Markets end positive quarter on downbeat note

A last day slide has not prevented European markets from recording a positive three monthly performance. The FTSE 100 has climbed 4.93%, its biggest increase since the three months to March 2013, but it was outshone by the FTSEurofirst 300 - up16% over the quarter, its best first quarter since 1998 - and Germany’s Dax, up 22%.

The European Central Bank’s quantitative easing has been one of the main factors behind the market surge, but the end of the quarter seems to have prompted investors to take profits. Underwhelming eurozone data, continuing worries about Greece, uncertainty over the timing of a US rate rise and another slump in the oil price all combined to take the shine off shares.

More here:

The closing scores showed:

- The FTSE 100 finished down 118.39 points or 1.72% at 6773.04

- Germany’s Dax dropped 0.99% to 11,966.17

- France’s Cac closed 0.98% lower at 5033.64

- Italy’s FTSE MIB fell 0.44% to 23,157.12

- Spain’s Ibex ended 0.07% down at 11,521.1

- The Athens market edged up 0.36% at 775.46

In the US, the Dow Jones Industrial Average is currently 104 points or 0.57% lower.

On that note, it’s time to close up for the evening. Thanks for all your comments, and we’ll be back tomorrow.

Greek deposit outflows slowed to €3bn in March, according to a Bloomberg report:

The outflow brings net withdrawals in four months to about €28bn, cutting the deposit total to about €137bn, the lowest in more than 10 years.

ECB policy makers hold a weekly review on Wednesday of their Emergency Liquidity Assistance, which is keeping Greek lenders afloat, according to two people familiar with the matter who asked not to be named because the talks are private. Last week it made more than 1 billion euros available, raising the limit to just over €71bn.

“Greece is being kept on an incredibly tight leash,” Michala Marcussen, global head of economics at Societe Generale SA, said in a Bloomberg Television interview. It’s “clearly intended to keep Greece under pressure and keep things moving forward in the negotiations.”

Full story here:

Greek Deposit Outflows Said to Slow to 3 Billion Euros

Portugal will benefit from its structural reforms and accelerating economic growth in the years ahead, but its large debt burden remains a challenge, ratings agency Moody’s has said in its annual analysis of the county:

“We expect Portugal’s real economic growth to accelerate to 1.7% and 1.8% in 2015 and 2016, respectively, from 0.9% in 2014, on the back of stronger domestic demand and renewed strength in exports. The implementation of broad structural reforms over the past several years should support a stronger economic growth path, while fiscal consolidation measures will help gradually reduce the country’s debt burden. However, Portugal’s debt levels still remain very high,” says Kathrin Muehlbronner, a vice president -senior credit officer at Moody’s.

Updated

#ECB balance sheet has expanded by a whopping €93bn as banks took €95bn in TLTRO loans and ECB bought govt bonds. pic.twitter.com/A5Imrmpte7

— Holger Zschaepitz (@Schuldensuehner) March 31, 2015

US consumers are becoming increasing confident, according to the latest conference board survey.

The March consumer confidence index came in at 101.3, better than the 96 figure expected by economists. This was up from a February figure of 98.8, itself revised up from 96.4.

Stock markets have been enjoying a good first quarter, not least thanks to the start (at last) of the European Central Bank’s quantitative easing programme.

But March is ending on a downbeat note, with a spate of profit taking hitting Wall Street, which had just opened. The Dow Jones Industrial Average, up 263 points on Monday, is currently down around 119 points.

Investors in Europe are also taking a breather, with Germany’s Dax down around 94 points. News that the Greek talks with its creditors had broken up has not helped matters.

In the UK the FTSE 100 is down 113 points, with commodity companies under pressure as oil slid again (on the prospect of increased supplies from Iran if the nuclear negotiations come to a conclusion shortly).

There was also a bit of pre-election jitters after the campaign began in earnest after Monday’s dissolution of Parliament.

Still, the FTSE 100 has enjoyed its best three month stretch since March 2013 while the FTSEurofirst 300 has seen its best first quarter since 1998.

