Glendale, California-based Public Storage (PSA) is a REIT that primarily acquires, develops, owns, and operates self-storage facilities. Valued at $50.9 billion by market cap, the company owned and/or operated 3,399 self-storage facilities located in 40 states with approximately 247 million net rentable square feet in the U.S. The self-storage giant is expected to announce its fiscal first-quarter earnings for 2026 in the near term.

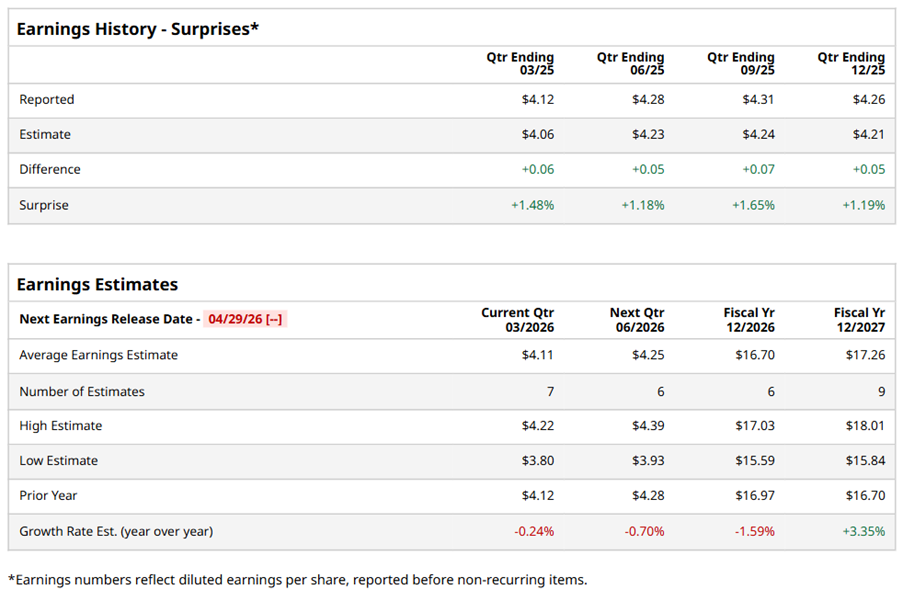

Ahead of the event, analysts expect PSA to report an FFO of $4.11 per share on a diluted basis, down marginally from $4.12 per share in the year-ago quarter. The company has consistently surpassed Wall Street’s FFO estimates in its last four quarterly reports.

For the full year, analysts expect PSA to report FFO per share of $16.70, down 1.6% from $16.97 in fiscal 2025. However, its FFO is expected to rise 3.4% year over year to $17.26 per share in fiscal 2027.

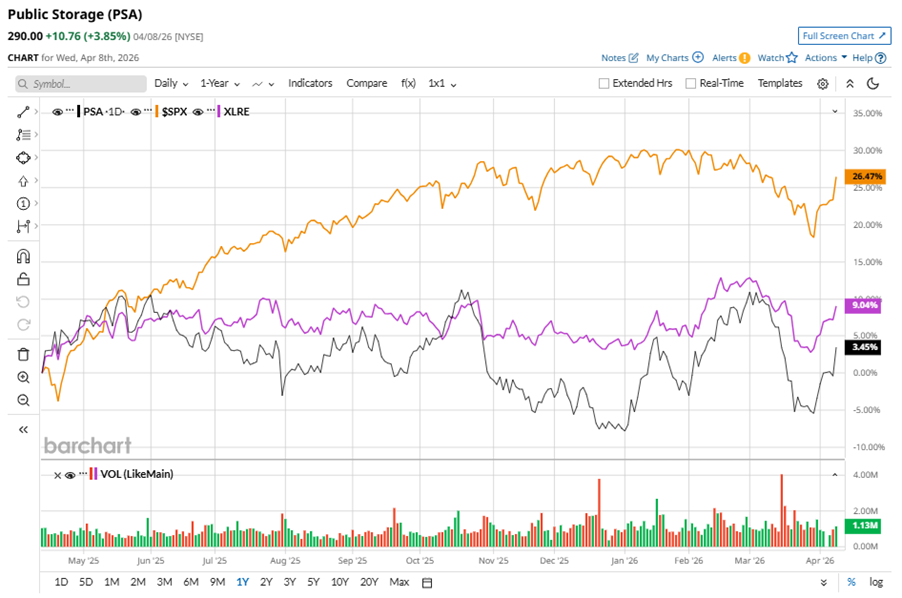

PSA stock has underperformed the S&P 500 Index’s ($SPX) 36.1% gains over the past 52 weeks, with shares up 8.9% during this period. Similarly, it underperformed the State Street Real Estate Select Sector SPDR ETF’s (XLRE) 14.5% uptick over the same time frame.

On Feb. 12, PSA reported its Q4 results, and its shares closed up by 2.7% in the following trading session. Its FFO of $4.26 per share exceeded Wall Street expectations of $4.21 per share. The company’s revenue was $1.22 billion, topping Wall Street forecasts of $1.21 billion. PSA expects full-year FFO in the range of $16.35 to $17 per share.

Analysts’ consensus opinion on PSA stock is reasonably bullish, with a “Moderate Buy” rating overall. Out of 19 analysts covering the stock, seven advise a “Strong Buy” rating, and 12 give a “Hold.” PSA’s average analyst price target is $312.07, indicating a potential upside of 7.6% from the current levels.