/Parker-Hannifin%20Corp_%20factory-by%20Jonathan%20Weiss%20via%20Shutterstock.jpg)

Cleveland, Ohio-based Parker-Hannifin Corporation (PH) manufactures and sells motion and control technologies and systems for aerospace and defense, in-plant and industrial equipment, transportation, off-highway, energy, and HVAC and refrigeration markets in North America and internationally. The company has a market cap of $124.8 billion and is expected to release its Q3 2026 earnings on Thursday, Apr. 30, before the market opens.

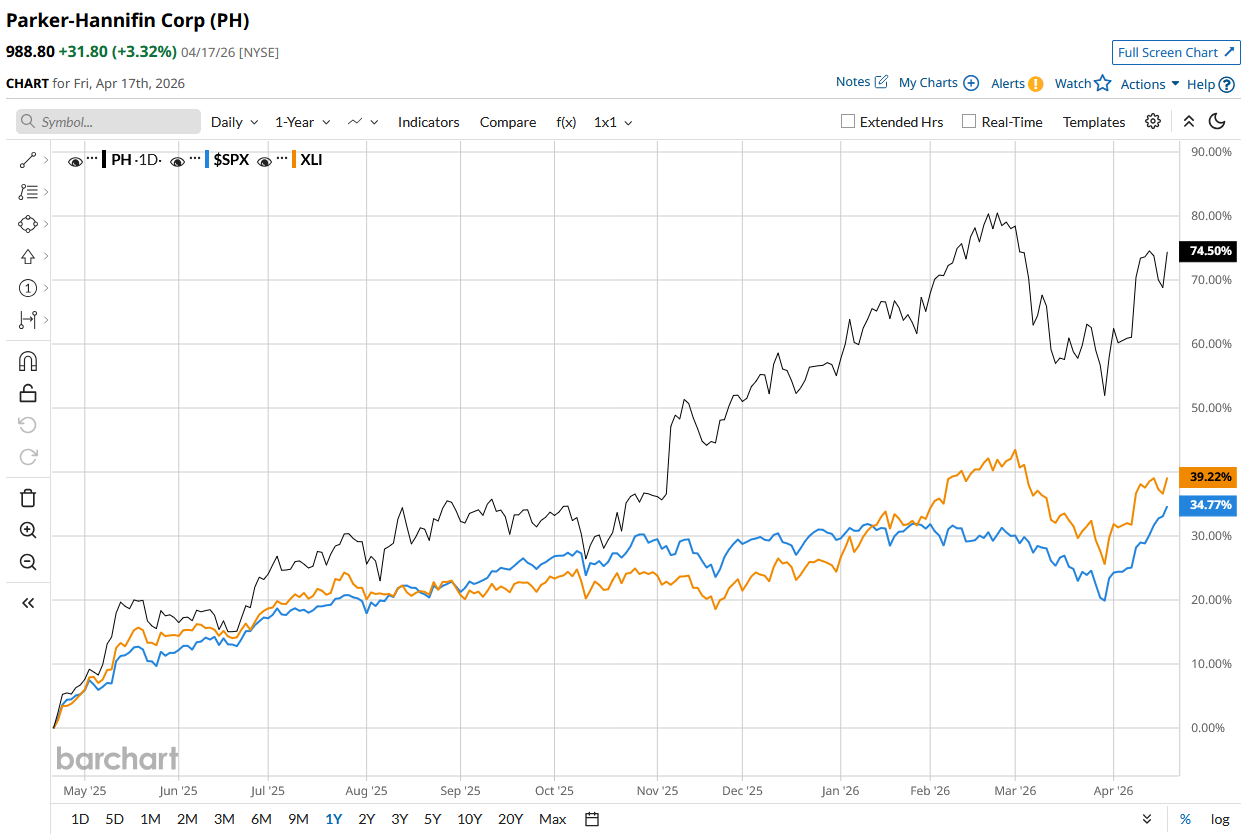

Ahead of the event, analysts expect the company’s EPS to be $7.81 on a diluted basis, up 12.5% from $6.94 in the year-ago quarter. The company has exceeded Wall Street’s EPS estimates in all of its last four quarters.

For fiscal 2026, analysts project the company’s EPS to be $30.99, up 13.4% from $27.33 in fiscal 2025. Moreover, its EPS is expected to rise by roughly 10.1% year over year (YoY) to $34.12 in fiscal 2027.

PH’s stock has surged 76.3% over the past 52 weeks, outperforming the S&P 500 Index’s ($SPX) 34.9% rise and the State Street Industrials Select Sector SPDR ETF’s (XLI) 38.5% return during the same time frame.

On Jan. 29, PH stock rose 3.5% following the release of its better-than-expected Q2 2026 earnings. The company’s sales rose 9% from the prior year’s quarter to $5.2 billion, surpassing the Street’s estimates. Moreover, its adjusted EPS for the quarter amounted to $7.76, coming in on top of Wall Street estimates. PH also increased its guidance for its full-year sales growth, which is expected to be in the range of 5.5% to 7.5%. Additionally, the company also expects its EPS to be in the range of $26.26 to $26.86 for the full year.

Analysts are highly bullish on PH, with the stock having a “Strong Buy” rating overall. Among the 25 analysts covering the stock, 18 are recommending a “Strong Buy,” one recommends a “Moderate Buy,” and six suggest a “Hold” for the stock. PH’s average analyst price target is $1,037.09, indicating an upside of 4.9% from the current levels.