Updated

Angela Merkel and Francois Hollande are giving a press conference in Berlin now.

The two leaders say France and Germany have come closer in recent months, as they face terrorism in Paris and the Germanwings disaster together.

#Hollande: In the past few weeks the German-French 'friendship' has become more of a 'brotherhood.'

— Open Europe (@OpenEurope) March 31, 2015

They then fielded questions on Greece. Merkel said she wasn’t worried that Tsipras is heading to Russia next week.

And the chancellor is still optimistic that an economic reform plan will be agreed, but won’t be lured into setting a deadline:

#Merkel: I won't pin down any dates, programme runs to the end of April, the faster Greece responds, the faster we can help. Work ongoing.

— Open Europe (@OpenEurope) March 31, 2015

#Merkel: There is more work to do with the institutions after talks tomorrow. Confident that will be done.

— Open Europe (@OpenEurope) March 31, 2015

Hollande added that “too much time” has been lost already, so reforms need to be settled as fast as possible.

Summary: Greek deal still pending

Time for a recap.

Hopes of an breakthrough between Greece and its creditors before the Easter break are fading today.

After three days of negotiations over reform plans, Greek officials are heading back from Brussels to Athens without a breakthrough.

European Council president Donald Tusk has predicted that it could take until the end of April for Greece to satisfy its lenders that it has a credible economic programme. Until then, the government must struggle on without bailout funding.

Greek officials are remaining upbeat, telling us that sessions took place in a “very good climate”, adding:

“Both sides agreed that the process of fact-finding currently underway in Athens should be intensified.”

But without any new bailout funds, Athens faces a struggle to meet debt repayments including the €450m owed to the IMF on April 9th.

Analysts at Goldman Sachs are predicting a long haul:

Goldman Sachs after trip in Athens: The path to a political agreement between #Greece & its international creditors is still unclear #banks

— Efthimia Efthimiou (@EfiEfthimiou) March 31, 2015

Goldman Sachs: Those we speak with ultimately expect negotiations to continue until summer #Greece

— Efthimia Efthimiou (@EfiEfthimiou) March 31, 2015

Prime minister Alexis Tsipras has also made fresh overtures towards Moscow, telling the TASS newswire that

“Greece, as an EU member state, can be a link, a bridge between the West and Russia.”

Tsipras also reiterated that his government don’t agree with the sanctions imposed on Russia over the Ukraine crisis [Bloomberg has more details].

While in Germany, one of Angela Merkel’s allies has resigned in protest at Greece’s bailouts.

In other news...

-

Eurozone unemployment was higher than expected last month, with 11.4% of adults classed as jobless.

-

Prices across the eurozone continued to fall in March, with the consumer prices index falling by 0.1%. Core inflation dipped to 0.6%, suggesting price pressures remain weak.

-

But Britain’s economy is stronger than expected; the ONS has revised up its growth estimate for the last quarter of 2014 to 0.6%, from 0.5%.

Greek Euro parliamentarians are also expressing confidence that an agreement will be found in time, adds our correspondent Helena Smith in Athens.

Drawn-out negotiations were part of the horse-trading to be expected in any negotiation, they say.

Stelios Koulouglou, Syriza MEP, told the Guardian:

“The government has to be tough to reach a workable compromise.

I am actually quite optimistic.”

That seems to chime with what prime ministerial aides are saying today.

Vehemently denying that there was discord within the Greek representation, officials insisted that progress had been made in the negotiations. One insider said:

“The Greek side has well-founded positions ... in quite a few instances these positions have been accepted, while in others there are disagreements”.

The reforms leaked to the press had indeed been presented to creditor institutions but “do not express them in their entirety,” the aides said.

There were many more that had been put forward in far greater detail, they added.

That chimes with what the Greek media (usually well briefed in such matters) has been murmuring in recent days.

Ta Nea today has a double-page spread headlined: “The list’s visible and secret measures.” The daily lists 24 proposed reforms - six more than those announced by the government last week.

