European markets down on Greek concerns

Another mixed day for stock markets, writes Nick Fletcher, with European shares under pressure on continuing worries about Greece’s finances as the latest deadline to reach a deal with its creditors approaches. Wednesday sees the latest meeting of the European Central Bank, with investors hoping an update on its quantitative easing programme will provide some support to the markets. But a revival in the mining sector saw the UK market buck the falling trend, while lower than expected US retail sales cast doubts again on an imminent rate rise from the Federal Reserve. The final scores showed:

- The FTSE 100 finished up 10.96 points or 0.16% at 7075.26

- Germany’s Dax dropped 0.9% to 12,227.60

- France’s Cac closed down 0.69% at 5218.06

- Italy’s FTSE MIB lost 1.07% to 23,752.91

- Spain’s Ibex ended down 1.36% at 11,704

- The Athens market fell 2.24% to 758.63

On Wall Street the Dow Jones Industrial Average is currently nearly 50 points or 0.3% higher.

On that note, it’s time to close up for the evening. Thanks for all your comments, and we’ll be back tomorrow.

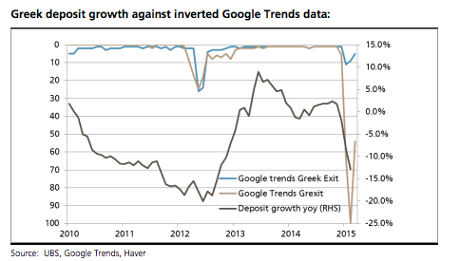

Investors are seriously underestimating the dangers that Greece’s potential exit from the eurozone would pose to the rest of the region, warns Paul Donovan of Swiss bank UBS.

He fears that the current rally in eurozone government bonds (which are now trading at record highs) has helped create a dangerous complacency.

If Greece were to quit the eurozone, it could spark a major banking panic across the region as savers in other peripheral countries took out their savings just in case they were next.

As Donovan puts it:

The contagion risk after a possible Greek exit arises if bank depositors elsewhere in the Euro area believe that a physical euro note held “under the mattress” at home today is worth more than a euro in a bank – because a euro in a bank might be forcibly converted into a national currency tomorrow.

Donovan adds that “There are some important things to note here”:

-

This is not a question of banking system solvency. Highly solvent banks will be subject to deposit flight if it is the value of the currency in that country that is uncertain.

-

This is not a question of the fiscal strength of the government. The question is whether the government is willing to bear the cost of staying in the monetary union .

-

This is not a question of bank depositors being certain of a monetary union breakup. The catalyst of deposit flight is likely to be triggered by the possibility of a breakup in the monetary union.

-

Popular opinion is irrelevant (it is worth noting that a very sizeable majority of Greeks wish to remain in the Euro and this has not stopped deposits falling in that country). In dealing with one’s assets the important driver of action is not what one wants to happen but what one fears might happen.

-

The example of economic pain in Greece in the wake of an exit from the Euro is irrelevant. Depositors in other countries may recognise that exit from the monetary union is economically disastrous, but if they think there is any possibility that their own economy could be forced down that route then it is logical to withdraw deposits. Indeed, economic chaos in Greece after an exit may be an incentive to accelerate deposit withdrawal elsewhere.

He also provides a chart, showing that Greek bank deposits tend to fall as anxiety over the crisis rises....

EU foreign policy chief Federica Mogherini doesn’t share Olivier Blanchard’s optimism that a Grexit would be manageable......

*MOGHERINI: GREXIT `COULD BE BEGINNING OF END' FOR EUROPE UNITY

— lemasabachthani (@lemasabachthani) April 14, 2015

IMF: Grexit would be costly, but manageable

Olivier Blanchard, the International Monetary Fund’s chief economist, has just told reporters that the eurozone could cope if Greece quit the single currency.

Speaking at the press conference in Washington, Blanchard said that a Gexit would be very costly and painful, but not impossible to handle.

