With a market cap of $12.5 billion, Pinnacle West Capital Corporation (PNW) provides retail and wholesale electricity services across Arizona through its subsidiary operations. It generates and delivers power using a diverse mix of sources including nuclear, gas, oil, coal, and solar, while maintaining extensive transmission, distribution, and energy storage infrastructure.

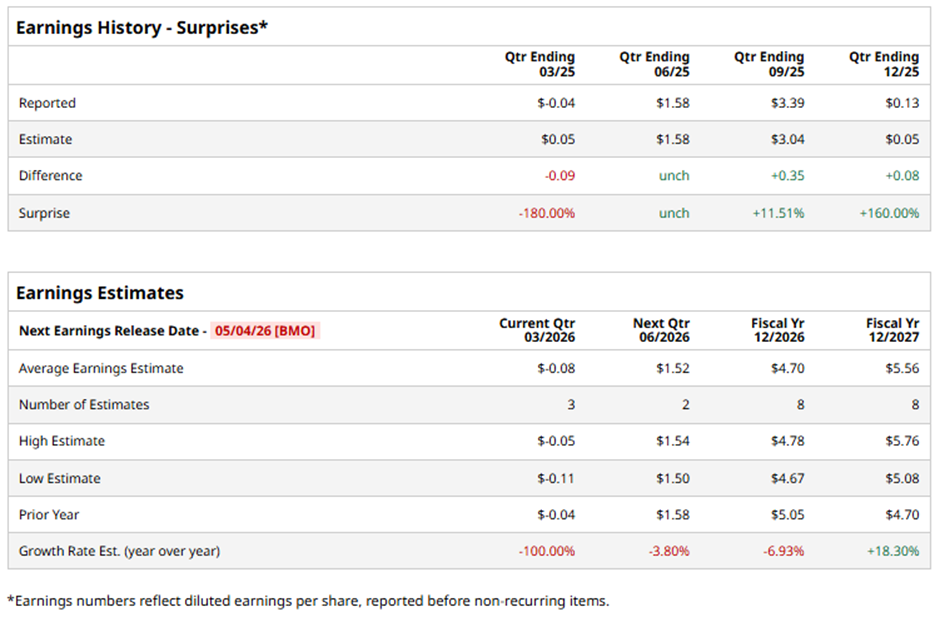

The Phoenix, Arizona-based company is expected to unveil its fiscal Q1 2026 results before the market opens on Monday, May 4. Ahead of the event, analysts anticipate PNW to report a loss of $0.08 per share, a decrease of 100% from a loss of $0.04 per share in the year-ago quarter. It has exceeded or met Wall Street's bottom-line estimates in three of the past four quarters while missing on another occasion.

For fiscal 2026, analysts predict Pinnacle West Capital to report EPS of $4.70, a decline of 6.9% from $5.05 in fiscal 2025. However, EPS is projected to increase 18.3% year-over-year to $5.56 in fiscal 2027.

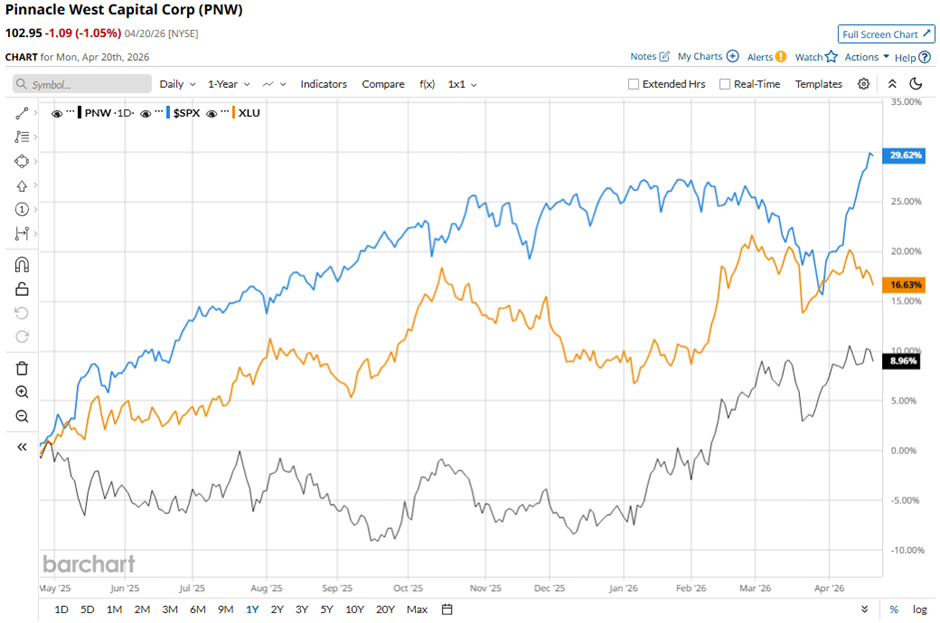

PNW stock has risen 9% over the past 52 weeks, lagging behind the S&P 500 Index's ($SPX) 34.6% gain and the State Street Utilities Select Sector SPDR ETF's (XLU) 17.7% return over the same period.

Pinnacle West Capital reported solid 2025 results on Feb. 25, including full-year net income of $616.5 million, up from $608.8 million in 2024, driven by customer growth, higher electricity usage, and increased transmission revenues. Investor sentiment was further boosted by strong operational trends, including 2.4% customer growth, 5% retail electricity sales growth, and peak demand rising over 5%. Additionally, the company’s 2026 EPS guidance of $4.55 - $4.75 and expectations of 5% - 7% annual sales growth over the next five years reinforced confidence.

Nevertheless, the stock fell marginally on that day, likely due to concerns about EPS declining year-over-year from $5.24 in 2024 to $5.05 in 2025 and ongoing pressure from higher interest, pension, and operating expenses.

Analysts' consensus rating on PNW stock is cautiously optimistic, with a "Moderate Buy" rating overall. Out of 17 analysts covering the stock, opinions include four "Strong Buys" and 13 "Holds." The average analyst price target for Pinnacle West Capital is $104.14, indicating a potential upside of 1.2% from the current levels.