Ratings agency Standard & Poor’s has upgraded Cyprus from B to B+ with a stable outlook, after a strong budgetary performance from the country.

S&P forecasts that the country’s real GDP will contract by around 3% in 2014 compared to earlier predictions of a 3.8% decline.

But it said there was a risk that any further EU sanctions on Russia could negatively affect tourism to the country.

Speaking of Russia, Moody’s may have downgraded the country a few days ago, but S&P has kept it at BBB-. However it warned a downgrade could follow if more sanctions are imposed on the country over its actions in Ukraine.

And on that note, its’s time to close up for the evening. Thanks for all your comments and we’ll be back on Monday.

Updated

European markets end week on downbeat note

It was a much calmer week after the panic seen during the previous five trading days, but European markets still ended, for the most part, in negative territory on Friday. Worries about Chinese growth, concerns about how the ECB’s plans to boost the flagging eurozone economy will work out, as well as the first confirmed case of Ebola in New York all combined to unsettle investors ahead of the weekend. Even an opening rise on Wall Street failed to inspire markets on the other side of the Atlantic. So the closing scores showed:

- The FTSE 100 finished down 30.42 points or 0.47% at 6388.73, still up on the week for the first time since mid September

- Germany’s Dax dipped 0.66% to 8987.80

- France’s Cac closed 0.69% lower at 4128.90

- Italy’s FTSE MIB added 0.31% to 19,495.68

- Spain’s Ibex ended up 0.05% at 10,339.3

On Wall Street the Dow Jones Industrial Average is currently 98 points or 0.59% higher.

And after the Draghi comments, Reuters has lines on German chancellor Angela Merkel’s response:

- 24-Oct-2014 16:16 - BRUSSELS - GERMANY’S MERKEL SAYS ECB’S DRAGHI MADE CLEAR TO EU LEADERS THAT STRUCTURAL REFORMS AND IMPROVING INVESTMENT CLIMATE WAS KEY FOR EURO ECONOMY

- 24-Oct-2014 16:17 - GERMANY’S MERKEL SAYS BELIEVE CLOSER ECONOMIC COORDINATION IN EURO ZONE IMPORTANT, DRAGHI AGREED WITH THIS

- 24-Oct-2014 16:19 - GERMANY’S MERKEL SAYS DRAGHI MADE CLEAR THAT MONETARY POLICY CAN ONLY DO SO MUCH, FISCAL POLICY MUST REACT AT SAME TIME

- 24-Oct-2014 16:22 - GERMANY’S MERKEL SAYS UK’S CAMERON DID NOT SAY HE WOULD NOT PAY ADDITIONAL EU BILL, JUST QUESTIONED THE DEADLINE FOR PAYMENT

- 24-Oct-2014 16:25 - GERMANY’S MERKEL SAYS COULD IMAGINE MOVING FORWARD REVIEW OF MEDIUM-TERM EU BUDGET PLAN TO SEE HOW TO BETTER USE EU FUNDS TO BOOST INVESTMENT

- 24-Oct-2014 16:27 - GERMANY’S MERKEL SAYS DOES NOT ENVISION USING ESM FUNDS TO BOOST INVESTMENTS IN EU

- 24-Oct-2014 16:29 - GERMANY’S MERKEL SAYS VERY MUCH APPRECIATES MARIO DRAGHI’S WORK IN THE EURO ZONE, WANTS GOOD COOPERATION WITH ECB

- 24-Oct-2014 16:31 - GERMANY’S MERKEL SAYS DOES NOT WANT TO CALL INTO QUESTION FREE MOVEMENT OF PEOPLE PRINCIPLE WITHIN THE EU, BUT THAT DOES NOT MEAN THERE ARE NO PROBLEMS

- 24-Oct-2014 16:33 - GERMANY’S MERKEL SAYS ECB’S DRAGHI DID NOT MAKE ANY ECONOMIC POLICY SUGGESTIONS FOR GERMANY

Germany's Merkel on the wires looks like a PR exercise in trying to deflect the gossip re bad blood between Germany and ECBs Draghi

— Live Squawk (@livesquawk) October 24, 2014

And here’s the full Reuters story on ECB president Mario Draghi’s latest thoughts on the eurozone economy and the measures needed to boost it, as given to eurozone leaders over lunch:

France and Italy renewed their commitment to reform their economies on Friday in the hope of winning more time to bring their public finances in order but the ECB’s president warned more needed to be done to avoid “a relapse into recession”.

After the bloc’s revival came to a halt in the second quarter, France and Italy want to shift course away from the spending cuts that marked the bloc’s response to the 2009-2012 crisis. Germany says debt discipline must continue.

Seated around a large oval table in the EU summit’s red marble building, European Central Bank President Mario Draghi told eurozone leaders over lunch that more needed to be done.

“We avoided the collapse of the euro with a joint effort. Now our focus should be to act jointly again to avoid a relapse into a recession,” Draghi said, according to his spokesman, who quoted from his speech. “Hope is not a strategy.”

He said a coherent strategy for economic growth had to involve “concrete and credible” structural reforms.