There are better firewalls in place than in 2012, he pointed out, but obviously it wouldn’t be smooth sailing.

It feels like a nudge to Greece to finally deliver a credible reform package by next Monday, as its increasingly impatient creditors have asked.

Interesting that IMF Chief Economist Olivier Blanchard just publicly stated that a #Grexit "could be done" & handled by the #Eurozone

— Open Europe (@OpenEurope) April 14, 2015

Updated

If the IMF forecasts are accurate, then Britain will be the second-fastest growing advanced nation this year (having been the fastest in 2014).

Latest IMF growth forecasts for the major advanced economies. UK in second place. pic.twitter.com/9ySO6kvtKs

— RBS Economics (@RBS_Economics) April 14, 2015

Here’s the full forecasts just released by the IMF:

Here’s another interesting chart from the IMF’s new World Economic Outlook, showing the damage caused by the financial crisis:

IMF: Output Compared to Precrisis Expectations pic.twitter.com/2g1NTQMWAs

— Fabrizio Goria (@FGoria) April 14, 2015

IMF: Core eurozone countries must do more

The IMF has also paid tribute to the European Central Bank, saying its QE stimulus programme appears to have “stalled the decline in inflation expectations”.

But there’s less love for Germany; just a nudge to do more to help its euro neighbours.

#IMF's new #WEO concerned "core economies" in eurozone not fiscally "accommodative" enough. Whoever could they mean? pic.twitter.com/8Swzv5nu6K

— Peter Spiegel (@SpiegelPeter) April 14, 2015

IMF hikes eurozone growth forecast

The IMF has good news for the eurozone -- it has raised its growth forecast for the region in 2015 to 1.5%, up from 1.2% previously.

It sees growth strengthening a little in 2016, to 1.6%. The weaker euro, and the fall in oil prices, should give European countries a boost, it believes.

The Fund is still optimistic for Greece, too, despite the current crisis.

The #IMF's just-released #WorldEconomicOutlook still has decent growth projections this year for #Greece pic.twitter.com/EWLV0tM9TV

— Peter Spiegel (@SpiegelPeter) April 14, 2015

IMF releases new World Economic Outlook

Breaking: The International Monetary Fund has reiterated that global growth will pick up in 2015 and 2016, but warned that the recovery is “moderate and uneven”.

In its new World Economic Outlook, just released, the IMF stuck to its forecast of global growth of 3.5% this year, rising to 3.8% in 2016 (compared with 3.7% in its January forecasts).

It has raised its forecast for Japan, but has downgraded its hopes for the US economy.

* IMF increases growth forecast for Japan to 1 pct this year, 1.2 pct in 2016 - RTRS

— Fabrizio Goria (@FGoria) April 14, 2015

* IMF cuts U.S. GDP growth forecast to 3.1 pct this year and next year, from 3.6 pct and 3.3 pct in January - RTRS

— Fabrizio Goria (@FGoria) April 14, 2015

The Fund has also warned that the global economy is vulnerable to shocks, following the 2008 financial crisis.

As our economics correspondent Phillip Inman reports from Washington:

The IMF.... warned that the “complex forces” that affected global activity in 2014 – including wild swings in exchange rates and collapsing commodity prices – were still shaping economic events.

Longer-term issues have also depressed the “productive capacity” of many countries, the IMF said, including large debt mountains and ageing populations in Europe, Japan and the US.

Updated

Heads up: The International Monetary Fund will release its latest assessment of the world economy in 10 minutes time.

Getting ready for the launch of the World Economic Outlook #WEO at 9 am ET. Follow live: http://t.co/gEJfJozXM6 pic.twitter.com/is2I7jALJF

— IMF (@IMFNews) April 14, 2015

Updated

Over to the US.... and the latest retail sales figures have just been released, and missed forecasts.

Granted, sales jumped by 0.9% in March - the fastest rise in a year. But the dollar is weakening, because economists had expected a bigger bounceback.

