/Visa%20Inc%20cards%20in%20wallet-by%20FinkAvenue%20via%20iStock.jpg)

San Francisco, California-based Visa Inc. (V) is a payment technology company with a market cap of $623.7 billion. It facilitates secure, fast transactions through its advanced technology and global infrastructure, enabling digital money movement and supporting commerce worldwide.

Shares of this payment technology company have lagged behind the broader market over the past 52 weeks. Visa has gained 16.6% over this time frame, while the broader S&P 500 Index ($SPX) has soared 18.5%. Moreover, on a YTD basis, the stock is up 7.7%, compared to SPX’s 15.1% uptick.

Nonetheless, zooming in further, V has considerably outperformed the Amplify Digital Payments ETF’s (IPAY) marginal 52-week decline and 8.2% YTD loss.

On Oct. 28, Visa delivered better-than-expected Q4 results, yet its shares plunged 1.6% in the following trading session. Due to continued healthy consumer spending, the company's net revenue improved 11.5% year-over-year to $10.7 billion, surpassing consensus estimates by a slight margin. Meanwhile, its adjusted EPS of $2.98 increased 10% from the year-ago quarter, topping analyst expectations by a penny. However, its total operating expenses surged by a notable 40% from the prior-year quarter, outpacing revenue growth, which led to a noteworthy decline in operating margins, making investors jittery.

For fiscal 2026, ending in September, analysts expect V’s EPS to grow 11.7% year over year to $12.81. The company’s earnings surprise history is promising. It surpassed the consensus estimates in each of the last four quarters.

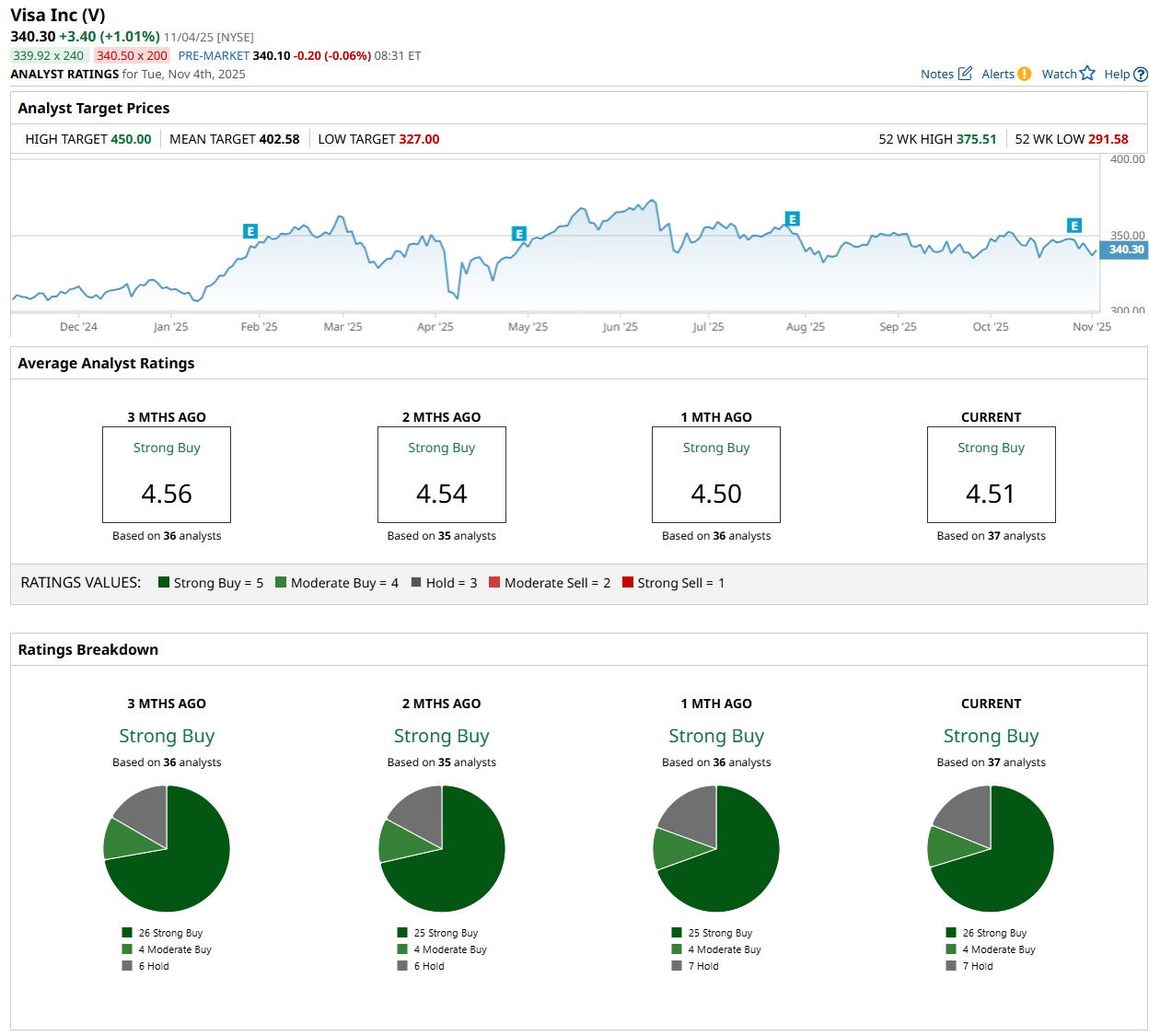

Among the 37 analysts covering the stock, the consensus rating is a "Strong Buy,” which is based on 26 “Strong Buy,” four “Moderate Buy,” and seven "Hold” ratings.

This configuration is slightly more bullish than a month ago, with 25 analysts suggesting a “Strong Buy” rating.

On Oct. 29, Macquarie analyst Paul Golding maintained a "Buy" rating on Visa and set a price target of $410, indicating a 20.5% potential upside from the current levels.

The mean price target of $402.58 represents an 18.3% premium from V’s current price levels, while the Street-high price target of $450 suggests an upside potential of 32.2%.