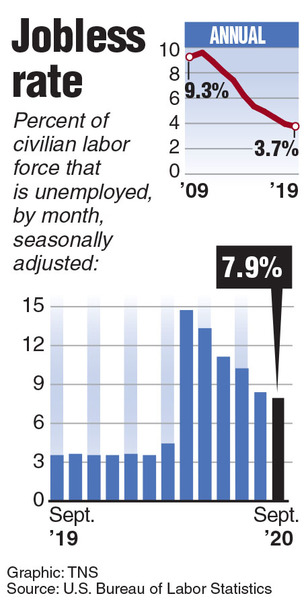

WASHINGTON _ The federal government's last jobs report before the election, released Friday, showed the third straight month of weakening recovery in employment. The nation added just 661,000 positions in September, down sharply from the 1.5 million gained in August.

And while the unemployment rate fell to 7.9%, from 8.4% in August, that wasn't good news given the reason: About 700,000 workers dropped out of the labor force, suggesting many are striking out in the job market. The report came hours after President Donald Trump confirmed that he and his wife tested positive for the coronavirus, giving a double jolt to a reelection campaign he's centered on his promises of a speedy "V-shaped" recovery and end to the pandemic. Stocks opened sharply lower.

The employment report, which covered both new jobs and those filled by calling back laid-off workers, seemed to confirm many analysts' pessimism over the nation's economic outlook, even as some other measures pointed toward a brighter future.

Retail sales, housing activity and business capital spending have been stronger than expected recently, thanks in part to federal pandemic-aid programs that are now largely expired, as well as robust monetary support from the Federal Reserve. The latest measures of consumer confidence showed gains, an especially encouraging sign when consumer spending accounts for some 70% of total economic activity.

The contrast between such positive indicators and the darker signs in both Friday's employment report and the views of most mainstream analysts in large part reflects the unique quality of the recession triggered by the COVID-19 pandemic. Unlike in past downturns, when the economic damage usually has been spread more broadly, today, there are essentially two economies: Millions of Americans, especially lower-wage workers, have been rocked by layoffs and lost incomes, while millions of others have remained largely untouched, mostly in higher-income, white-collar jobs.

What makes the dramatic fall-off in job gains last month worrisome is that it suggests the economic destruction of the pandemic has begun to spread upward into the previously stronger segments of the workforce. That is happening amid indications Thursday that negotiations have all but collapsed between Congress and the White House for up to $2 trillion in further federal relief.

"It is clear that the economic rebound is entering a new, weaker phase," said Michael Pearce, senior U.S. economist at the research firm Capital Economics.

The darkening economic outlook was unwelcome news at the White House and Trump reelection headquarters.

"Heading into today's number, the unemployment rate was already looking likely to show the worst economy of any president running for reelection in modern economic history," said Chris Rupkey, chief financial economist for MUFG Bank in New York.

"This is the highest unemployment and worst economy for any president facing reelection in history," he said, noting that when President Jimmy Carter lost his bid for a second term, the unemployment rate before the election was 7.5% in September 1980. When President George H.W. Bush unsuccessfully sought a second term in 1992, the jobless rate was 7.6% in September.

Evidence outside official government reports also has hopes for a quick rebound fading, including recent announcements of large layoffs by major corporations as varied as Raytheon, Allstate and Marathon Petroleum.

Burbank, Calif.-based Disney Co. said this week that it's cutting 28,000 jobs, most of them at its theme parks and resorts in Florida and California.

"The easy part of the labor market recovery is largely behind us now," said Brian Coulton, chief economist at Fitch Ratings. "The sobering statistic here is that 36% of unemployed are now classed as permanent job losers, up from 14% in May."

In California, so-called early warning layoff notices from employers were on pace to exceed levels in the past two months. Through Sept. 23, officials received 299 notifications affecting more than 28,000 workers. A little more than half were for permanent job losses, a notably higher percentage than in prior months.

"As we enter October, the California economy is stalled, with no significant uptick in hiring," said Michael Bernick, former director of the state's Employment Development Department. "As the economic lockdowns slowly lift, employers are bringing back some of the workers laid off earlier in the pandemic. But they are not hiring additional workers."

Separate data from economists at Harvard and other institutions tracking the recovery show that as of Sept. 20, the number of small businesses in California was down 29.4% from January. For the nation, that figure was 24.2%.

And now, a rise in COVID-19 cases in much of the country raises the specter of new business shutdowns and a pullback from the gains made in consumer traveling, shopping or and dining out. "We've reached a point where even if the economic lockdowns were fully lifted tomorrow, hiring will be slow until there is a vaccine, and many workers will remain reluctant to go back," Bernick said.

Sophia Koropeckyj, a labor economist at Moody's Analytics, wrote in a note to clients that the recovery of 661,000 jobs can't be dismissed. The gains were spread in both manufacturing and construction as well as services, she said, led by the hard-hit restaurant and hospitality sectors continuing to claw back gains. But the economy has regained only about half of the 22 million jobs lost to the pandemic, and the recovery is petering out.

Last month, she noted, the pace of hiring was down especially at retail stores. Job growth tapered off at professional and business services, and there was a sizable drop in local government jobs as many schools have turned to remote learning.

"The shift into permanent unemployment is likely to increase until a widely available vaccine enables the economy to function more normally. Many businesses on hold because of the pandemic will not be able to hold on much longer," she said.

Koropeckyj added: "There is a good chance that economic activity will stall in the fourth quarter, as long as the pandemic persists and Congress is unable to agree on the sorely needed fourth fiscal stimulus package to provide support to distressed households and state and local governments struggling to maintain services amid falling revenues."