/AI%20(artificial%20intelligence)/AI%20microchip%20by%20DesignKingBD360%20via%20Shutterstock.jpg)

The chip business is still running hot, and AI is the reason. Data-center spending is strong, customers want more advanced chips, and the companies that sit closest to that demand are still getting the market’s attention. Taiwan Semiconductor (TSM), better known as TSMC, is right in the middle of that story.

Recently, Taiwan Semiconductor announced A13, its latest process node. That matters because TSMC does not build hype around every new generation. It usually signals the next step in the company’s long road map. In this case, A13 is aimed squarely at AI, high-performance computing, and mobile chips. That keeps the big question simple for investors: does a stronger technology lead make TSM stock more attractive from here, or does the market already know the story?

Taiwan Semiconductor Holds a Unique Position in Chips

TSMC is the world’s most important contract chipmaker. It does not make finished gadgets. It makes the advanced chips that power them. That gives it a rare position in the semiconductor world. When chip demand is strong, TSMC tends to feel it first.

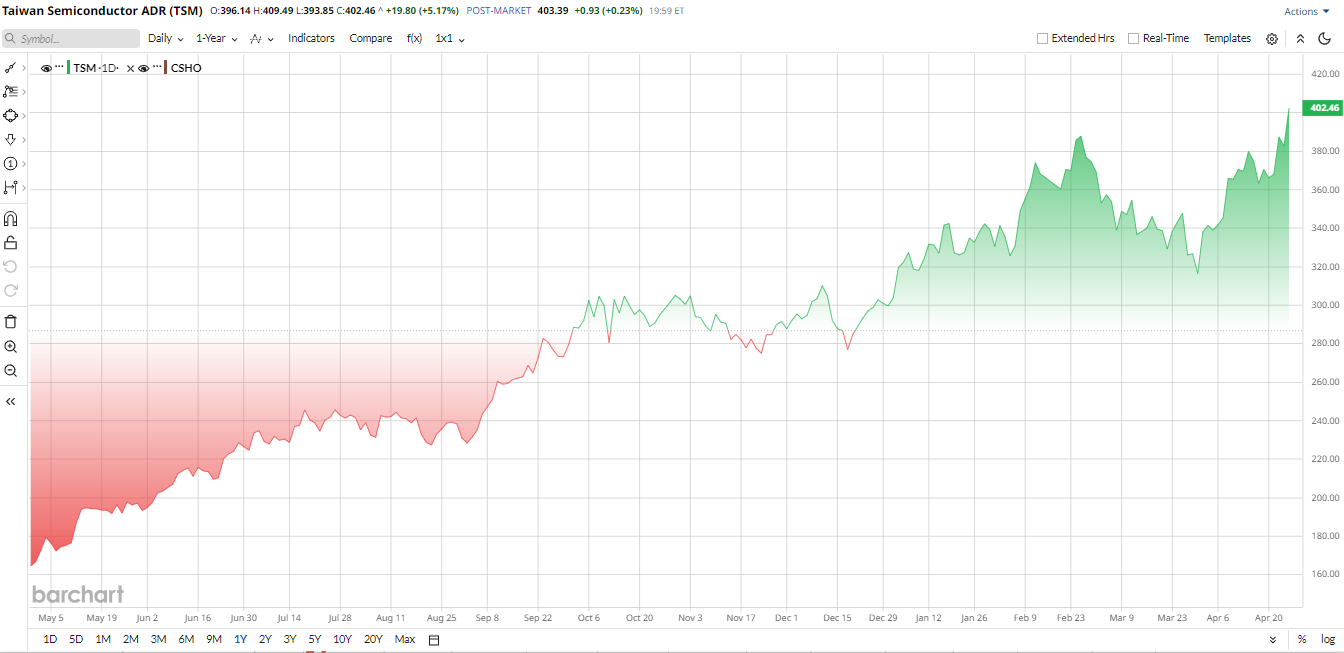

TSM stock has been on a tear lately. Over the past year, TSM is up about 140%, while shares have gained about 29% year-to-date (YTD). This move in the stock makes sense. The AI boom has kept demand strong for leading-edge manufacturing, and TSMC has kept delivering.

The company also benefits from a simple idea. The more AI chips the market wants, the more valuable TSMC’s manufacturing edge becomes. That is why investors keep paying attention every time the company unveils a new node or expands advanced packaging.

On the valuation front, TSMC looks more like a premium growth stock than a bargain-bin name. Its trailing price-to-earnings (P/E) ratio is around 33.5 times. That is well below the semiconductor industry median of about 44 times.

The same pattern shows up in the P/E-to-growth ratio. TSMC’s PEG ratio is about 1.2 times, compared to an industry median near 3.1 times. So, the stock is not cheap in the old-school value sense. But relative to its growth and competitive position, the valuation does not look excessive, either.

What Happened With A13?