US retail sales up 0.9% in March (-0.6% in Feb), missing consensus of +1.1%, but still largest rise in a year

— Markit Economics (@MarkitEconomics) April 14, 2015

It bolsters the case that the US Federal Reserve might not raise interest rates until the autumn, or even later.

A June rate hike was already looking unlikely, as this chart from Bank of America-Merrill Lynch shows:

Fund Managers are now even more biased towards a 3Q lift-off, per BAML pic.twitter.com/m613wVhDwx

— Lady FOHF (@LadyFOHF) April 14, 2015

Lunchtime summary: Inflation pegged at zero again

Time for a recap.

Britain has avoided falling into negative inflation for the first time in over half a century.

The Consumer Prices Index was unchanged year-on-year in March, the second month running of zero inflation in the UK.

Food prices are down by 3.2% annually, while motor fuel prices have tumbled by 13.7%.

Core inflation, which ignores such items, fell unexpectedly to a nine-year low of 0.9% - indicating that underlying inflationary pressures have weakened.

Consumer Price Inflation flat y/y in March according to @ONS. But another chunky drop in core inflation to just 1%: pic.twitter.com/r6FfaZz3sE

— Ben Chu (@BenChu_) April 14, 2015

The Office for National Statistics also found that clothing and footwear prices fell during March, the first monthly decline since they started calculating the CPI in 1996.

Petrol prices, though, inched up during the month.

Historic data shows that the CPI hasn’t been negative since March 1960:

UK inflation steady at record-low zero percent in March http://t.co/FWAWp50NyB via @Reuters pic.twitter.com/cBqvLjSII7

— Global Markets Forum (@ReutersGMF) April 14, 2015

Economists remain split on whether inflation will fall below zero in a month’s time. But there’s broad agreement that we are not heading into a deflationary spiral. Reaction starts here.

UK chancellor George Osborne claimed the data showed the economy is in good health; Labour disagreed.

For more, just scroll back to 9.30am -- or even better, read Katie Allen’s story:

Updated

Allan Monks of JP Morgan says there’s a decent chance UK inflation will inch up this month:

With petrol prices having risen in April, the currency falling, utility bill cuts largely passed through, and global agricultural commodity prices having stabilized, headline inflation could rise to 0.1% in April even as core weakens.

We still see downside risk to our forecast for headline inflation, but March may have marked the trough in headline.

And here’s JPM’s inflation forecasts, from a research note titled “UK skirts deflation despite drag from womens clothing”*

* We’ll do the puns, you do the thinking, ok?

Greek finance minister Yanis Varoufakis will meet Barack Obama on Thursday, as the clock ticks towards Athens’ next deadline.

Greek newspaper eKathimerini reports:

Varoufakis is in Washington for the Spring Meetings of the World Bank Group and the International Monetary Fund. He is expected at the White House on Thursday to attend celebrations for the March 25th Greek Independence Day celebrations, becoming the first official of the recently elected Greek government to meet with the US president.

Sources say he will have a few moments to talk with Obama and US Vice President Joe Biden at a time when Greece is in crucial negotiations with its international creditors.

What are the odds @yanisvaroufakis will wear a tie to his meeting with @BarackObama? I say he won't. http://t.co/1OMIQpGvAg

— Felix Salmon (@felixsalmon) April 14, 2015

Greece’s creditors want to see a detailed list of reforms by next Monday, so finance ministers could discuss then and potentially release bailout funds on Friday 24th April.

Back to Greece.... and European Commissioner Pierre Moscovici has told the European Parliament that he’s still waiting for a detailed reform list from Athens:

#EU's Moscovici says need list of precise reforms from Greek gov't ~BBG | #Greece

— Yannis Koutsomitis (@YanniKouts) April 14, 2015

Moscovici Says Need List Of Precise Reforms From Greek Govt "like pulling teeth out"

— Steve Collins (@TradeDesk_Steve) April 14, 2015

One of the City’s most pessimistic analysts, Albert Edwards of Societe Generale, has just warned that Britain’s will face a currency crisis due to the large current account deficit.