Laying out a four-pronged strategy, Draghi emphasised that monetary policy was only one part of an economic revival plan, with the others being reforms, sound public finances and healing the bloc’s sick banks.

But despite Draghi’s firm words, the summit underscored how the eurozone has few quick fixes for near record unemployment, leaving it in search of billions of euros for spending that Berlin wants to see come from the private sector.

German chancellor Angela Merkel said no country with a national debt greater than its economic output should be borrowing more, diplomats said.

According to people in the room, Merkel said record low interest rates gave the euro zone “room to breathe” and that a mix of private investment, fiscal discipline and openness to fast-growing Asian economies was the way forward.

Merkel also said a proposed free-trade deal with the United States, which is increasingly unpopular in Europe, was crucial.

But such measures could take years to bear fruit, while the euro zone’s poor performance is becoming a wider concern, with the United States and the International Monetary Fund worrying that the bloc that makes up a fifth of the world economy is a drag on global prosperity.

Updated

Some comments from ECB president Mario Draghi have hit the wires. Courtesy Reuters:

- 24-Oct-2014 15:38 - BRUSSELS-ECB’S DRAGHI TELLS EU LEADERS JOINT EFFORT NEEDED TO AVOID “RELAPSE INTO RECESSION”

- 24-Oct-2014 15:40 - DRAGHI-EURO ZONE COUNTRIES WITH FISCAL SPACE SHOULD CONSIDER STIMULATING DEMAND -SPOKESMAN

- 24-Oct-2014 15:40 - DRAGHI SAYS EU BUDGET RULES MUST BE CREDIBLY UPHELD AS POLICY ANCHOR -SPOKESMAN

- 24-Oct-2014 15:41 - DRAGHI REPEATS ECB READY TO USE OTHER UNCONVENTIONAL MEASURES IF NEEDED, DID NOT SPEAK OF DEFLATION - SPOKESMAN

- 24-Oct-2014 15:43 - DRAGHI URGES ALL EURO ZONE GOVERNMENTS TO PRESENT STRUCTURAL REFORM TIMETABLE BY DECEMBER EU SUMMIT

- 24-Oct-2014 15:44 - DRAGHI-WOULD BE WORRIED IF PROLONGED LOW INFLATION LED TO SECOND ROUND EFFECTS IN WAGE AND PRICE SETTING

Draghi has lost it with his stimulus remarks. Germans will be furious.

— MineForNothing (@minefornothing) October 24, 2014

Updated

Tesco now has the full set of ratings agency downgrades in the wake of Thursday’s results.

Following Moody’s and Fitch, Standard and Poor’s has cut its rating from BBB to BBB-, with a negative outlook. This reflects the view that Tesco “will continue to experience tough trading conditions and that its credit metrics are unlikely to improve.”

Updated

Twenty five banks are set to fail the ECB’s stress test when the results are released on Sunday, Bloomberg is reporting. It said:

Twenty-five lenders in the European Central Bank’s euro-area bank health check are set to fail the regulator’s Comprehensive Assessment, according to a draft communique of the final results, seen by Bloomberg News.

One-hundred-and-five banks are shown passing the review, according to the draft statement. Of the lenders that failed, about 10 will still face capital shortfalls they need to plug, according to a person with knowledge of the matter, who asked not to be identified because they weren’t authorized to speak publicly. That figure is likely to change as talks continue before the final results are published Oct. 26, said the person.

Full story here:

ECB Set to Fail 25 Banks in Review, Draft Document Shows

Updated

US new home sales edge higher.

And in the event sales of new US single family homes rose 0.2% month on month to a six year high of 467,000 in September.

But the rise only came about because August’s figure was revised down from 504,000 units to 466,000.

As previously pointed out, new home sales - which account for around 8% of the market - tend to be volatile and revisions are not unusual.

The September figure is up 17% on a year ago, but is slightly below the 470,000 predicted by economists.

Following the report, the Dow Jones Industrial Average has reversed early gains and is currently nearly 5 points lower.

US new homes sales are due, with a month on month fall of 6.8% expected.

Before making too much of new home sales (10 am ET), remember: small sample & high volatility. Aug confi interval for m/m was +/-16%.

— Jed Kolko (@JedKolko) October 24, 2014

Wall Street is open and despite disappointing results from Amazon, markets are moving higher, helped by good gains by Microsoft after its figures.

The Dow Jones Industrial Average is up 49 points or 0.29% in early trading, in contrast to European markets which are still in negative territory, on worries about Ebola, poor Chinese property figures and uncertainty ahead of the ECB bank stress tests, the results of which are due to be released on Sunday.

No further comment needed:

Satire truly dead when Greece forced to borrow money to pay EU extra €89m on account of economic over performance: pic.twitter.com/mafPNKRzr7

— Faisal Islam (@faisalislam) October 24, 2014

Back to the GDP figures, and my colleague Phillip Inman says that despite the economy growing chancellor George Osborne has cause for concern:

George Osborne is clearly worried. Going into a pre-election war-gaming huddle with his advisers, the economic numbers that once sang a happy tune and are so crucial to victory, now sound a little discordant.

