/Cooper%20Companies%2C%20Inc_%20phone%20and%20site-by%20T_Schneider%20via%20Shutterstock.jpg)

The Cooper Companies, Inc. (COO) is a global medical device company focused on vision care and women’s health. Through its CooperVision and CooperSurgical businesses, it develops products that support eye health and reproductive care. The company is headquartered in San Ramon, California, and serves healthcare professionals and patients around the world. It has a market capitalization of $12.20 billion.

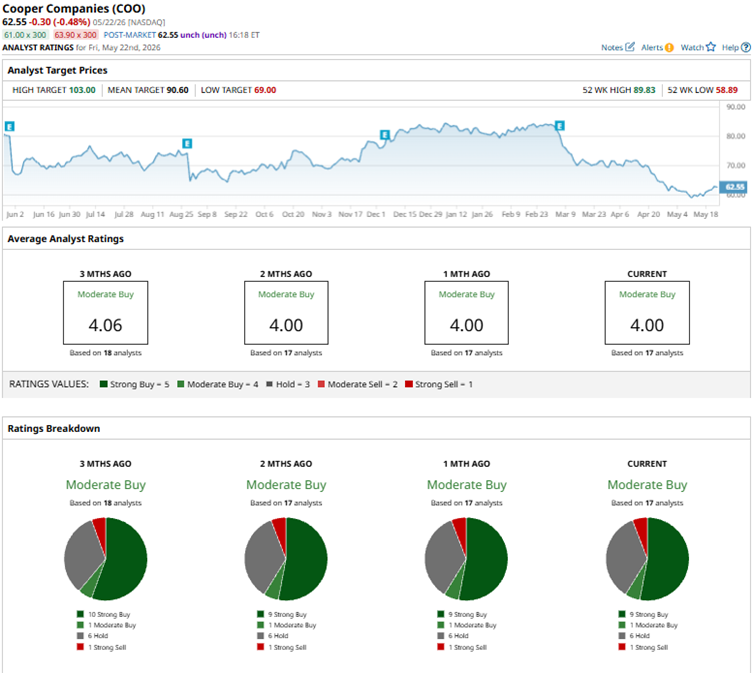

Cooper Companies’ stock performance has been weak due to slower organic growth, especially in the contact lens business, and concerns about performance in the Asia-Pacific. Over the past 52 weeks, the stock has declined 21.1%, and it is down 23.7% year-to-date (YTD). COO’s shares reached a 52-week low of $58.89 on May 12, but are up 6.2% from that level.

The S&P 500 index ($SPX) is up 27.9% over the past 52 weeks and is up 9.2% YTD. Therefore, the stock has underperformed the broader market over these periods. Compared with Cooper Companies’ own sector, we also observe underperformance. The State Street Health Care Select Sector SPDR ETF (XLV) has increased 14.8% over the past 52 weeks, while it has dropped 3.2% YTD.

For the first quarter of fiscal 2026 (quarter ended Jan. 31), Cooper Companies’ revenue increased 8% year-over-year (YOY), or 3% organically, to $695.10 million. The Americas segment exhibited 7% YOY revenue growth, while the Asia-Pacific segment showed a 4% revenue decline. Cooper Companies’ non-GAAP EPS increased 20% YOY to $1.10. The company is targeting more than $2.20 billion in free cash flow from 2026 through 2028.

For the second quarter of fiscal 2026 (to be reported on June 4, after the market closes), Street analysts expect the company’s profit to increase 14.6% YOY to $1.10 per diluted share. For the current fiscal year, it is expected to increase 12.1% to $4.62 per diluted share, followed by an 8.2% growth to $5 per diluted share in the following fiscal year. The company also has a solid history of surpassing consensus estimates, topping them in each of the four trailing quarters.

Among the 17 Wall Street analysts covering Cooper Companies’ stock, the consensus is a “Moderate Buy.” That’s based on nine “Strong Buy” ratings, one “Moderate Buy,” six “Holds,” and one “Strong Sell.” The ratings configuration has remained consistent over the past two months.

In March, analysts from Barclays maintained an “Overweight” rating on Cooper Companies and raised the price target from $98 to a Street-high of $103. Analysts cited improving sequential growth in the company’s Vision and Surgical segments, although partially offset by declines in older, lower-margin hydrogel products in Japan.

Cooper Companies’ mean price target of $90.60 indicates a 44.8% upside over current market prices. Moreover, the Street-high price target of $103 implies a potential upside of 64.7%.