Living up to his reputation as a ‘permabear’, Edwards’ latest report claims the UK was a ‘ticking time bomb”.....

Albert's channelling 2010-era Bill Gross... pic.twitter.com/qkDT4KhMhc

— James vS (@James_v_S) April 14, 2015

Seven years later and Albert's still pushing the imminent collapse schtick... pic.twitter.com/eIJADlfem2

— James vS (@James_v_S) April 14, 2015

"sterling crisis" klaxon from Edwards. Gotta love election season. https://t.co/9Sk10FkvNM

— Katie Martin (@katie_martin_FX) April 14, 2015

Here’s my colleague Katie Allen on today’s inflation data:

It’s a tale of two inflation rates, says former Bank of England policymaker Andrew Sentance:

Zero inflation in UK conceals big disparity between food and energy prices down by over 3pc on a year ago and services inflation of 2.4pc

— Andrew Sentance (@asentance) April 14, 2015

Petrol prices tick up....

Today’s inflation report contains bad news for motorists, who may have got used to paying less at the pump.

Average petrol prices rose by 3.8 pence per litre between February and March this year, suggesting that the boost from weaker oil prices has ended [Brent crude has risen during 2015, after tumbling in late 2014].

If fuel prices keep rising, then Britain’s inflation rate may not fall below zero at all, says Ben Brettell, senior economist at Hargreaves Lansdown.

He adds:

Falling inflation has largely been driven by falling fuel and food costs, and this should be positive for the economy. When the price of essential goods and services falls, it acts like a tax cut, boosting disposable incomes and allowing consumers to spend on other items.

[Bank of England governor] Mark Carney has described the impact of cheaper oil prices as “unambiguously good” for the economy.

This is a rather neat chart from the Economist Intelligence Unit:

UK inflation since 2010: evident effect of falling prices of energy, food in last few months; imported price effects pic.twitter.com/cNqInGthWi

— Linda Yueh (@lindayueh) April 14, 2015

Updated

High street sales helped to keep inflation at zero, points out Hannah Maundrell, editor in chief of money.co.uk:

“Today’s confirmation that UK inflation has remained at zero is welcome news.....

Although we are expected to return to inflation in the not too distant future, we’re facing uncertain times and it’s likely our flirt with deflation is not yet over.”

Martin Beck, senior economic advisor to the EY ITEM Club, says Britain could be flirting with negative inflation for several months:

“We expect inflation to remain close to zero until the latter months of this year, at which point the base effects, caused by the collapse in oil prices, will begin to kick in.

But core inflationary pressures are likely to remain well contained, ensuring that inflation remains below the 2% target for a prolonged period. Therefore, while the threat of ‘noflation’ becoming entrenched looks low, there is equally little threat of inflation taking off.

Let’s hope ‘noflation’ catches on

Inflation could turn negative by the summer, predicts Peter Cameron, assistant fund manager at Ecclesiastical Investment Management.

He’s not worried, though:

“Inflation has remained at 0% this morning but could well fall negative in the next couple of months. The fall in inflation over the past year has been driven by declines in the prices of essential, everyday items like food and fuel. Therefore it is the equivalent of handing consumers a temporary tax cut through cheaper household bills. What we have not witnessed in the UK so far is the toxic form of deflation that occurs when people defer purchases of big ticket items on the idea that they will become cheaper in the future.

As long as that is avoided, these inflation figures should be considered a positive for the UK economy and also provide more wriggle room for the Bank of England when determining when to begin raising interest rates”.

Reaction to today’s inflation data is flooding in, so I’ll round up the best quotes now....

....starting with Joshua Raymond of City Index, who sees little chance of an interest rate rise soon:

Clearly the UK remains on the cusp of deflation and this continues to put the Bank of England between a rock and a hard place when it comes to hiking interest rates.

The threat of deflation is pushing market views for the BoE’s first rate hike further out and whilst todays inflation reading will do little to change current forecasts, there were some fears we could see a deflationary print today.