The A13 announcement is a reminder that TSMC is still pushing forward. The new node is a direct shrink of A14 and brings around 6% better area efficiency, along with improved power and performance. More importantly, it stays compatible with A14 design rules. That makes it easier for customers to move to the next generation.

That is especially important in AI. Hyperscalers and chip designers want more performance in less space, with better power use. TSMC is trying to be the company that solves this problem first.

Investors liked the message, but they did not treat it like a near-term earnings surprise. That makes sense. A13 is a long-term roadmap win, not a revenue pop next quarter. Still, it reinforces the idea that TSMC remains a core supplier for the AI buildout.

Strong Quarterly Results

TSMC’s latest quarterly report for the March 2026 quarter was strong. Revenue came in at NT$1,134.1 billion, up 35% from a year earlier. Net income jumped 58% to NT$572.5 billion. Adjusted EPS also rose 58% to NT$22.08. That is the kind of growth that keeps bulls interested.

The mix was also good. TSMC said 3-nanometer chips made up 25% of wafer revenue, while 5nm chips accounted for 36% and 7nm chips added another 13%. Altogether, advanced technologies made up 74% of wafer revenue.

That tells you where the company’s strength lies. It is not just about selling more chips — it is selling the most advanced chips in the world.

Cash generation was strong as well. Operating cash flow was NT$658.97 billion. Capital spending was NT$350.76 billion. That left free cash flow of NT$348.21 billion. TSMC ended the quarter with cash and equivalents of more than NT$3 trillion.

CEO C.C. Wei made the message clear. He said customers come to TSMC for a reliable stream of new silicon technologies, and that remains the core of the bull case.

For the next quarter, management expects continued strong demand. It also signaled that capital spending remains high, which is not a surprise. The company is still building for the AI cycle. Full-year analyst estimates still point to strong top-line growth and higher earnings of about $15.10 per share in 2026, supported by AI demand, advanced-node ramps, and packaging expansion.

TSMC Is Still Busy in 2026

TSMC is not standing still. It is expanding CoWoS packaging, which helps customers pack more compute and memory into one system. That matters a lot for AI workloads. It is also building out its global manufacturing base, including U.S. expansion plans.

That is a positive for long-term resilience — and a reminder that TSMC’s spending needs will remain high. That could pressure margins in the short term, even if it supports bigger growth later.

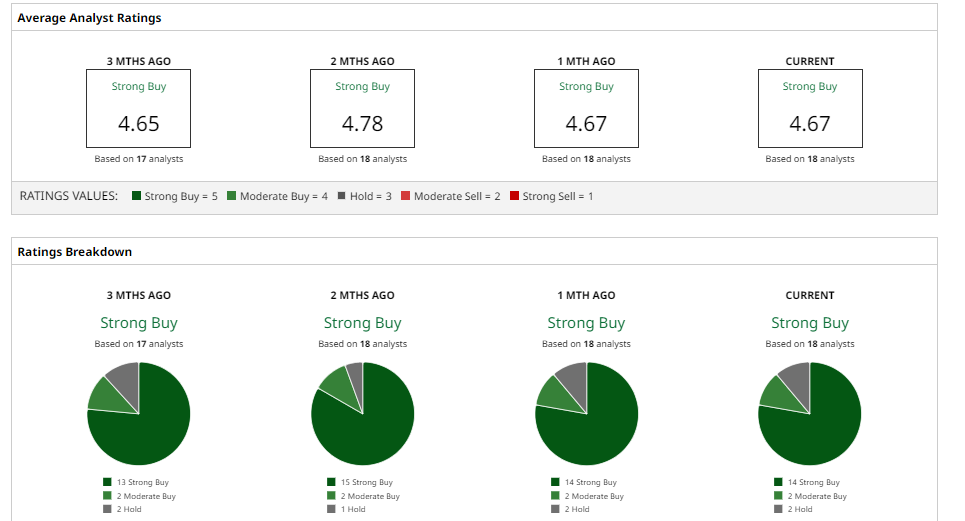

What Do Analysts Think of TSM Stock?

Wall Street still likes TSM stock. Morgan Stanley recently raised its price target and called TSM attractive relative to its earnings power. Goldman Sachs lifted its target to NT$2,600 and kept a “Conviction Buy” rating, pointing to AI as a bigger and bigger driver. Barclays also raised its target to $470 and said that TSMC remains a core holding.

Aletheia Capital went even higher with a $600 target and a “Buy” rating. The common thread is simple: analysts think TSMC’s AI exposure, technology lead, and capacity expansion still give the stock room to run.

Barchart’s consensus view remains positive, too, with an overall “Strong Buy” rating and an average price target of $439.38. That suggests 12% potential upside from current levels, even after the strong move this year.

The Bottom Line

Taiwan Semiconductor is not a cheap stock. But it is one of the best-positioned companies in the AI supply chain. A13 does not change that by itself. What it does is confirm that the company is still moving ahead of the pack. For investors who want AI exposure without chasing the loudest names in the market, TSM stock still looks like one of the cleaner ways to play the trend.