Indianapolis, Indiana-based Simon Property Group, Inc. (SPG) is a self-administered and self-managed real estate investment trust (REIT). Valued at $58.8 billion by market cap, the company owns, develops, and manages retail real estate properties, including regional malls, outlet centers, community/lifestyle centers, and international properties. The real estate giant is expected to announce its fiscal third-quarter earnings for 2025 after the market closes on Monday, Nov. 3.

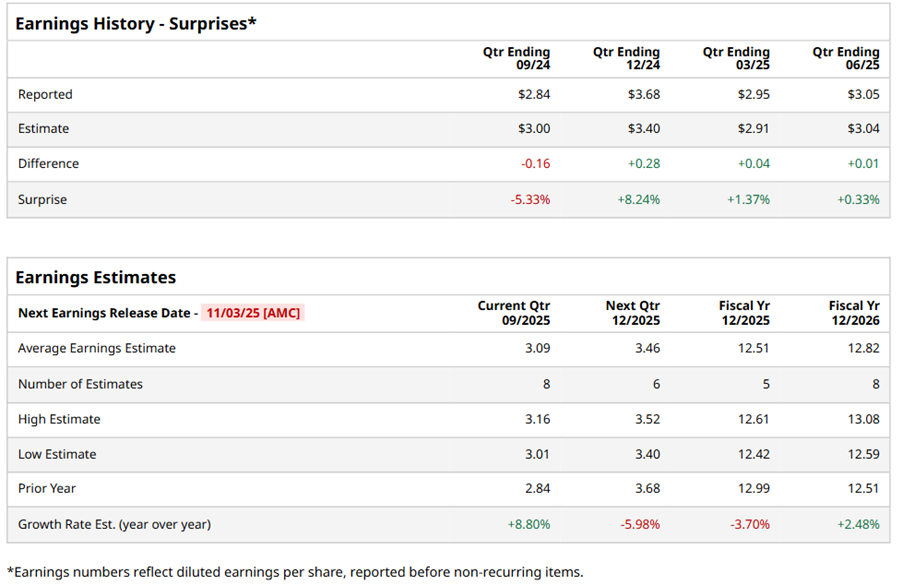

Ahead of the event, analysts expect SPG to report an FFO of $3.09 per share on a diluted basis, up 8.8% from $2.84 per share in the year-ago quarter. The company surpassed the consensus estimates in three of the last four quarters while missing the forecast on another occasion.

For the full year, analysts expect SPG to report FFO of $12.51 per share, down 3.7% from $12.99 per share in fiscal 2024. However, its FFO is expected to rise 2.5% year over year to $12.82 per share in fiscal 2026.

SPG stock has underperformed the S&P 500 Index’s ($SPX) 14.5% gains over the past 52 weeks, with shares up 2.9% during this period. However, it outperformed the Real Estate Select Sector SPDR Fund’s (XLRE) 3.9% losses over the same time frame.

On Aug. 4, SPG shares closed up more than 2% after reporting its Q2 results. Its FFO of $3.05 per share surpassed Wall Street forecasts of $3.04 per share. The company’s revenue was $1.50 billion, falling short of Wall Street forecasts of $1.51 billion. Simon Property expects full-year FFO in the range of $12.45 to $12.65 per share.

Analysts’ consensus opinion on SPG stock is reasonably bullish, with a “Moderate Buy” rating overall. Out of 21 analysts covering the stock, eight advise a “Strong Buy” rating, and 13 give a “Hold.” SPG’s average analyst price target is $188.45, indicating a potential upside of 4.7% from the current levels.