President Donald Trump may be celebrating his long-awaited victory over the Federal Reserve's rate policy, but underneath the surface, inflationary pressures remain dangerously persistent.

Earlier this week, the Federal Reserve cut its benchmark interest rate by 25 basis points to a range of 4.00%-4.25%, meeting widespread expectations. The move followed mounting political pressure and signs that the central bank is now leaning more heavily into the labor market part of its dual mandate, potentially at the expense of curbing inflation.

But here's the catch: the Fed's own projections show inflation staying above the 2% target well into 2027.

In its updated "dot plot," Fed policymakers penciled in two more rate cuts in 2025, bringing the median year-end rate to 3.6%. One additional cut is expected in both 2026 and 2027.

This easing cycle is occurring despite upward revisions to inflation forecasts, with core PCE inflation expected at 3.0% in 2025, 2.6% in 2026, and only reaching 2.1% in 2027.

Tariffs Are Not A Big Risk For The Fed

Fed Chair Jerome Powell also downplayed the extent to which tariffs are feeding through to consumer prices.

“A reasonable base case is that the effects on inflation will be relatively short-lived—a one-time shift in the price

level,” he said on Wednesday.

Powell indicated that inflation is still expected to rise—maybe not as much as a few months ago—but the pass-through from tariffs has been slower and more limited.

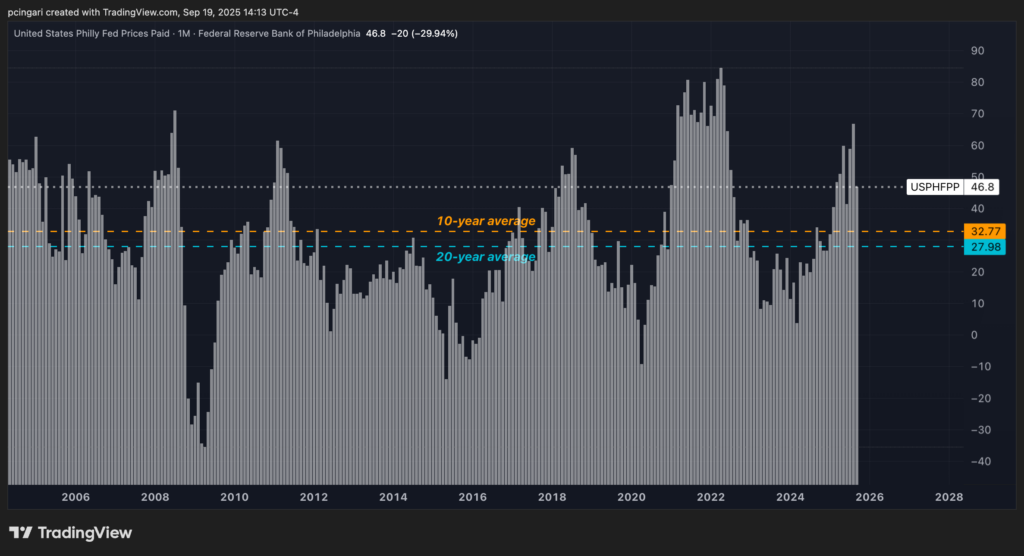

What About Philly Fed Data?

Some observers latched onto the September 2025 Philadelphia Fed Prices Paid index, which dropped sharply to 46.8, the steepest month-on-month drop in a decade.

But this decline is more noise than signal.

Even after the plunge, the index remains significantly above its historical average of 32.8 over the past 10 years and 28 over the past 20.

This suggests that while momentum has softened, price pressures remain historically elevated.

Does Inflation Still Have Teeth?

Economic data says yes. Consumer data says yes. Even the Fed's preferred metrics say yes.

Let's start with the Consumer Price Index (CPI). In August 2025, the CPI was up 2.9% year-over-year, rising from 2.7% in both June and July. Core CPI, which strips out food and energy, came in at 3.1%, steady from June and July but up from 2.8% in April and May.

The Personal Consumption Expenditures price index was 2.6% in July, up from 2.4% earlier this year. More concerning, core PCE inflation —the Fed's go-to inflation gauge— rose to 2.9%, increasing from 2.7% in May and 2.8% in June.

Despite the Fed's projections, the market doesn't buy a rapid return to the 2% target.

A forward-looking measure shows a 61.5% chance that PCE inflation will exceed 2.5% over the next 12 months, making it more likely than not that inflation remains sticky.

What Are Consumers And Investors Saying?

The University of Michigan's September survey shows 1-year inflation expectations at 4.5%, a level more in tune with persistent inflation than returning to price stability.

And bond traders? The 10-year breakeven rate—which reflects the market's average inflation expectations over the next decade—stands at 2.38%, further reinforcing skepticism that 2% inflation is in reach.

What's The Risk For The Fed?

By pushing the Fed into a rate-cutting cycle and celebrating the outcome, Trump may be staking his political capital on a strategy that could backfire.

If inflation keeps rising, the cuts may be reversed—or worse, if they aren’t, it could signal the Fed’s independence is effectively compromised.

Read Next:

Photo: Joshua Sukoff from Shutterstock