Technology enters its Q2 earnings with strong momentum, driven by surging demand for AI-driven solutions and a broad-based recovery across its end markets. While macroeconomic uncertainty and mixed earnings-day reactions in the past suggest that volatility is still a risk, the company’s expanding footprint in custom AI silicon, electro-optics, and co-packaged optics provides a compelling long-term growth narrative. With revenue expected to surge and earnings projected to more than double year-over-year, Marvell appears well-positioned to deliver another solid quarter, making it a buy.

Analysts are also upbeat about MRVL stock ahead of earnings and maintain a “Strong Buy” consensus rating.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.