It seems churlish to strain for the bum notes in the latest GDP figures. All parts of the economy are growing, with the exception of agriculture. And growing more strongly than they are in any of the major European economies.

But it is the chancellor’s words that set off the alarm bells. He said: “If we want to avoid a return to the chaos and instability of the past, then we need to carry on working through our economic plan that is delivering stability and security.”

Adopting the word “chaos” is at once interesting and alarming. He seems to be saying that any other path than the one he has chosen will bring with it a swirling storm of instability.

Billing himself as Lord Protector, Osborne risks overstating his case, especially when the GDP numbers are so strong. Growth is moderating, but most surveys report that businesses remain confident about the recovery and continue to hire more staff. As a result, unemployment continues to fall.

So what can he be worried about? There is the three months of restrained housing market activity. If it’s true, and we don’t fully understand the link, that much of the recovery is connected to the increase in property buying, then any slowdown is a cause for concern. Except the chancellor wanted the housing market to cool. And his policies are largely the reason banks are refusing to dole out loans after he gave regulators instructions in April to clampdown on risky mortgage lending.

A slowdown in housebuilding was also a logical knock-on effect, given that a majority of homes are constructed by a private building sector keen to maintain its extraordinary profit levels.

We know he is worried about the slowdown in exports, which didn’t take off four years ago, as he had expected. The eurozone’s impending recession is largely to blame, but a lack of support to exporters, particularly multimillion-pound credit insurance, has also proved a barrier.

However, the crucial issue is the government’s finances, which have worsened this year despite the strong recovery. For a man with the electoral cycle stamped on his DNA, it is tragic that businesses and workers are not paying much extra tax.

The full piece is here:

George Osborne’s choice of words are sounding the alarm bells

Here’s our latest take on the demand for more money from Britain and others for the EU budget:

Europe’s finance ministers will convene an emergency meeting following the disclosure of a demand for some countries, including Britain, to contribute billions more to the EU budget, the prime minister’s spokesman said.

David Cameron believes the demand for £1.7bn from Britain is “unacceptable” and has secured a gathering of Treasury ministers to discuss the recalculation of contributions which have hit the UK, Italy, and the Netherlands with additional bills, while France and Germany are to receive a rebate.

The meeting is a minor victory for No 10 following Thursday night’s disclosure that Britain has been ordered to pay the money because its economy is performing better than others in the EU.

Full story here:

David Cameron labels EU demand for extra £1.7bn from UK unacceptable

I'm angry at the sudden presentation of a €2bn bill to the UK by the EU. It's an appalling way to behave and I won't be paying it on Dec 1st

— David Cameron (@David_Cameron) October 24, 2014

Updated

Over in the US, and Ford has reported a 34% drop in third quarter profits to $835m, but this was higher than Wall Street analysts had been expecting.

The drop was partly due to the costs of introducing its F-150 aluminium bodied pickup truck, with its Dearborn plant in Michigan shut for five weeks to prepare for the launch. There was also a $160m charge relating to restructuring in Europe.

Updated

More on the EU budget demand on Britain:

EU leaders agree PM's request for talks over missing 1bn. Commission wants cash in time for Christmas- imagine what you cd buy with that!

— Laura Kuenssberg (@bbclaurak) October 24, 2014

Shire reports 60% rise in income

Back in the corporate world and Shire - recently jilted by US predator AbbVie after a proposed clampdown on tax inversion - has just revealed a 32% jump in third quarter revenues to $1.597bn and a 60% rise in operating income to £717m.

After what it called a very strong performance Shire has raised its guidance and now expects a rise in earnings per share in the high 30% range. Previously it had been expecting low to mid 30% growth.

As part of its defence against AbbVie it said it planned to double sales to £10bn by 2020.

Shire’s shares are currently leading the FTSE 100, recovering from earlier falls to rise 125p or 3% to £40.20.

Updated

Meanwhile there is interest in the GDP figures from an unexpected source:

A spider just photobombed Ed Balls pic.twitter.com/d7lCux1WyM

— BBC News (UK) (@BBCNews) October 24, 2014

Katie Allen: UK economic growth slows to 0.7%

If you’re just joining us, or would like a recap, here’s Katie Allen’s full story on today’s GDP data:

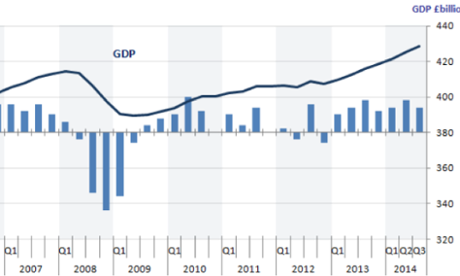

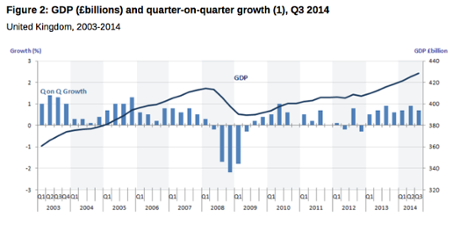

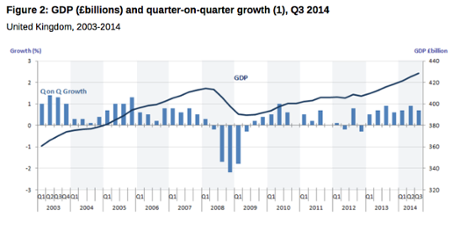

The UK economy grew at a slower pace in the third quarter but was still up a solid 0.7%, more than most other advanced economies.

