/Tesla%20Inc%20tesla%20by-%20Iv-olga%20via%20Shutterstock.jpg)

In February 2026, the competitive landscape of autonomous vehicles and robotaxi services is shifting in a way that could materially impact Tesla (TSLA). Alphabet's (GOOG) (GOOGL) Waymo is a self-driving pioneer, has just completed one of the largest funding rounds in autonomous vehicle history, raising $16 billion and achieving a valuation of roughly $126 billion, nearly three times its valuation just 16 months earlier. This fresh capital will accelerate its expansion into more than 20 new cities, backed by a roster of top institutional investors and Alphabet as the majority stakeholder.

The monumental round underscores strong investor conviction in Waymo’s technology, commercial traction, and leadership in robotaxi deployment, with the company already delivering hundreds of thousands of weekly rides across several major areas.

Meanwhile, Tesla’s valuation is at a level that has drawn concern from some analysts, given the company’s reliance on future growth in autonomous services and robotics to justify its valuation. At the same time, Tesla’s core automotive business faces slowing deliveries and margin pressures, and its Full Self-Driving (FSD) suite and robotaxi initiatives continue to be scrutinized for commercialization timelines.

So, does Waymo’s momentum signal that Tesla’s valuation may be overextended, and is February 2026 the time to consider trimming or selling TSLA?

About Tesla Stock

Tesla is an automotive and clean energy company headquartered in Austin, Texas. Tesla designs, manufactures, and sells electric vehicles (EVs), alongside energy storage solutions such as Powerwall and Megapack, solar products like solar panels and Solar Roof, and related services.

Over the years, Tesla has expanded globally with a network of production facilities, showrooms, service centers, and Supercharger stations, and has increasingly emphasized advanced software and autonomous capabilities as part of its long-term strategy. Tesla is one of the world’s most valuable companies, with a current market cap of approximately $1.6 trillion.