Updated

Greek officials: Fact-finding work will be 'intensified'

Over in Athens, officials are putting on a brave face on the situation, as technical team heads back from Brussels (see earlier post).

They say that despite the seeming lack of progress, talks were held in a “very good climate,” our correspondent Helena Smith reports.

One well-placed official said:

“The sessions took place in a very good climate with a mutual desire for an agreement to succeed. Greek representatives had the opportunity to present the list of reforms that the Greek government had prepared at length,”

The Greek side also had the opportunity to provide “clarification” to queries creditor institutions had over the workability of the reforms, the official added.

“Both sides agreed that the process of fact-finding currently underway in Athens should be intensified.”

While there was a desire for a compromise to be found as soon as possible, prime minister Alexis Tsipras’ leftist-led government had made clear any deal would not include recessionary measures but should be aimed at “kickstarting the economy.” HS

Money continues to flow out of shares today, and into safe-havens such as German debt.

The price of Germany’s two-year bonds has hit a new all-time high, pushing down the yield (the rate of return on the bond) below -0.25%.

Here we go again. German 2-year bond #yield sets another record low. -0.257%(!) pic.twitter.com/qLOr73vhUn

— jeroen blokland (@jsblokland) March 31, 2015

That means investors are paying more than the face value of the debt, and accepting they will make a loss when it matures (unless they sell it to someone else at an even higher price!).

The FTSE 100, though, is showing a triple-digit loss -- down 104 points or 1.5% at 6787.

A senior member of Angela Merkel’s Conservative bloc has resigned from his parliamentary seat, saying he cannot support the chancellor’s handling of the Greek debt crisis.

Peter Gauweiler also quit the vice-presidency of the conservative Christian Social Union (CSU) party, which is allied with Merkel’s CDU party.

Gauweiler said he was stepping down because:

“I have been publicly pressured to vote in the Bundestag for the exact opposite, on the grounds that I am a vice-president,”

“This is incompatible with my interpretation of the duty of a legislator.”

Gauweiler’s departure may be politically awkward for Merkel, but we should note that he has opposed Europe’s handling of its debt crisis for some years.

AFP dub him “a well-known eurosceptic and outspoken critic of euro bailout funds”. He has led several legal challenges against eurozone bailouts, including challenging the ECB’s OMT bond-buying programme which helped çalm the crisis in 2012.

Officials in Athens remain optimistic that a deal over Greece’s reform plans can be reached soon, according to Greek journalist Efi Egthimiou.

#Greece govt official say BG meeting ended last night, was in a very good mood, there's common will in order a deal 2b reached (@capitalgr )

— Efthimia Efthimiou (@EfiEfthimiou) March 31, 2015

The European Commission insist that negotiations with Greece have certainly not ended permanently.

EC spokeswoman Mina Andreeva told reporters in Brussels that talks with Greek officials are still ‘ongoing’ (even as they head back to Athens):

She said:

“The constructive talks are ongoing since Friday, but we are not there yet, so this is why the talks should continue.

The Eurogroup working group will discuss the matter at its next meeting.”

That working group (made up of deputy finance ministers) is due to hold a teleconference call on Wednesday afternoon to discuss the state of play:

Euro-area call on Greece scheduled for tomorrow @ 3pm CET

— Steve Collins (@TradeDesk_Steve) March 31, 2015

Updated

Greek negotiating team 'returning to Athens'

The technical negotiations between Greece and its creditors in Brussels have ended, it appears, without agreement on the country’s reform plan.

Greek insiders, though, say that progress has been made - although slowly - and talks could restart next week.

Reuters has the details:

Talks between officials from Greece and its EU/IMF lenders in Brussels have ended without a deal on the country’s reform plans and may continue next week, three Greek government officials said on Tuesday.

A fourth source close to the talks said the halt in negotiations was not a sign of a rupture but an indication of slow-moving progress in the discussions, which may be continued in Athens on Wednesday.

