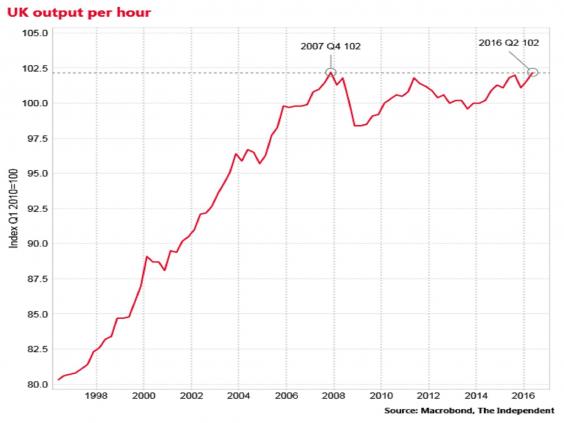

The UK’s level of productivity has finally crawled back to its pre-recession peak after nine years, but it remains far below its pre-financial crisis trend and still languishes well below other advanced countries.

The UK’s output per hour worked across the whole economy grew by 0.6 per cent in the three months to June, slightly faster than the 0.5 per cent expansion in the first quarter, according to the Office for National Statistics.

This was after GDP grew by 0.7 per cent, but hours worked increased by just 0.1 per cent.

That took the level of productivity, on this measure, to the heights last seen in the final quarter of 2007, when the UK was on the verge of a deep recession.

Back to peak

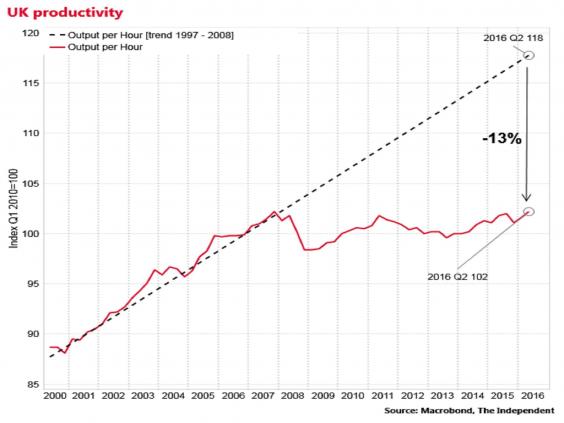

However, the level of productivity is around 13 per cent lower than if productivity had continued to grow on its 1997-2008 trend rate.

Mind the gap

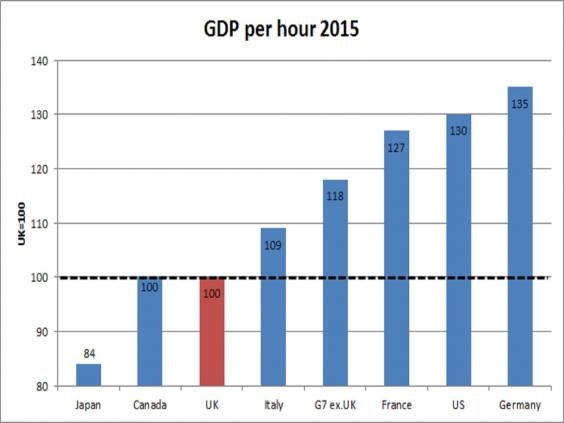

And the ONS also reported that the level of UK productivity was 27 per cent below France, 30 per cent below the US and 35 per cent lower than in Germany in 2015.

The UK was 18 per cent below the rest of the G7 excluding Britain.

International laggard

In his speech to the Conservative party conference on Monday the Chancellor Philip Hammond highlighted the UK’s poor productivity performance saying “millions of British workers are working longer hours for lower pay than their counterparts in Europe and the US”.

Hammond said he would put raising productivity at the heart of the Government’s industrial strategy, noting that a 1 per cent increase in the UK’s productivity growth rate would boost GDP by an additional £250bn within a decade, equivalent to £9,000 per household.

Official forecasters such as the Bank of England and the Office for Budget Responsibility have become steadily less optimistic about the UK’s productivity growth potential since the financial crisis, after successive forecasts of a bounceback in the growth rate have been disappointed.

The Bank of England now expects productivity to grow by 0.75 per cent this year, rising to 1.25 per cent in 2017 and 1.5 per cent in 2018 – all well below the pre-crisis average rate of 2.25 per cent.

Some sectors of the economy have seen particularly bad productivity performances.

The productivity of finance and insurance is still 14 per cent below where it was in 2007, a likely impact of the unsustainable rate of growth of the sector in advance of the global financial crisis.

But economist still regard the UK's exceptionally weak level of productivty across the whole economy since 2007 as a "puzzle", with some arguing that it would be higher if aggregate demand was higher and others saying that the supply capacity of the UK economy has been permanently impaired by the financial crisis.

Others argue that a lack of capital investment by firms and the ready availability of cheap labour are important factors in the story.

“Securing a sustained recovery can only come from increased investment in people and new technologies. The forthcoming Autumn Statement needs to show how the Government intends to support future productivity growth through investment in infrastructure, skills, and the science base" said Ian Brinkley of the Chartered Institute of Personnel and Development.