/Trane%20Technologies%20plc%20logo%20and%20price%20data-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

Swords, Ireland-based Trane Technologies plc (TT) designs, manufactures, sells, and services industrial equipment. With a market cap of $95.4 billion, the company offers central heaters, air conditioners, electric vehicles, air cleaners, and fluid handling products.

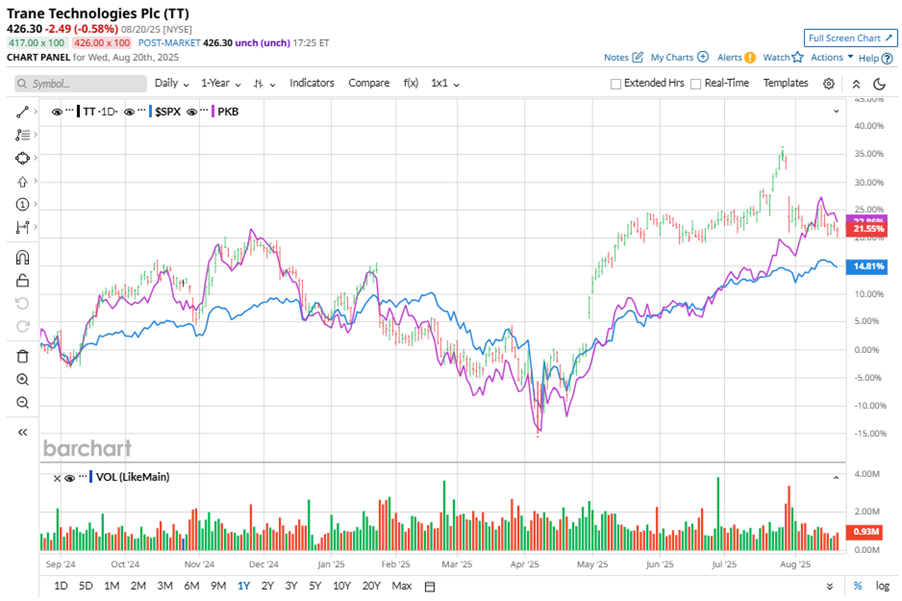

Shares of the global climate innovator have outperformed the broader market over the past year. TT has gained 22.6% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 14.3%. In 2025, TT stock is up 15.4%, surpassing the SPX’s 8.7% rise on a YTD basis.

Narrowing the focus, TT’s underperformance is apparent compared to the Invesco Building & Construction ETF (PKB). The exchange-traded fund has gained about 25.2% over the past year. Moreover, the ETF’s 17.8% returns on a YTD basis outshine the stock’s returns over the same time frame.

Trane Technologies is outperforming due to the growing demand for sustainable solutions that reduce energy consumption, emissions, and operational costs. The company's recent acquisition of BrainBox AI and establishment of the BrainBox AI Lab are driving innovation in AI-powered building solutions, enabling smarter energy use and digital transformation.

On Jul. 30, TT shares closed down more than 8% after reporting its Q2 results. Its revenue stood at $5.7 billion, up 8.3% year-over-year. The company’s adjusted EPS increased 17.6% from the year-ago quarter to $3.88.

For the current fiscal year, ending in December, analysts expect TT’s EPS to grow 16.4% to $13.06 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

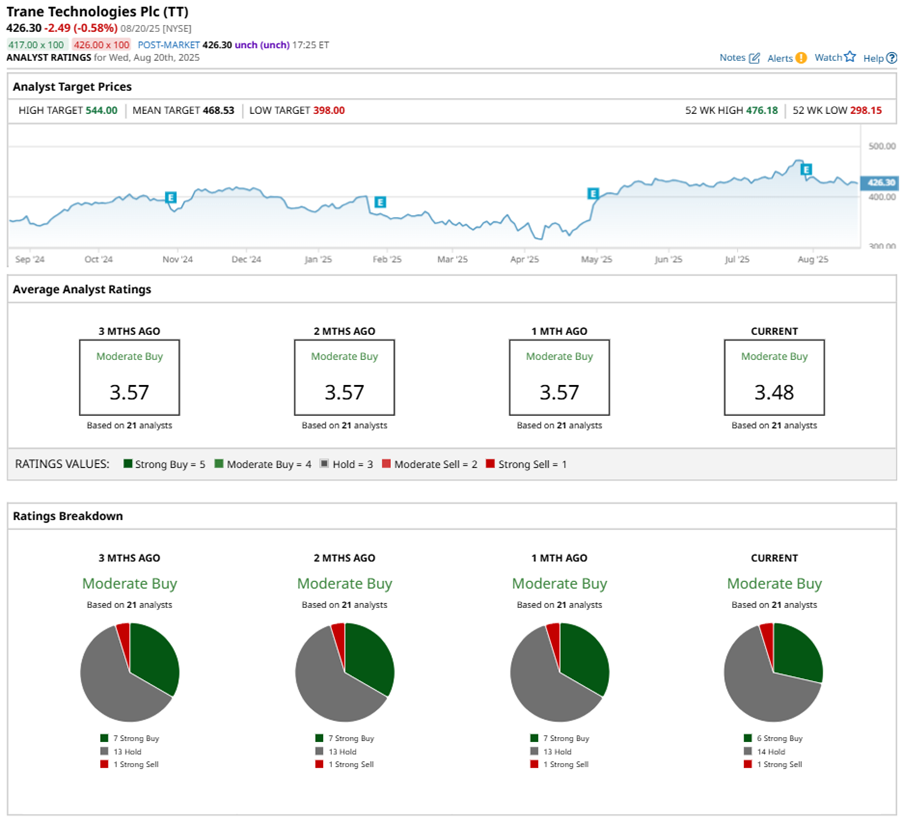

Among the 21 analysts covering TT stock, the consensus is a “Moderate Buy.” That’s based on six “Strong Buy” ratings, 14 “Holds,” and one “Strong Sell.”

This configuration is less bullish than a month ago, with seven analysts suggesting a “Strong Buy.”

On Aug. 7, Andrew Kaplowitz from Citigroup Inc. (C) maintained a “Buy” rating on TT with a price target of $499, implying a potential upside of 17.1% from current levels.

The mean price target of $468.53 represents a 9.9% premium to TT’s current price levels. The Street-high price target of $544 suggests an upside potential of 27.6%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.