“The Brussels Group process has been concluded,” one of the government officials said, referring to the informal name of the EU/IMF lenders.

“Significant steps of progress were made. The technical teams will continue to collect data in Athens.”

Greek TV station TVXS has also heard that an agreement is close (which might come as news to Donald Tusk!)

#BrusselsGroup talks concluded; #Greece delegation returning to Athens, officials say agreemnt v close, even in next 1~2 days, @tvxs reports

— Yannis Koutsomitis (@YanniKouts) March 31, 2015

The lack of agreement has hit European stock markets, with all the main indices now in the red.

Updated

EUCO president: Greek deal before Easter unlikely

Back to the looming issue of Greece..... and European Council president Donald Tusk has warned that an agreement is unlikely before the Easter break, but could come by the end of April.

Speaking in Madrid, Tusk explained that the technical talks over Greece’s economic reforms are very complex, and thus:

I don’t foresee any breakthough before Easter.

The situation in Greece is under control at present, Tusk said, and declined to speculate on any “Plan B”.

We are focused on a successful financial deal for Greece, under the conditions agreed on 20 February, he added.

Here’s a video clip of Tusk speaking:

#Tusk @eucopresident in #Spain: Press conference extract on the reform programme of #Greece http://t.co/PhSM5f8EVr pic.twitter.com/PoV6aQXapC

— EU Council TV News (@EUCouncilTVNews) March 31, 2015

Updated

Here’s my colleague Katie Allen’s take on today’s UK GDP report:

The UK economy grew faster than expected in the final months of last year, helped by a long-awaited rise in exports, according to new official figures.

In a welcome boost to the Conservatives ahead of May’s election, GDP growth for the fourth quarter of 2014 was revised to 0.6%, up from a previous estimate of 0.5% and matching the pace of expansion in the third quarter. For the year as a whole, growth was upgraded to 2.8%, from 2.6%, and was the fastest expansion since 2006.

The Office for National Statistics said growth in real household disposable income also picked up while net trade moved from being a drag on the economy in the third quarter to boosting growth. However, business investment fell 0.9% on the quarter, casting doubts over the outlook for growth. There were also signs that households are dipping into savings to fuel spending, as the savings ratio dropped to 5.8% in the fourth quarter from 5.9% in the third quarter....

Updated

The pound has jumped against the euro since this morning’s flurry of data was announced.

Sterling is up around one eurocent at €1.377, a one-week high, as traders learn that UK growth was faster than expected in the last quarter.

The euro, though, has been hit by the news the unemployment was higher than expected, at 11.3%. And there is concern that the eurozone’s ‘core inflation’ (stripping out volatile elements like energy), fell to 0.6% this month.

It’s been a rough three months for the euro.

The euro is now down 11% against the dollar since January and heading for its worst quarter of all time. ECB trade-weighted € down 8% in Q1

— RANsquawk (@RANsquawk) March 31, 2015

The chancellor didn’t waste any time reacting to the new growth figures:

Hat trick of good news just out from ONS: GDP revised up, consumer confidence up, living standards up. #LongTermEconomicPlan working

— George Osborne (@George_Osborne) March 31, 2015

GDP revised upwards from 2.6% to 2.8% for 2014. Confirms UK as clearly fastest growing major advanced economy

— George Osborne (@George_Osborne) March 31, 2015

Andrew Sentance, senior economic adviser at PwC, suggests that the UK might be the fastest growing advanced economy this year, as in 2014.

Here’s his take on the new growth data:

“It is not surprising to see GDP being revised up for Q4 and for 2014 as a whole. A whole raft of other data points to a strong year for the British economy - including business surveys, car sales, retail sales and falling unemployment.

“The other encouraging thing about these figures is that they show that growth is being led by investment and exports - both of which rose by over 5% year-on-year in the final quarter of last year. Exports of services are also growing at over 5% with export-oriented services industries at the leading edge of the UK economic recovery. That is supported by the strong growth we are seeing in professional and business services - the strongest growing sector in the UK economy last year.