No prizes for spotting the trend:

Falling inflation not all about oil. UK & EZ core inflation falling for last 3 years. pic.twitter.com/QE1XyIkoOB

— RBS Economics (@RBS_Economics) April 14, 2015

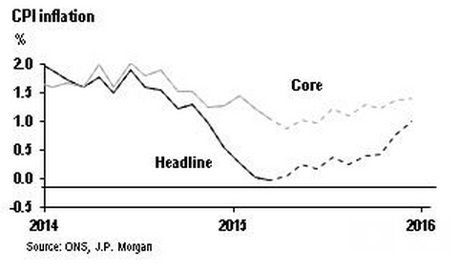

As flagged earlier, the UK’s core inflation rate (ignoring food, fuel, tobacco etc) has hit a nine-year low of 1.0%.

Updated

Inflation: the political reaction

The two main political parties didn’t waste seizing on today’s inflation figures.

Chancellor George Osborne (who saw the data yesterday) swiftly welcomed the news that CPI inflation remained at zero.

Our plan for working people gets another boost today with good news for family budgets - Inflation at zero for second month in a row.

— George Osborne (@George_Osborne) April 14, 2015

But Chris Leslie, Labour’s Shadow Chief Secretary to the Treasury, was predictably less impressed:

“A few months of falling world oil prices won’t solve the deep-seated problems in our economy or make up for years of bills rising faster than wages.

“Wages continue to be sluggish and are down £1,600 a year on average under this government. And tax and benefit changes since 2010 have left families £1,100 a year worse off on average.

UK house price growth slows

Britain’s housing boom is slowing down, according to this morning’s statistics.

The ONS reports that average prices rose by 7.2% year-on-year in February, compared with 8.4% a month ago.

London still outpaced the market, with prices up 9.4% year-on-year. But strip out the capital and the South East, and average prices were only up by 5.9%. Still faster than wage growth, but a sign that the market is cooling.

According to the ONS:

- House price annual inflation was 7.4% in England, 1.1% in Wales, 6.4% in Scotland and 14.2% in Northern Ireland.

- Annual house price growth is showing signs of slowing across the majority of the UK.

Newsnight’s Duncan Weldon argues that deflation is not a threat:

Reasons not to worry about deflation in the UK: service CPI well above 2%, wage growth positive. Reasons to worry: core CPI now at just 1%.

— Duncan Weldon (@DuncanWeldon) April 14, 2015

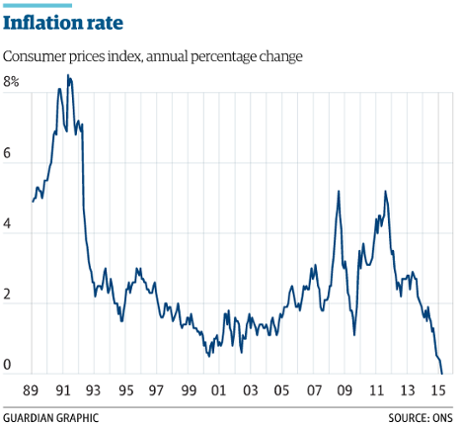

Hat-tip to Sky’s Ed Conway for showing that UK inflation is at its lowest since the start of the swinging 1960s.

Not since 1960 has CPI inflation been as low as it is today. Historical chart based on @ONS numbers: pic.twitter.com/GCZyB3GnmV

— Ed Conway (@EdConwaySky) April 14, 2015

UK retailers usually hike the cost of cardigans and shoes in spring, but not this year..

The cost of clothing and footwear fell month-on-month in March for the first time since the consumer prices index was created in 1996, according to the ONS.

Here’s how the inflation report explains it:

Clothing and footwear: prices, overall, fell by 0.1% between February and March this year, compared with a rise of 1.8% between the same 2 months a year ago. This is the first time that prices have fallen between February and March since the CPI was introduced. Normally prices rise as they continue to recover following the January sales period. The downward contribution came from price movements for a range of women’s outerwear, particularly trousers, dresses and cardigans. There was also a smaller downward effect from men’s outerwear.