The slowdown from growth of 0.9% in the second quarter was in line with most forecasts. But after recent economic indicators showing a weaker housing market, and slower manufacturing and consumer spending, some had feared growth could be weaker. Relief in financial markets at the figures, which confirmed seven consecutive quarters of growth, gave the pound a boost in morning trading.

“While today’s figures show that growth in the third quarter was modestly lower than in the second quarter, we do not consider that the recovery is losing serious momentum,” said Philip Shaw, economist at Investec.

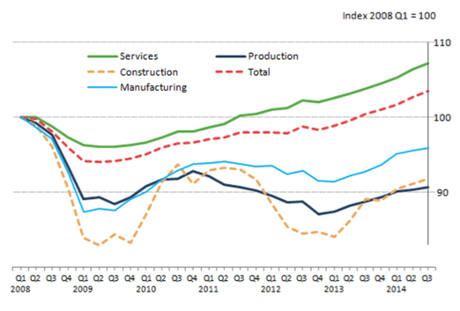

The Office for National Statistics said growth in output from the UK’s dominant services sector slowed from July to September and that manufacturing grew at the slowest pace for 18 months.

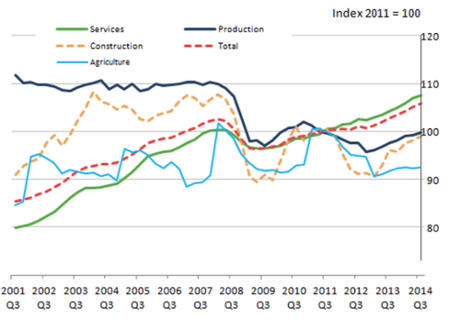

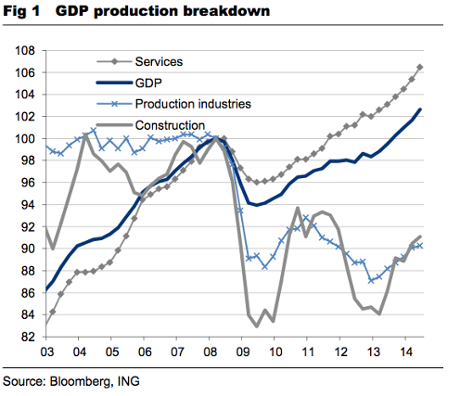

Services remained far and away the biggest driver of growth, followed by production, which includes manufacturing. Construction growth picked up in the third quarter, chiming with reports that housebuilding is at its strongest since 2007.

Compared with a year ago, GDP was up 3%, down from annual growth of 3.2% in the second quarter.

The solid growth figure is not all good news, however, after it emerged that Britain has been told it must pay an extra €2.1bn (£1.7bn) into the European Union budget by the end of next month because it is performing better than its European neighbours.

Rob Carnell, economist at ING Financial Markets, said the performance was “very respectable”, though he added: “The UK chancellor may view this as a mixed blessing, after being given a bigger bill for the EU budget thanks to the UK’s relative outperformance of its European Union peers.

“This will be especially irksome since despite the stronger growth figures, there has not yet been an accompanying improvement in the UK public finances to match.”

The Treasury welcomed the latest figures but was quick to point to pressures from outside the UK weighing on business activity.

Chancellor George Osborne said: “Today’s strong growth figures show that the UK continues to lead the pack in an increasingly uncertain global economy. With all the main sectors of the economy growing it’s clear that our recovery is broadly based.

“But the UK is not immune to weakness in the euro area and instability in global markets, so we face a critical moment for our economy.”

Despite a more balanced recovery, services still dominate providing >85% of #GDP growth since the crisis. [2/2] pic.twitter.com/3mvwkVYKrf

— Daiwa Europe (@DaiwaEurope) October 24, 2014

Business groups have also warned that manufacturers in particular are feeling the strains in the eurozone, where some economies are contracting and others are grappling with deflation.

The CBI said this week that falling demand for British goods abroad weighed on manufacturers in October. A stronger pound also dented UK competitiveness and export orders dropped for the first time in 18 months.

The manufacturers’ organisation EEF said the sector was still on track to grow at its fastest pace since 2010 and domestic demand remained healthy.

However, EEF senior economist Felicity Burch said: “Today’s estimates confirm the economy has slowed, with little surprise that export-intensive sectors have been most affected. After strong growth in the first six months of the year, the pace of growth in manufacturing has also slackened as a result of weaker demand from key markets including Europe and China.”