“The UK economy now appears to have more momentum going into 2015 than we earlier thought. So we should expect GDP forecasts for this year to be revised upwards on the back of this data. It is still entirely possible that the UK will head the G7 growth league in 2015, as we did last year.”

Kit Juckes of French bank Société Générale is alarmed to see Britain’s current account deficit hitting a record high, at 5.5% of GDP.

He writes:

Trade balance improved, but the investment income balance didn’t. The regional current account deficit with the EU (£28.3bn) is particularly ugly.

It’s going to take years to turn these trend round, which are born of low investment returns in Europe vs the UK and the long-term erosion of the overall net foreign asset position of the UK. Needless to say, such a big balance of payments hole is unhelpful at a time of political uncertainty, reflective of a country living beyond its means and really scary if the UK, or global economies were to slow sharply.....

Not that it’s a new trend....

Annual UK Current Account (percentage of GDP) 1948-2014. pic.twitter.com/aUABFFvG2h

— Duncan Weldon (@DuncanWeldon) March 31, 2015

Here’s some early expert reaction to today’s UK GDP report

Real household disposable income per head, consumption per head and GDP per head now all above where they were at last election

— Robert Peston (@Peston) March 31, 2015

Looks like real net disposable income per head is 0.2% up on Q2 2010, which is good, though other real income measures a bit of a way to go.

— David Smith (@dsmitheconomics) March 31, 2015

Per capita GDP, most simple proxy for living standards, still below crisis peak, but well above 2010 levels: pic.twitter.com/fa7pN2gpHa

— Faisal Islam (@faisalislam) March 31, 2015

Here’s a great chart showing unemployment in some of the eurozone’s larger economies over the last 25 years.

EZ unemployment rates pic.twitter.com/vnfti1hhqe

— cigolo (@cigolo) March 31, 2015

Eurozone unemployment at 11.3%

The Eurozone’s jobless rate was 11.3% in February, the lowest since May 2012 -- but also worse than expected.

Eurostat reports that unemployment across the euro area fell from 11.4% in January -- having revised up its previous estimate of 11.2%.

Unemployment across the wider EU dipped to 9.8% in February 2015, down from 9.9% in January 2015 and from 10.5% in February 2014.

According to Eurostat, the number of people unemployed in the euro area fell by 49,000 meaning 18.204m were out of work.

And, as usual, the lowest unemployment rates were recorded in Germany (4.8%) and Austria (5.3%), and the highest in Greece (26.0% in December 2014) and Spain (23.2%).

Eurozone unemployment at 11.3% in February: Greece: 26.0% Spain: 23.2% Italy: 12.7% France: 11.6% Germany: 4.8% http://t.co/llSUmcTYDe

— Markit Economics (@MarkitEconomics) March 31, 2015

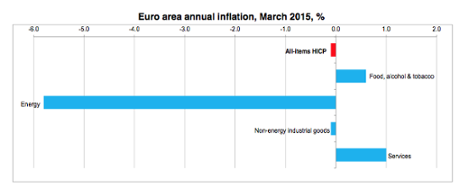

Eurozone inflation rises to minus -0.1%

Just in: Prices across the eurozone fell by 0.1% this month, up from -0.3% in February.

Once again, falling energy prices dragged down the cost of living, while service sector and food costs are rising.

Eurostat explains:

Services is expected to have the highest annual rate in March (1.0%, compared with 1.2% in February), followed by food, alcohol & tobacco (0.6%, compared with 0.5% in February), non-energy industrial goods (-0.1%, stable compared with February) and energy (-5.8%, compared with -7.9% in February).

