The Tax Cuts and Jobs Act of 2017 resulted in lower tax rates for Americans. The act is scheduled to expire at the end of 2025 — and when it does, tax rates will revert to 2017 levels unless Congress takes action before then.

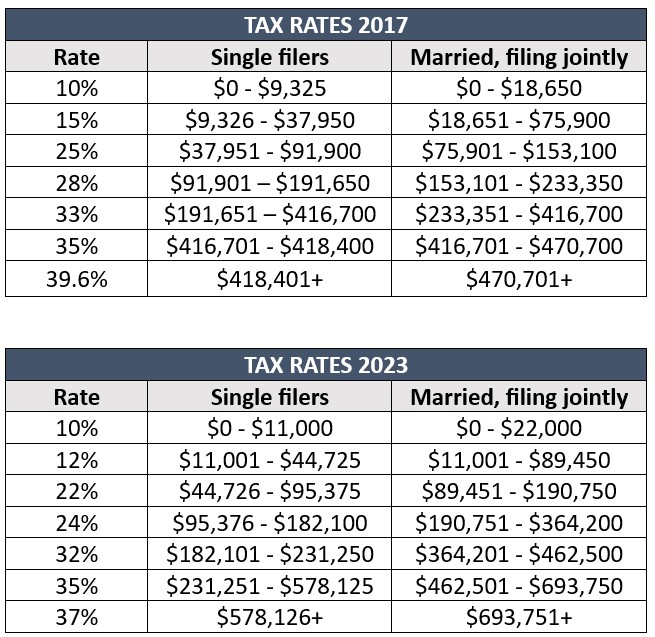

The TCJA's sunset means the majority of Americans will see an increase in how much they owe in taxes. Take a look at how income tax brackets and rates compared in 2017 and 2023:

As you can see, if you are in the 12% bracket in 2023, you would fall into the 15% bracket with the same income once the TCJA expires. If you’re currently in the 22% bracket, you will move to the 25% bracket in 2026. And if you fall in the 24% bracket in 2023, you could jump to the 28% bracket when rates increase.

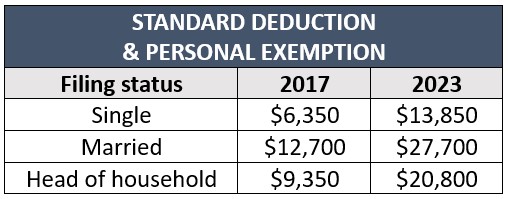

Many Americans also benefited from an increase in the standard deduction amount, which doubled following the TCJA. Here’s how standard deductions and personal exemptions changed from 2017 to 2023:

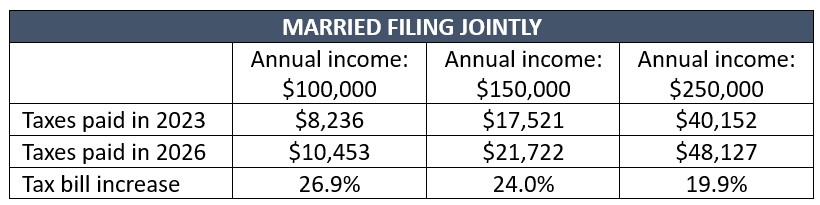

The higher tax rates and expanded tax brackets plus a lower standard deduction mean many Americans could end up paying about 20% more in taxes when the TCJA expires. Here’s a breakdown of a real-life example of how much more one couple might end up paying in 2026 vs 2023:

I like to think of our current low-tax-rate environment as a “tax sale.” Just as we would stock up on items at the grocery store during a big sale, most of us would benefit from paying taxes now, rather than waiting until rates go up. If we don’t do it now, we may be forced to pay higher rates on distributions from tax-deferred investments like 401(k)s and IRAs in retirement.

We can take advantage of lower rates by implementing proactive tax planning strategies and be what I call “tax smart.” One way to do this is through a Roth IRA conversion, where money from tax-deferred accounts is moved to a Roth IRA account. You will pay taxes on the amount converted now, but you won’t pay taxes on withdrawals made later. This strategy could result in more money to live on in retirement.

At our firm, we’ve used this strategy with many of our clients, who often ask us, “Why didn’t my previous financial planner suggest a Roth IRA conversion earlier?” My answer is that many financial planners don’t specialize in tax planning. Instead, most focus only on investment management and not the other four pillars of a complete financial plan: taxes, estate planning, health care and income. I encourage you to find a team of financial planners who specialize in all five pillars to ensure you are getting the financial plan you deserve.

Interested in more information on the TCJA expiration or other tax planning strategies? Read my book, I Hate Taxes: Lower Your Taxes, Own Your Retirement, to learn more.

The appearances in Kiplinger were obtained through a public relations program. The columnist received assistance from a public relations firm in preparing this piece for submission to Kiplinger.com. Kiplinger was not compensated in any way.