Taken as a whole the UK’s economy is now 3.4% above its pre-crisis peak in the first quarter of 2008. But in a blow to the government’s ambitions to secure more balanced growth, it is only the services sector that has exceeded its pre-crisis peak. Manufacturing and construction still have some way to go to make up lost ground, the ONS confirmed today.

“Although there has been widespread growth across all major components of GDP since the start of 2013, the service industries remain the largest and steadiest contributor to economic growth, and the only component of GDP where output has exceeded its pre-downturn peak,” statisticians said.

The economy also remains below its pre-crisis level when measured by head of population.

John Hawksworth, chief economist at PwC points out that while total GDP is now around 3.4% higher than its pre-recession peak, the population has also grown by around 4.5% over the same period.

“Average GDP per person is therefore still around 1% lower in real terms than before the recession, which helps to explain why many people may feel that there is some way to go before the downturn is truly over,” he said.

UK headline growth looks not bad. But GDP per capita shows UK has had the worst post-crisis recovery in the G10: pic.twitter.com/CTYMMVqKpA

— Jamie McGeever (@ReutersJamie) October 24, 2014

And I’m handing over to Nick Fletcher now.... Cheers, GW

This is curious... George Osborne has apparently denied that living standards have fallen, in an interview with ITN.

But when I point out living standards are falling as wages have fallen behind inflation he says "I don't accept that."

— Richard Edgar (@ITVRichard) October 24, 2014

There’s no dispute that wages have been lagging inflation for the last five years....

UK @GeorgeOsborne denies living standards falling as wages lag inflation. It's 5 years and counting. HT @ITVRichard pic.twitter.com/Dh8qDvtz8e

— Jamie McGeever (@ReutersJamie) October 24, 2014

I think they were playing Monopoly last night at #EUCO. I found this on the floor by David's seat. pic.twitter.com/NWcaEThsgd

— Berlaymonster (@Berlaymonster) October 24, 2014

Over in Brussels, the EU summit continues to be dominated by the demand for an extra £1.7bn from Britain due to its recent economic success.

David Cameron has demanded an emergency meeting to discuss it:

At EU Summit Cameron interrupts meeting to demand emergency finance minister's meeting to discuss UK facing a £1.7 bln budget surcharge.

— Gavin Hewitt (@BBCGavinHewitt) October 24, 2014

The Dutch, who are also facing a higher bill, are unimpressed:

#UK2bn dutch government says it is surprised and has lots of questions for the commission

— Ian Traynor (@traynorbrussels) October 24, 2014

While George Osborne says he only found out on Tuesday:

.@george_osborne tells me he first heard abt EU €2.1bn bill on Tues. It was a decision made by “junior officials” in the “bowels” of the EC

— Ed Conway (@EdConwaySky) October 24, 2014

George Osborne tells me EU demand for cash is "just not an acceptable way for an organisation to behave"

— Richard Edgar (@ITVRichard) October 24, 2014

Updated

On the economy, chancellor tells me: "These GDP numbers, 0.7%, 0.9% what do they mean? Economic security, more jobs a brighter future."

— Richard Edgar (@ITVRichard) October 24, 2014

George Osborne’s trip to Derby is part of a push to encourage more women into the workplace.

The government is aiming to get almost 500,000 more women in the workplace by the beginning of 2016, which would push Britain’s female employment rate up to match Germany’s.

As the Telegraph explains here, the Treasury said it will achieve the target by increasing access to childcare across the country

Just in; photos of George Osborne in Derby, on the second day of his trip to meet women working across the UK economy.

Updated

The chancellor couldn’t resist his favourite hashtag, on a trip to the East Midlands.

Am @ToyotaUK in Derby to meet staff & hear what more #LongTermEconomicplan can do to support them

— George Osborne (@George_Osborne) October 24, 2014

Osborne has just held some interviews with the broadcast media, so we should have new quotes soon:

Just been chatting to this bloke. More on @SkyNews presently pic.twitter.com/2cnBfVSyLQ

— Ed Conway (@EdConwaySky) October 24, 2014

Updated

Today’s GDP figures are important, but they’re only one measure of the economy, alongside wage growth, unemployment, and the deficit.

My colleague Angela Monaghan has rounded up the charts that tell the story:

John Hawksworth, PwC’s chief economist, makes an important point:

Total UK GDP is now around 3.4% higher than its pre-recession peak in Q1 2008, but the population has also grown by around 4.5% over this period.

Average GDP per person is therefore still around 1% lower in real terms than before the recession, which helps to explain why many people may feel that there is some way to go before the downturn is truly over.”

Hawksworth also reckons that growth will slow next year, to around 2.5% compared to 3% or so in 2014.

But this will still be one of the best growth performances in the G7 in 2015, behind only the US and possibly Canada, following the UK’s chart-topping results in 2014.

Ed Balls responds to the GDP data

Ed Balls, Labour’s Shadow Chancellor, has responded to today’s GDP data with a broad-brush attack on the Tories (and no specific reference to the actual report).

“For all George Osborne’s claims that the economy is fixed most people are still not feeling the recovery. Working people are over £1600 a year worse off since 2010 and these figures now show a concerning slowdown in economic growth too.