Euro area annual inflation up to -0.1% in March 2015 - flash estimate from #Eurostat http://t.co/g8SLdY3BGS

— EU_Eurostat (@EU_Eurostat) March 31, 2015

Some political context:

Past decade or so, UK quarterly economic growth: pic.twitter.com/tVHKegsmer

— Faisal Islam (@faisalislam) March 31, 2015

Nice milestone RTRS-UK 2014 CURRENT ACCOUNT BALANCE 5.5 PCT OF GDP, LARGEST DEFICIT AS A PERCENTAGE OF GDP SINCE RECORDS BEGAN IN 1948

— Eric Burroughs (@ericbeebo) March 31, 2015

UK current account deficit hits record high

Britain’s current account is not for the faint-hearted.

The deficit in Britain’s trade and overseas investments has hit 5.5% of GDP, which is the largest deficit since records began in 1948.

So despite the recovery, the UK continues to import more than it exports, and is struggling to cover the gap with ‘invisible earnings’ and income from the assets it controls abroad..

Current account deficits don't matter until they matter. And then they can matter a lot...

— Duncan Weldon (@DuncanWeldon) March 31, 2015

Our economics editor, Larry Elliott, wrote recently about why this is such a concern:

One note of caution, the UK economy is still effectively smaller than before the financial crisis struck, once you adjust for population changes.

So we’re individually worse of than before the collapse of Lehman Brothers.

Updated

The Conservative Party must be cheering the news that growth was a little faster than previously thought in the last quarter:

UK growth upward revision a timely boost for Cameron ahead of Thursdays #leadersdebate #GE2015

— Joshua Raymond (@Josh_CityIndex) March 31, 2015

Britain’s service sector led the way in the last quarter, with growth of 0.9%.

Industrial production rose by 0.2%, while construction output shrank by 2.2%.

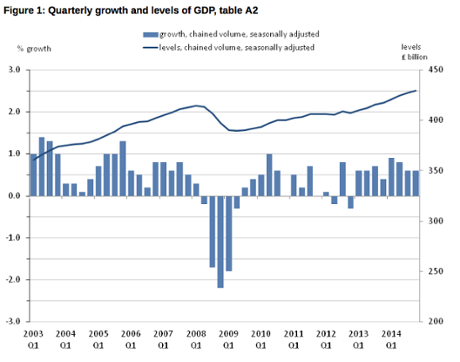

UK GDP: The key chart

UK growth revised up to 0.6%

Breaking: The UK economy grew by 0.6% in the last three months of 2014, higher than the 0.5% previously estimated.

The Office for National Statistics has also revised up its estimate for year-on-year GDP growth to 3.0%, up from 2.7%.

In addition, the ONS has also upped its estimate for GDP growth during 2014 as a whole, from 2.6% to 2.8% -- that’s the highest since 2006.

And it means UK GDP is now 3.7% above its pre-crisis peak, before the financial crisis.

More good news! UK GDP was estimated to have increased by 2.8% in 2014 (revised up 0.2%) #GBP

— Shaun Richards (@notayesmansecon) March 31, 2015

Updated

Stock markets enjoy best quarter in years

European stock markets are on track for their strongest quarterly growth in many years, despite Greece’s debt problems.

The launch of the ECB’s quantitative easing programme has helped fuel a remarkable stock market rally. Germany’s DAX has surged by 23% during 2015, which we think is the biggest quarterly jump since 2003.

The Italian FTSE MIB is close behind, up 22% despite the weakness of the Italian economy.

The wider FTSEurofirst 300, covering the biggest 300 companies across Europe, has gained almost 17% since the start of January.

That’s the best first-quarter performance in 17 years.

Europe stocks climb, head for best first-quarter gain since ’98

— Francine Lacqua (@flacqua) March 31, 2015

The rally hasn’t been confined to Europe either. China’s stocks has been on an absolute tear, with more retail investors flocking to the market. More than a million new share-dealing accounts were opened last week alone in China.

As Chris Weston of IG comments:

This is a sentiment driven market and when you see a record 1.14 million new A-share accounts last week you know that rampant speculation is underway.