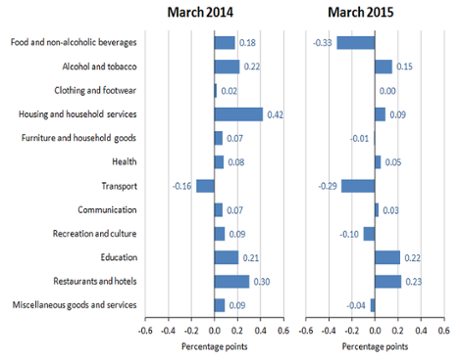

Inflation: The Key Charts

This chart from the ONS shows how inflation has rocketed towards zero in the last year:

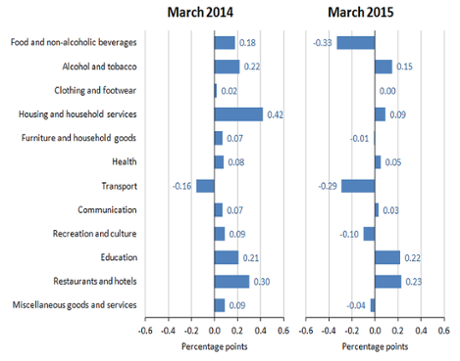

And this chart confirms that food and transport costs were the biggest drag on the annual inflation rate last month.

Eating out or getting educated cost more, though:

Updated

Cheaper food and energy prices are the main reason why inflation remained at zero last month.

The ONS says:

In the year to March 2015, food prices fell by 3.2% and prices of motor fuels fell by 13.7%. In both cases, the falls were smaller than in the year to February but the 2 groups still provided the largest downward contributions to the 12-month rate for March

Pound hit by weak core inflation

The pound has just fallen by half a cent against the US dollar, hitting $1.4614.

I reckon that is because Britain’s core inflation, which strips out volatile factors such as energy and food, fell to 1.0% in March, from 1.2% 1.4% in February.

That’s the lowest measure of core inflation since July 2006, suggesting weak underlying inflation pressures.

Updated

The Retail Prices Index measure of inflation rose by 0.9% year-on-year in March, down from 1.0% in February. That’s weaker than expected.

DEFLATION! But it's not as bad as all that. CPI drops to minus 0.01% in March, the tiniest of negative readings. Officially it's still 0.0%

— Richard Edgar (@ITVRichard) April 14, 2015

Inflation negative to two decimal places.....

Britain came extremely close to negative inflation, though.

The Office for National Statistics says that March’s consumer prices index actually dropped by 0.01% - which it has rounded up to zero.

UK ONS The Consumer Prices Index (CPI) was unchanged in the year to March 2015, that is, a 12-month rate of 0.0% #GBP #BoE

— Shaun Richards (@notayesmansecon) April 14, 2015

UK inflation sticks at zero

Breaking: Britain has avoided falling into negative inflation.

Consumer price inflation remained steady in March at 0.0%, meaning prices were unchanged year-on-year.

So inflation remains at its weakest level since 1960

More to follow....

Just 4 minutes to go until we find whether UK inflation remained at zero in March or not....

Updated

Greece’s denial that it’s preparing to default next month hasn’t prevented its government bonds weakening this morning.

That’s driving the yield, or interest rates, on its debt into even higher and more worrying levels:

Default risk climax RT @TradeDesk_Steve Greek yields (groundhog day): 10-yr 11.79 +21½ 5-yr 16.42 +79 3-yr 22.55 +121½bp #Greece

— Yannis Koutsomitis (@YanniKouts) April 14, 2015

Weak inflation isn’t just a British phenomenon.

Prices across the eurozone have been falling since December, and America’s CPI rate also briefly dipped below zero in January. Why? Falling oil prices and sluggish economic growth get the blame.

If you look back into history, periods of falling prices were a common sight until second world war.