“We need a strong and balanced recovery that works for all working people, not just a few at the top. But under the Tories we have stagnating wages and too many people in low-paid jobs which, as the OBR said last week, are leading to rising borrowing. This plan isn’t working for working people.

“And under this government house building is it at its lowest level since the 1920s, business investment is lagging behind our competitors and exports are way off target.

“Labour’s economic plan will make Britain better off, create more good jobs and earn our way to higher living standards for all.

“We will get 200,000 new homes built a year, raise the minimum wage, cut business rates and expand free childcare for working parents. And we will balance the books as soon as possible in the next Parliament, but do so in a fairer way by reversing David Cameron’s tax cut for millionaires.”

The pound is broadly unchanged, up just 0.04% at $1.6035.

There’s very little reaction to today’s data in the financial markets, confirming that investors and traders had expected a growth figure of around 0.7%.

As mentioned earlier, today’s GDP report is only based on two month’s data.

And Berenberg bank suggests the ONS may have been too optimistic in its assumptions about September:

The number crunchers have assumed construction rises 4.0% month-on-month, bouncing back from August’s surprise 3.9% fall, industrial production rises 0.6% (mom) – the strongest since February – while services rise 0.5% mom, the strongest since March.

If those assumed growth rates turn out to reflect the truth, then output will head into Q4 on strong foundations. The much discussed UK slowdown will not be evident in September in that case. Alternatively, there may be downward revisions to come....

Although Britain’s growth has slowed, today’s data will probably create sense of relief in Westminster and amongst UK policy makers, says Jon Pryor of City firm Investec.

“The 0.7% growth keeps the country on a 3% annual growth rate, which keeps the UK at the top of the G7 nations.

This should calm fears for now that the slowdown in Europe and deflation fears around the globe are not such an immediate threat to the UK economy.”

Despite a more balanced recovery, services still dominate providing >85% of #GDP growth since the crisis. [2/2] pic.twitter.com/3mvwkVYKrf

— Daiwa Europe (@DaiwaEurope) October 24, 2014

Felicity Burch, Senior Economist at EEF, the manufacturers’ organisation, says UK manufacturers have suffered from weaker overseas demand.

“Today’s estimates confirm the economy has slowed, with little surprise that export-intensive sectors have been most affected.

After strong growth in the first six months of the year, the pace of growth in manufacturing has also slackened as a result of weaker demand from key markets including Europe and China.

But 2014 has still been a decent year:

“Nonetheless, the domestic economy remains relatively upbeat, and manufacturing sectors with strong exposure to the UK should do particularly well. Manufacturing is still on track to grow at its fastest pace since 2010.”

Looking into the data, Britain’s manufacturing sector grew by just 0.4% during the last quarter.

That is the weakest quarterly growth since the first quarter of 2013.

The weaker global outlook does appear to be hurting UK factories, as George Osborne suggests. Figures yesterday showed that demand for British exports was slowing.

Osborne uses the "Not immune" phrase with relation to the eurozone, whilst welcoming "strong" GDP number

— Faisal Islam (@faisalislam) October 24, 2014

Britain will struggle to grow faster than 0.7% per quarter unless conditions improve at home and abroad, says Jeremy Cook, chief economist at currency exchange company World First.

“Headwinds from the current slowing of output in Europe and China are obvious dangers to the UK’s growth picture.

With real wages staying determinedly negative at the moment, there are concerns about how much farther domestic demand levels can be pushed.

TUC: A tale of two economies

The TUC hammers home the point that wages aren’t keeping up with inflation:

General Secretary Frances O’Grady says:

“It’s a tale of two economies – a few people at the top are thriving, but most workers’ wages are still in decline.

“This kind of growth is fragile because businesses can’t keep prospering if their customers have less money to spend.

“George Osborne needs a clear strategy for a wages-led recovery or it will be the deficit that continues to grow while the economy runs out of steam.”

Updated

ING: Public finances lagging behind GDP

Although Britain has posted quite respectable growth in the last year, this hasn’t yet fed into the public finances - with borrowing around 10% higher this year than last.

And Rob Carnell of ING reminds us that Britain already faces a larger bill from Brussels, to reflect its stronger economic performance.

UK 3Q14 GDP has come in at a very respectable 0.7%QoQ, taking the year on year growth rate to 3.0% - in line with market expectations. However, the UK Chancellor may view this as a mixed blessing, after being given a bigger bill for the EU budget thanks to the UK’s relative outperformance of its European Union peers. This will be especially irksome since despite the stronger growth figures, there has not yet been an accompanying improvement in the UK public finances to match.

Britain’s weak wage growth is one factor weighing on the public finances, meaning income tax receipts have barely grown this year.

Read the report yourself.

You can see the GDP report, here on the ONS website.

Services still powering UK economic growth, 3rd quarter GDP data shows pic.twitter.com/wL4QFt2T99

— jeremy warner (@JeremyWarnerUK) October 24, 2014

George Osborne: UK leads pack in 'increasingly uncertain global economy'

George Osborne, chancellor of the Exchequer, strikes a cautious tone as he welcomes today’s GDP figures:

“Today’s strong growth figures show that the UK continues to lead the pack in an increasingly uncertain global economy.