Of top 5 equity markets, only 1 is European (and it's not in eurozone) pic.twitter.com/TbiRy4v7eF http://t.co/x7WnVZIFpm pic.twitter.com/6heogPcKib

— fastFT (@fastFT) March 31, 2015

(note: this graph is priced in US dollars, which dampens the size of Europe’s rally)

Updated

Disappointment as Italian jobless rate rises

Hopes that Italy’s economy was healing have just taken a knock.

Italy’s unemployment rate jumped to 12.7% in February, from 12.6% in January, new data shows.

And the youth unemployment rate has spiked too, to 42.6% from 41.2% in January.

That’s disappointing, given recent signs that Italian consumer confidence was rising after several years of recession or stagnation.

Italy's confidence up, Italy's unemployment up as well. The economy has stopped contracting, but still losing ground vis-a-vis its EU peers

— federico fubini (@federicofubini) March 31, 2015

German jobless rate hits record low

Just in: Germany’s unemployment rate has hit a new all-time low of 6.4%, as Europe’s largest economy continues to recover.

The seasonally adjusted jobless total has fallen by 15,000 this month, down to 2.798m. A bigger fall than expected.

*GERMAN UNEMPLOYMENT RATE FELL TO RECORD LOW OF 6.4% IN MARCH *GERMAN UNEMPLOYMENT FELL 15,000 IN MARCH; EST. 12,000 DROP

— Bloomberg Markets (@markets) March 31, 2015

Updated

Jeremy Cook, chief economist at World First, confirms that the lack of progress over Greece’s economic reforms is hurting the euro today.

Last night showed us that the Greek government and the European architects of Greece’s bailout program remain very far apart on what needs to be, and can be done for the former’s economy.

On every agenda item of what the austerity and bailout program needs, Greece disagrees. The program calls for a VAT increase on the tourism sector, the Greek government has said no. Pension reform has been shot down and public sector wages will remain protected.

The wider effect is that the budget surplus – the difference between what the government is spending and what it is receiving in the form of tax revenues – should be 3% of GDP in this year and 4% next year according to the program. Greece says they can do 1.5%.

Updated

Veteran investor Mark Mobius has offered Greece some much-needed solidarity today.

Mobius, who runs Templeton’s emerging markets fund, told Greek financial daily Naftemporik that:

“Greece will stay in the euro zone, there is no issue.....The stock market is cheap and we are buyers.”

Templeton's #MarkMobius tells the Greek press "Greece will stay in the euro zone. The stock market is cheap and we are buyers."

— Sally Bundock (@SallyBundockBBC) March 31, 2015

Good news for the town of Swindon this morning – Japanese automaker Honda has announced a £200m upgrade to its car plant.

That means Swindon will be ready to produce the next-generation five-door Civic, calming fears over the factory’s future.

Kingfisher to shut 60 B&Q stores

In the UK, Kingfisher has announced it will close around 60 B&Q stores as new CEO Véronique Laury implements her plans for the company.

Laury is speaking to reporters now, saying she hopes the impact on jobs will be ‘neutral’; some workers can be redeployed, with Kingfisher also opening more Screwfix outlets.

A few loss-making stores in Europe are also being shut.

Karen Witts, chief financial officer, warned that the French market (which Laury used to run) remains tough:

“In the short term, whilst we remain encouraged by the improving economic backdrop in the UK, we remain cautious on the outlook for France, our biggest market.”

Kingfisher says doing notably better in UK than in France. But it's closing 60 stores in the UK...

— Adam Parsons (@AdamParsons1) March 31, 2015

The City likes the plan -- Kingfishers shares have jumped by 4.5% in early trading.

Updated

Russia’s TASS news agency is running quotes from Alexis Tsipras, saying that Greece opposes the sanctions imposed on Moscow over the Ukraine conflict.

Bloomberg have picked them up too:

*GREEK PM TSIPRAS SAYS COUNTRY OPPOSES RUSSIA SANCTIONS: TASS

— Manus Cranny (@ManusCranny) March 31, 2015

#Tsipras says #Greece can be bridge between Russia, West: Tass

— Francine Lacqua (@flacqua) March 31, 2015

It’s another reason to be cautious about the euro, suggests Ilya Spivak, Global Macro Strategist at DailyFX.com.