As our economics editor Larry Elliott wrote back in 2007:

In the 19th century there were as many years of falling prices as of rising prices, with the result that the cost of living was lower when the first world war broke out in 1914 than it had been when Wellington triumphed at Waterloo in 1815.

But since 1945, deflation has been considered yesterday’s problem - in the UK at least. Japan, Sweden and the Czech Republic have all had periods of negative inflation, but the last time the published inflation rate went negative in Britain was in 1947. For most of the time, policymakers have been terrified at the prospect of an inflationary spiral, particularly in the 1970s and 1980s, when the annual increase in the cost of living rose above 20%.

That followed the death of the gold standard, which gave countries the flexibility to weaken their currencies by expanding the money supply.

There will be a splurge of data at 9.30am, as the Office for National Statistics releases its latest survey of UK house prices alongside the inflation data.

We also get the latest Retail Price Index, another inflation measure that also includes housing costs. That’s expected to have risen by 1.0% in March -- so no sign of deflation there....

Updated

We probably shouldn’t get too excited about inflation turning negative this morning.

A majority of City economists surveyed by Reuters reckon the Consumer Prices Index will remain unchanged in an hour’s time, meaning inflation remained at 0.0% for the second month running.

That would still mean the weakest inflation since 1960 (when My Old Man’s A Dustman was leading the charts).

Dominic Bryant, head of UK economics at BNP Paribas, reckons inflation will remain weak for some months:

“I don’t think there will be deflation. The bigger picture is it is going to be close to zero for another two or three months. It is low inflation now – you might get a negative print, you might not, but it is not deflation.”

Updated

Today’s inflation data will include the impact of a recent 5% price cut by British Gas.

That should bring utility bills lower, after years of inflation-busting price hikes helped to drive the cost of living up.

Petrol prices, though, appear to have bottomed out.

Centrica, incidentally, has just announced the new boss of British Gas -- Mark Hodges, an insurance industry veteran. It’s a politically charged appointment, given Labour pledge to rein in the energy sector if it wins the general election.

Greek default rumours swirl...

Denial ain’t just a river in Egypt, it’s also the Greek government’s standard response to most media reports these days.

This time, Athens has rubbished a report in the Financial Times that said it was preparing to default if it can’t reach agreement with creditors by the end of April.

According to the FT, Greece would withhold payments due to the IMF next month.

Here’s a flavour:

The government, which is rapidly running out of funds to pay public sector salaries and state pensions, has decided to withhold €2.5bn of payments due to the International Monetary Fund in May and June if no agreement is struck, they said.

“We have come to the end of the road . . . If the Europeans won’t release bailout cash, there is no alternative [to a default],” one government official said.

A Greek default would represent an unprecedented shock to Europe’s 16-year-old monetary union only five years after Greece received the first of two EU-IMF bailouts that amounted to a combined €245bn.

Such reports could potentially help Greece squeeze a deal out of its lenders. But a Greek government official insists it’s not true.

Greece denies reports in FT suggesting they are considering defaulting on debt if an agreement with its EU counterparts cannot be reached

— RANsquawk (@RANsquawk) April 14, 2015

However, if Greece doesn’t get a cash injection soon, it may not have much choice....

Isn't Greece preparing for default if talks fail a bit like me deciding to get wet when getting caught in rain? http://t.co/1xC2mqaENd