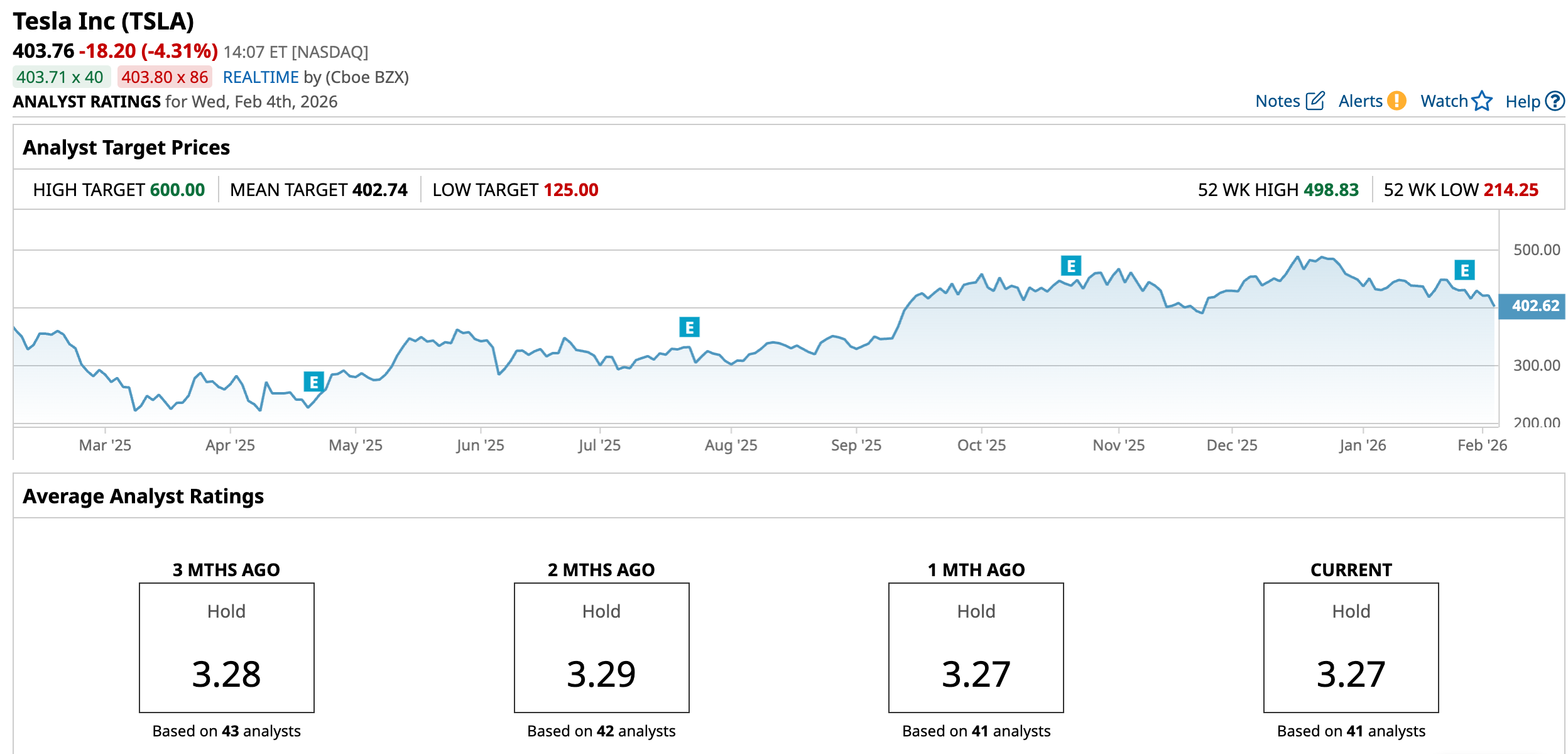

Tesla’s share price has experienced a dramatic and often volatile journey over the past year, reflecting shifting investor expectations. TSLA closed the last session at $405.42, about 18.7% below its 52-week high of $498.83, reached on Dec. 22, 2025. This underscores the stock’s roller-coaster behavior surging on optimism over autonomous technology and AI initiatives, then retreating sharply on softer deliveries and profit concerns. The stock is, however, up by around 3% over the past year.

TSLA reached record highs in December 2025 amid enthusiasm around robotaxi testing milestones and hopes of revenue improvement.

However, year-to-date (YTD), Tesla’s performance has been negative, with a YTD plunge of 10.19%. The stock’s performance has been tempered by operational headwinds, including slowing vehicle deliveries, increased competition in the EV market, and concerns over execution on robotaxi commercialization.

In terms of price-to-earnings (P/E) ratio, TSLA stands at 271.64 times, well above industry averages, suggesting investors are pricing in sustained high growth and successful commercialization of new businesses such as robotaxis and humanoid robots. Also, the stock is at 14.35 times sales, which is also a premium compared to its peers.

This premium valuation seems difficult to justify based on current fundamentals alone, given slowing vehicle deliveries, compressed margins and heightened competition in EV markets, leading some to label the stock as overvalued.

Muted Financial Performance

Releasing financial results on Jan. 28 for Q4 2025, Tesla reported total revenue of $24.9 billion, a 3% decline year-over-year (YOY). Automotive revenue, the core of Tesla’s business, fell more sharply, down about 11% YOY to $17.7 billion, reflecting softer vehicle sales and pricing pressures.

However, energy generation and storage revenue grew robustly, rising about 25% YOY, and services and other revenue increased 18% YOY. Gross margins improved to 20.1%, the highest in several quarters. Tesla reported non-GAAP earnings per share (EPS) of $0.50, marking a 17% YOY decline.

Operationally, Tesla delivered 418,227 vehicles in Q4, down about 16% from Q4 2024, with production of 434,358 units. Comparatively, Q4 2024 deliveries were roughly 495,570 vehicles, highlighting the moderation of demand.

For the full year 2025, Tesla posted revenue of about $94.8 billion, a 3% drop from 2024, marking the first annual revenue decline in the company’s history. Automotive revenue contracted about 10%, while energy storage continued to grow, up about 27%. Full-year net income stood at $3.8 billion, which was down around 46% YOY, reflecting persistent margin pressure and increased costs. Non-GAAP EPS for 2025 came in at $1.66, reflecting a 28% YOY decline.

Total vehicle deliveries for 2025 were approximately 1.6 million, down 9% YOY.

Additionally, Tesla signaled a continued pivot toward its AI, robotics, and autonomous strategy, including production of its Cybercab robotaxi in 2026 and expanded investment in related technologies such as Optimus humanoid robots and AI infrastructure, even as it phases out older models. Management also reiterated that capital expenditures will rise significantly in 2026, emphasizing long-term growth initiatives.