If the Tass report is accurate and Tsipras just broke rank with EU, might hint he sees nothing left to lose, i.e. no deal on bailout

— Ilya Spivak (@IlyaSpivak) March 31, 2015

The euro is likely to keep falling, thanks to Greece’s debt problems and the ECB’s new stimulus package.

That’s according to Shusuke Yamada, a Tokyo-based currency strategist at Bank of America Merrill Lynch, who told Bloomberg that:

“Markets are becoming more sensitive to the Greek issue.

In addition, the European Central Bank’s quantitative easing is keeping downward pressure on the euro. Fundamentals point to euro selling.”

Euro hit by Greek bailout brinkmanship

The euro has fallen back this morning after Greece failed to agree a package of economic reforms with its lenders on Monday, as hoped.

The single currency has fallen half a cent against the US dollar, hitting $1.078, as traders reacted to last night’s events in the Athens parliament, and the prospect of more deadlock ahead.

Ready to rumble: EURUSD breaks below 1.0800. Now Euro trades at $1.0789. pic.twitter.com/3KsDLBvBH0

— Holger Zschaepitz (@Schuldensuehner) March 31, 2015

As we covered in last night’s liveblog, prime minister Alexis Tsipras insisted that he would not unconditionally surrender to Greece’s creditors. He declared:

It is true that we are seeking an honest compromise with our lenders but don’t expect an unconditional agreement from us.”

Tsipras vowed to stop ‘the bleeding’ in Greece, and repeatedly argued that the country needs a new debt restructuring deal. Greece has a simple choice, he argued, between surrendering, or changing the policies that have caused such economic misery.

He pledged to end the ‘pillaging’ of the middle classes, and revealed that a new clampdown on unpaid taxes had already delivered €100m.

But his speech lacked clear details about the reform plan that Greece is putting together in negotiations with its creditors over the last few days.

Tsipras also urged opposition politicians to back him, but was criticised by former PM Antonis Samara for damaging Greece’s relations with the rest of Europe and threatening the recovery.

ND's Samaras tells Greek govt: 'We will support you, but not on anything. If you push the country back to recession and deficits, we won’t'

— Kathimerini English (@ekathimerini) March 30, 2015

Samaras says Tsipras imagined he'd get money without terms but ended up getting terms without money #Greece

— MacroPolis (@MacroPolis_gr) March 30, 2015

Analysts fear that Greece will run out of cash this month unless it receives a cash injection from its lenders.

As Jonathan Sudaria of Capital Spreads puts it:

“The brinkmanship continues as both sides continue to stare at each other over the political void. Despite Greece hurtling towards bankruptcy, an agreement continues to evade.”

Ian Williams of Peel Hunt agrees, saying:

The euro is under renewed pressure on persistent concerns about Greece.

The Agenda: Eurozone inflation and unemployment data due

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

There’s a lot of talk at present that Europe’s economy is healing, and we’ll get a proper healthcheck today with new inflation data for this month, and the February unemployment report, both at 10am BST.

Economists predict that eurozone prices fell by just 0.1% year-on-year, an improvement on February’s 0.3% decline. If so, this period of negative inflation (or “DEFLATION!!” if you have alarmist tendencies) may be ending, now oil prices appear to have stabilised.

The eurozone jobless rate, though, is expected to hover around 11.2%, around twice the level in the UK and US. And we’ll probably see the usual sharp regional differences, with Germany’s economy improving and Italy lagging behind.

We also get the third estimate of UK GDP for the fourth quarter of last year, probably confirming that growth slowed to 0.5%. There’ll also be new details of how the economy fared during the quarter. That’s at 9.30am BST.

And overshadowing everything is Greece, which has still to agree a programme of economic reforms with its creditors.

I’ll be tracking all the main events through the day....

Updated