— Lorcan Roche Kelly (@LorcanRK) April 13, 2015

Updated

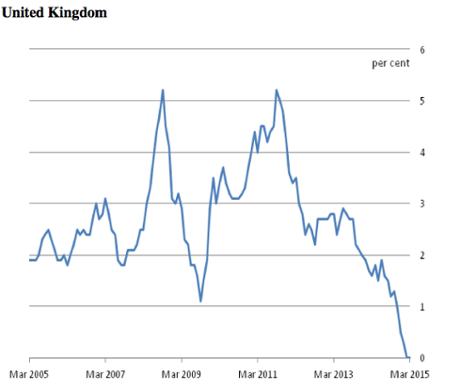

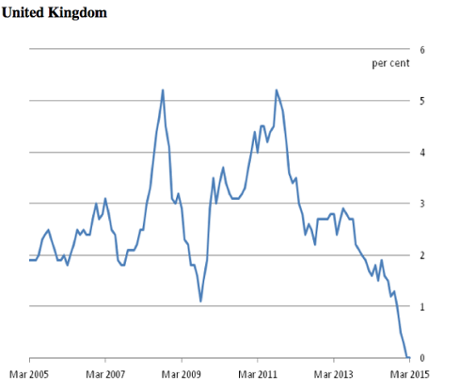

Today’s inflation numbers will not improve the Bank of England’s track record on hitting (or missing) its goals.

Since the financial crisis began, the CPI index has only enjoyed a passing relationship with the BoE’s 2% target, as this chart from last month shows:

Q&A: What negative inflation would mean for you

Press Association have published a Q&A about the possibility of the UK inflation rate falling below zero today.

Has this ever happened before?

CPI has never turned negative since comparable records began in 1989. According to an experimental data series by the Office for National Statistics (ONS) going back to 1950 it was last negative, at minus 0.6%, in March 1960.

Would it mean the pound in my pocket is worth more?

Yes. CPI at minus 0.1% would mean a basket of goods worth 100 a year ago is now worth 99.90. Low inflation has been driven by falling petrol and grocery prices.

Is there a downside?

Sustained falling prices could mean shoppers putting off purchases and firms delaying investment, while mortgages become less affordable, especially if wages drop. But this is thought unlikely, with temporary causes such as low oil prices likely to fade.

What will this mean for the General Election?

Coalition politicians will hope added purchase power creates a feel-good factor as well as boosting consumer spending and lifting the economy. But the boost to growth might come too late to affect first quarter figures out a week before the poll.

How will this affect interest rates?

The Bank of England must try to return inflation towards its target of 2% so low CPI should mean rates at 0.5% for longer. Deeper or more prolonged negative inflation could create growing speculation of interest rates being cut even further.

The Agenda: UK inflation, or deflation?....

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

Is Britain experiencing its first bout of negative inflation since Harold Macmillan was running the country? We’ll find out at 9.30am BST today, when the Office for National Statistics reveals the latest consumer prices index.

With the UK election just 23 days away, the figures will be scrutinised by all sides for clues into the state of the economy.

Some City economists predict the annual CPI turned negative in March, indicating that the cost of living actually fell (slightly) compared with a year ago.

That hasn’t happened in over half a century, according to estimates from the Office for National Statistics which suggest CPI (had it existed) would have fallen by 0.6% in March 1960.

The headline measure of inflation hit zero in February, dragged down by price-cutting between supermarkets and the slide in the oil price since last summer.

Other number-crunchers, though, reckon CPI probably remained nailed at 0.0% last month.

And either way, we’re unlikely to see full-blown deflation in Britain (a protracted period of falling prices, where people expect inflation to keep falling).

Alicia Higson, senior economist at the Centre for Economics and Business Research, says:

It is likely this will be a short-lived bout of deflation and the UK will returning to inflation later this year.

And we shouldn’t forget that inflation was significantly over the UK’s 2% target between 2011 and 2014. So shoppers have earned some relief.

As Alan Clarke, economist at Scotiabank, put it:

“While food price deflation of close to 4% year on year may sound extreme, this represents something of a relief after years of rapid price increases.

More specifically, over the seven years between 2007 and 2013, the average annual pace of increase in food price inflation was 5% per year. Enjoy the cheap food and fuel while it lasts!”

Here’s our full preview:

UK economy poised to welcome deflation for first time since 1960 - by me http://t.co/CaTKeJhFPC

— Julia Kollewe (@JuliaKollewe) April 12, 2015

We’ll bring you all the data and full reaction from 9.30am, along with other developments through the day, including Greece’s bailout talks.

Updated