Analysts predict EPS to grow 53.2% YOY for fiscal 2026, and again rise 19.2% to $1.99 in fiscal 2027.

What Do Analysts Expect for Tesla Stock?

Recently, Freedom Capital Markets raised its Tesla price target to $440 from $406 but maintained a “Hold” rating, following Q4 2025 results.

Also, Needham reiterated its “Hold” rating on Tesla after Q4 results, while highlighting Tesla’s lofty valuation, concluding that much of the long-term upside is already priced in.

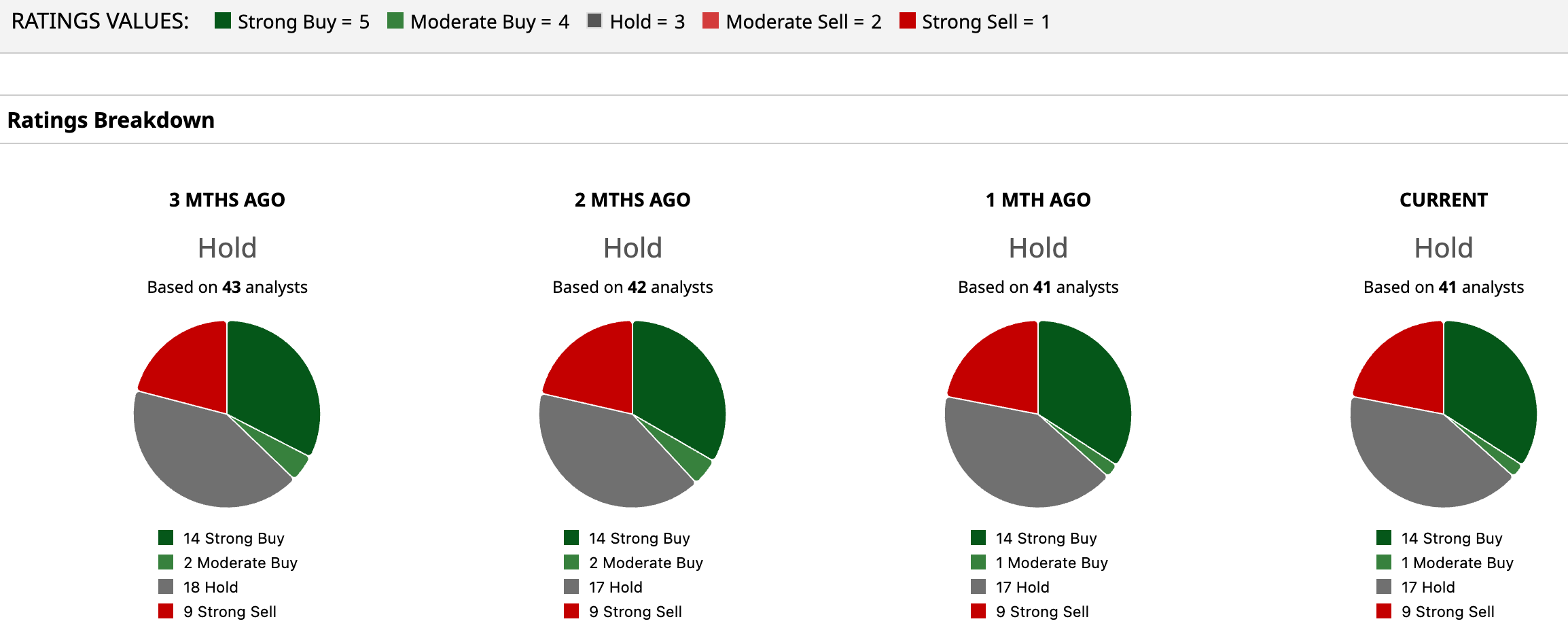

Overall, TSLA has a consensus “Hold” rating, indicating a cautious stance. Of the 41 analysts covering the stock, 14 advise a “Strong Buy,” one recommends a “Moderate Buy,” 17 analysts are on the sidelines, giving it a “Hold” rating, and nine propose a “Strong Sell.”

TSLA has already surpassed the average analyst price target of $402.74, while the Street-high target price of $600 suggests that the stock could rally as much as 48.6%.