With all the main sectors of the economy growing it’s clear that our recovery is broadly based. But the UK is not immune to weakness in the euro area and instability in global markets, so we face a critical moment for our economy. If we want to avoid a return to the chaos and instability of the past then we need to carry on working through our economic plan that is delivering stability and security.”

Another chart, underlining how Britain’s recovery since 2011 has been led by the services sector:

Danny Alexander, Lib Dem Chief Secretary to the Treasury, says the recovery is now “well established”, giving Britain “good momentum” to cope with global uncertainty.

And with an eye to next May’s election, he says:

Our plan is working and we need to stick to it. The families and businesses of Britain whose hard work is powering this recovery will judge harshly any Party that threatens to squander this progress. Britain can’t forget the deficit or believe unfunded promises. Being sensible with the nation’s money is the bedrock of the Liberal Democrat approach.

We will keep a steady hand on the economic tiller because that is the only way to produce the stronger economy and fairer society that Britain needs.’

Updated

This chart, tweeted by the ONS, shows how Britain’s dominant services sector provided the bunk of the growth.

It’s disappointing that industry couldn’t grow as fast; despite hopes of rebalancing the economy.

UK #GDP grew 0.7% in Q3, driven by services (+0.7%) http://t.co/JMF7XBwVjN pic.twitter.com/2CLkdHHWAR

— ONS (@ONS) October 24, 2014

Britain’s economy is now 3.4% higher than its previous pre-crisis peak (achieved in autumn 2008, before the financial crisis plunged the world economy into crisis)

Some historical context:

On an annual basis, UK GDP is 3.0% higher than a year ago. That outpaces our major European rivals (France, for example, hasn’t grown for the last six months)

UK economy grows by 0.7% -- the details

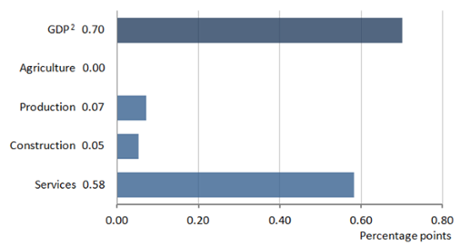

All four sectors of the UK grew in the last quarter.

- The services sector grew by 0.7%

- Industrial production rose by 0.5%

- Construction output rose by 0.8%

- And agriculture grew by 0.3%

So, the UK recovery has slowed, largely as economists had expected. Not a major shock.

UK GDP FIGURES RELEASED

Breaking: The UK economy grew by 0.7% in the third quarter of 2014, according to figures just released by the Office for National Statistics.

That follows growth of 0.9% in the second quarter of the year, so the UK’s growth has slowed.

Five minutes to go until we learn how fast the UK grew in the last quarter (if you’re just joining us, our introduction on today’s growth figures is at 8am).

The Office for National Statistics have briefed newswire reporters at a ‘lock-in’ in London, so we’ll get the numbers at 9.30am exactly.

Updated

RBC Capital Markets reckon the UK economy grew by 0.7% last quarter, but recent weaker data suggest that “the risks are tilted slightly to the downside”.

This chart shows how the UK service sector has recovered faster than the rest of the economy, since the collapse of Lehman Brothers in 2008.

Updated

Andrew Sentance, a former Bank of England policymaker, predicts that the UK grew by 0.7% or 0.8% in the last quarter (not exactly sticking his neck out!)

That’s:

“still quite respectable in the relatively slow growth world we’ve seen since the financial crisis”.

Sentance also reckons that the UK will lead the G7 growth league this year, for the 10th time since 1980.

UK growth may slow a bit in Q3 but to remain relatively strong into next year. My interview with @BloombergTV today: http://t.co/4A7ObIEl62

— Andrew Sentance (@asentance) October 24, 2014

Updated

James Knightley, economist at ING, predicts that UK GDP rose by 0.8% in the third quarter, down from 0.9% in Q2.

That’s partly due to weaker Eurozone demand, but the story remains “very positive”, he adds:

Today’s 3Q GDP report is expected to show the seventh consecutive quarter of expansion with the economy 10.2% larger than it was when activity bottomed out in 2009.

And here’s a Vine from Number 11, via Sophy Ridge:

Updated

Is the chancellor having a party?

16 boxes of white wine carried into No11... pic.twitter.com/3FM63t3HOv

— Sophy Ridge (@SophyRidgeSky) October 24, 2014

Drinks order for Mr Osborne

A large Carlsberg van has been spotted outside George Osborne’s residence in Downing Street.

That’s via Sophy Ridge of Sky News:

Carlsberg delivery at No 11... Will the Chancellor have something to celebrate after today's GDP figures? pic.twitter.com/7SPYl8iUYe

— Sophy Ridge (@SophyRidgeSky) October 24, 2014

Or drowning his sorrows? We’ll find out in 40 minutes.....

Updated

Robert Oxley fears that Brussels could dip deeper into Britain’s pockets, if today’s growth figures are decent

Will expected improved GDP figures at 0930 mean even more money for the EU?

