New York-based VICI Properties Inc. (VICI) is a prominent real estate investment trust (REIT) focused on owning and managing a portfolio of gaming, hospitality, and entertainment properties. With a market capitalization of $31.4 billion, VICI Properties holds a diverse range of assets, including casinos, hotels, and entertainment venues, located across key U.S. gaming markets.

Shares of VICI have underperformed the broader market over the past 52 weeks. VICI has plunged 2.5% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 20.9%. However, in 2025, VICI shares are up 2%, compared to SPX’s 1.9% gain on a YTD basis.

Zooming in further, VICI has also trailed the Real Estate Select Sector SPDR Fund’s (XLRE) 7.9% gain over the past 52 weeks.

On Oct. 31, VICI shares declined 2% after reporting its Q3 results. Both revenue and FFO surpassed the consensus estimates, and it updated its AFFO guidance to a range of $2.36 billion to $2.37 billion.

For FY2024, which ended in December, analysts expect VICI’s FFO to grow 5.1% year-over-year to $2.26 per share. The company’s earnings surprise history is promising as it consistently beat or met the consensus estimates in the last four quarters.

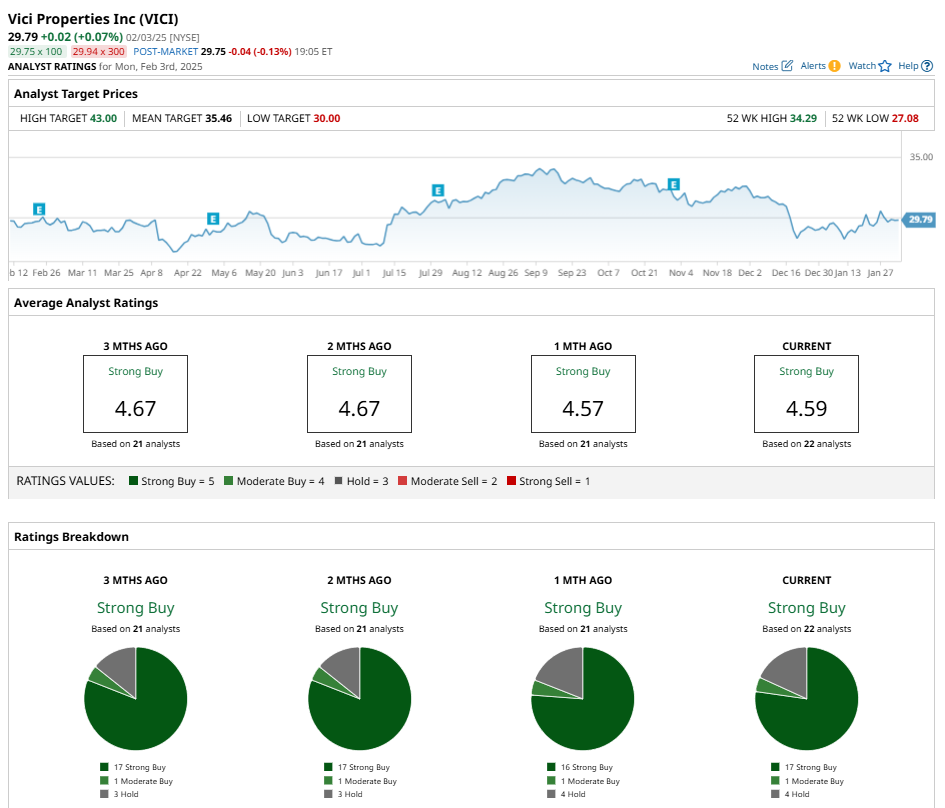

Among the 22 analysts covering the stock, the consensus rating is a “Strong Buy.” That’s based on 17 “Strong Buy” ratings, one “Moderate Buy,” and four “Holds.

This configuration is slightly more bullish than a month ago, with 16 “Strong Buy” ratings on the stock.

On Jan. 27, JMP Securities reaffirmed its positive outlook on VICI Properties, maintaining a “Market Outperform” rating and a $35 price target. The firm highlighted VICI’s 5.84% dividend yield, consistent dividend increases for 7 years, and strategic shift towards financing transactions in response to the volatile interest rate environment. This new focus includes financing projects like the Great Wolf Resorts and Venetian Property Refresh, rather than traditional acquisitions.

The mean price target of $35.46 represents a premium of 19% from prevailing price levels. Its Street-high price target of $43 implies a potential upside of 44.3% from the current price.