— Robert Oxley (@roxley) October 24, 2014

European stock markets have all dropped this morning, by around 0.4%.

That follows a late selloff on Wall Street, after a doctor in New York tested positive for Ebola.

Marc Ostwald of ASM Investor Services says:

The news flow on the NY Ebola case will naturally catch plenty of attention, while the European Council meeting to discuss the EU Budget is set to be a stormy affair, above all in the wake of the demand for an extra £1.7 Bln from the UK (because the economy’s doing so “well”)

Updated

Anger as UK told to pay more to Brussels

Today’s growth figures are overshadowed by the news that Britain has been asked to contribute another £1.7bn to the European Union budget.....

...because its economy has performed better than its EU neighbours.

The revelation dominates today’s front pages, and has outraged critics of Brussels.

As my colleagues Ian Traynor and Nick Watt explain:

The demand is certain to be used against David Cameron by the growing camp who want the UK to quit the EU.

British and European commission officials confirmed that the Treasury had been told last week that budget contribution calculations based on gross national income (GNI) adjustments carried out by Eurostat, the EU statistics agency, had exposed a huge discrepancy between what Britain had been asked to contribute and what it should be paying, because of the UK’s recovery

Full story: EU budget: UK ordered to pay extra €2.1bn by December

France and Germany, meanwhile, are expected to get rebates. A reward for stagnation?

You can imagine the howls of outrage.

But here’s a flavour anyway, from Conservative Peer Lord Michael Ashcroft:

It is hard to believe that the European Union can legally charge the UK an extra £1.7billion because we have a stronger recovering economy.

— Lord Ashcroft (@LordAshcroft) October 24, 2014

Times columnist Tim Montgomery:

The EU must want Britain to vote UKIP http://t.co/rtPORdkjl7 pic.twitter.com/ud4CVRaZLx

— Tim Montgomerie (@montie) October 24, 2014

And Robert Oxley of Business for Britain:

EU demand for £1.3bn is punishment for making the right decisions. Must be rejected.@forbritain vigorously opposed

— Robert Oxley (@roxley) October 24, 2014

But, as former MP Denis MacShane points out -- Britain has benefitted from these same calculations in the past:

In 1990s EU sent £700 mn to UK because we were poor and others were rich. Did `German, Dutch media, MEPs turn it into a mega moan

— Denis MacShane (@DenisMacShane) October 24, 2014

When UK boom goes bust - as it always does - will French radio be full of French MEPs saying UK is a 'basket case'? Insults not grown-up

— Denis MacShane (@DenisMacShane) October 24, 2014

Updated

Why GDP is an imperfect measure of the economy

A quick disclaimer on today’s growth figures. GDP isn’t a perfect tool, by any measure.

Today’s numbers are only based on data from July and August - ONS statisticians will have extrapolated those figures into September.

And it’s a blunt instrument, that doesn’t care whether economic activity was harmful or beneficial to the UK, for example (building a hugely polluting power station is treated alongside a new hospital).

And it doesn’t take any account of income inequality -- whether the growth was spread ‘fairly’, or ‘unfairly’.

As the brilliant John Kay wrote in the FT in April:

It values expenditure on war and nursing care on the same basis. It records the despoliation of the environment only by reference to the amount spent despoiling it, and then includes the amount spent to clean it up.

It does not tell us how happy we are or how fulfilling are our lives.

It also struggles to measure technological change, and flatters countries with large reserves of natural resources or jam-packed with multinational companies.

Opening Post: UK GDP figures released this morning

Good morning.

It’s GDP Day - when we get the first official indication of how the UK economy performed in the third quarter of 2014.

And we’re expecting to find that Britain’s economy slowed over the summer.

City economists predict that UK GDP rose by 0.7% between the start of July and the end of September. Not a bad result, but a less vigorous performance than the first six months of 2014 (GDP rose by a healthy 0.9% in the April-June quarter).

UK third quarter growth figures out today @ONS

— Panmure Gordon & Co (@HPanmureGordon) October 24, 2014

A poor reading will raise concerns that Britain’s recovery is losing pace, in the face of a weakening world economy. The eurozone ground to a halt earlier in the year, while growth in China also slowed in the last three months.

The GDP report comes at a somewhat tricky time for chancellor George Osborne. The latest public finance figures showed that the UK borrowed more this year than a year ago, despite the fabled Long-term Economic Plan (a phrase I fear we’ll hear a few times today).

The data will also show which parts of the UK economy fared particularly well, or badly, last quarter.

Economists reckon the service sector, which makes up about three quarters of the economy, probably outpaced manufacturing and construction.

Paul Hollingsworth of Capital Economics warns:

“The provisional estimate of Q3 GDP is likely to show that the economic recovery has maintained a healthy degree of momentum, but has become increasingly dependent on the services sector.

“The upshot is that while the recovery remains robust, it has become a bit more unbalanced.”

The data is released by the Office for National Statistics at 9.30am BST on the dot.

I’ll track all the details and reaction, along with any other major business and finance news -- including how the markets react to the news that a US doctor has tested positive for Ebola in New York.

Updated